I have to tell you some terrible things.

I have to tell you some terrible things.

I didn’t want to do it – I almost didn’t bother with this post as it’s soooooo depressing and who wants to hear that crap but there’s also a lot of stuff going on and it’s my job to inform you of it so I’m HOPING (because I am a hopeful guy) that, if we get it out of the way now, we can start the new week in a better mood. So, I’ve decided to post up some of the news stories I’ve been reading but intersperse then with encouraging pictures to take the edge off a little:

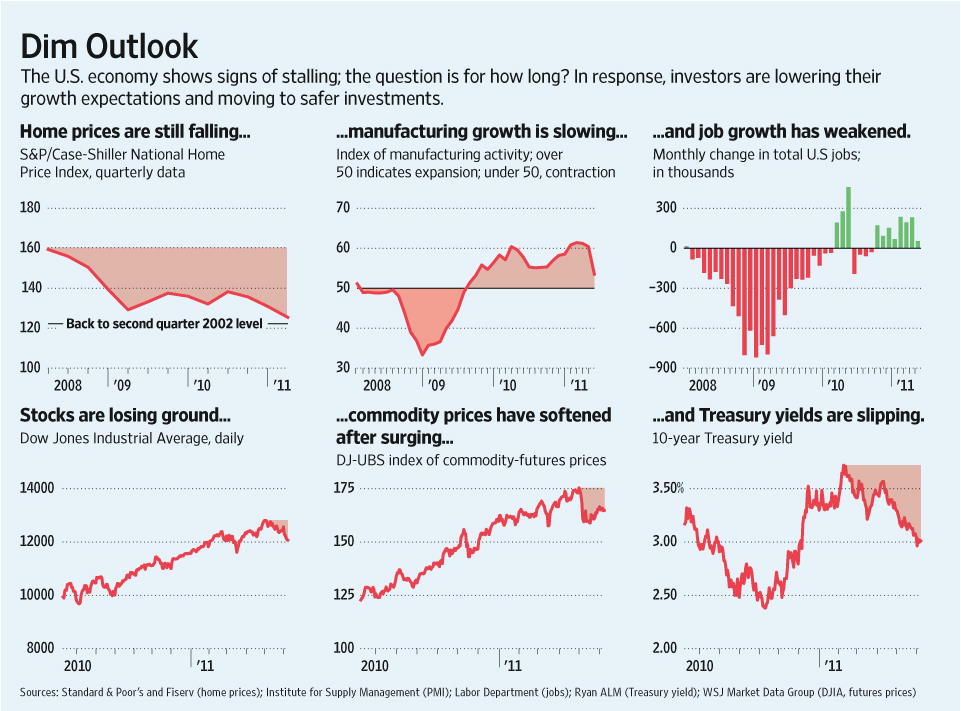

First, a couple of items about jobs. It seems that the aggregate hours worked in U.S. economy from all workers moves back to February 1999 levels. 25 million Americans out of work or looking for full-time work as middle class continues to shrink. RortyBomb points out: "This is part of what people mean when they say there’s unused capacity, and that’s a tremendous waste of people’s talents and lives." An unemployed person detracts from the wealth of the nation and anyone in Congress who doesn’t believe that does not value the American workers and should not BE valued by them in November! Equally awful: At this point, only 45 percent of Americans now have health insurance through their employers. Equally startling is the 16.6 percent (52M) that have no insurance at all. The employment figures are one facet of the larger storyline of a shrinking middle class.

Meanwhile, as our Congresspeople tell us we can’t afford $1Bn for this and that program that benefits the American people, Brown University’s Eisenhower Research Project just released a study that shows 225,000 people killed in the Iraq-Afghanistan wars, 137,000 of whom were civilians with 7.8M people turned into refugees – about the entire population of Connecticut and Kentucky combined forced to flee their homes and about 20% of population of the countries we invaded. They US has spent about $4,000,000,000,000 on the war (so far), which was enough money to give 8M people $500,000 each rather than blowing up their homes. That’s OK though, there are 110M taxpayers in America so we only borrowed $36,363.63 each to pay for it (so far).

Meanwhile, as our Congresspeople tell us we can’t afford $1Bn for this and that program that benefits the American people, Brown University’s Eisenhower Research Project just released a study that shows 225,000 people killed in the Iraq-Afghanistan wars, 137,000 of whom were civilians with 7.8M people turned into refugees – about the entire population of Connecticut and Kentucky combined forced to flee their homes and about 20% of population of the countries we invaded. They US has spent about $4,000,000,000,000 on the war (so far), which was enough money to give 8M people $500,000 each rather than blowing up their homes. That’s OK though, there are 110M taxpayers in America so we only borrowed $36,363.63 each to pay for it (so far).

According to the Institute: "The human and economic costs of these wars will continue for decades, some costs not peaking until mid-century. Many of the wars’ costs are invisible to Americans, buried in a variety of budgets, and so have not been counted or assessed. For example, while most people think the Pentagon war appropriations are equivalent to the wars’ budgetary costs, the true numbers are twice that, and the full economic cost of the wars much larger yet… There are many costs of these wars that we have not yet been able to quantify and assess. With our limited resources, we focused on U.S. spending, U.S. and allied deaths, and the human toll in the major war zones, Afghanistan, Iraq and Pakistan. There is still much more to know and understand about how all those affected by the wars have had their health, economies, and communities altered by the decade of war, and what solutions exist for the problems they face as a result of the wars’ destruction."

Don’t worry about the money – WE’LL PRINT MORE! In all of last week’s excitement, no one noticed the Fed’s balance sheet clocking in at $2.84Tn – up $600Bn in 6 months in 2011. Now $100Bn a month may not seem like a lot to us rich Americans but it’s a pretty shocking number to someone in Greece, who is being told the THEY are irresponsible for running a $50Bn ANNUAL deficit. Keep in mind that $100Bn a month is only covering 2/3 of our monthly deficit. The Fed’s generosity has led to $1.6Tn of EXCESS reserves piling up among their Member Banks – money that was supposed to be loaned out to provide liquidity to the economy but instead is being pooled in order to collect interest rate spreads that generate ever-increasing bonuses for the Banksters.

Don’t worry about the money – WE’LL PRINT MORE! In all of last week’s excitement, no one noticed the Fed’s balance sheet clocking in at $2.84Tn – up $600Bn in 6 months in 2011. Now $100Bn a month may not seem like a lot to us rich Americans but it’s a pretty shocking number to someone in Greece, who is being told the THEY are irresponsible for running a $50Bn ANNUAL deficit. Keep in mind that $100Bn a month is only covering 2/3 of our monthly deficit. The Fed’s generosity has led to $1.6Tn of EXCESS reserves piling up among their Member Banks – money that was supposed to be loaned out to provide liquidity to the economy but instead is being pooled in order to collect interest rate spreads that generate ever-increasing bonuses for the Banksters.

Speaking of Banksters – they are actually very poorly paid compared to other top 10 earners, earning "just" 333 times what the average American family earns in a year, which is nothing compared to the top 10 non-financial CEOs, who earned an average of 946 times what the average family earns in a year. Perhaps that’s because there aren’t 10 IBanks anymore (that’s an ROFL if you are an insider – it’s funny ’cause we bankrupted the other guys, wiped out their investors and took all their money)! Anyway, Forbes came out with it’s "Top 10 Income List" and Les Leopold summed it all up:

| The Highest Income Celebrities, CEO and Hedge Fund Managers (2010) | ||

| The Top Ten | Average Yearly Income | Number of years if would take for the average American family to earn as much. |

| Hedge Fund managers | $1,753,000,000 | 35,217 years |

| Movie directors/producers | $126,000,000 | 2,531 |

| Top celebrities from all fields | $119,800,000 | 2,407 |

| Pop musicians | $87,200,000 | 1,752 |

| Non-financial CEOs | $47,100,000 | 946 |

| Athletes | $44,600,000 | 896 |

| Movie stars | $42,600,000 | 856 |

| Authors | $26,900,000 | 402 |

| Lawyers | $20,000,000 | 402 |

| Bank/Insurance CEOs | $16,600,000 | 333 |

| Median Family Income (2009) | $49,777 | 1 year |

Yep, Hedge Funds are definitely the place to be with the top 10 of my fellow Hedge Fund Managers earning an average of 35,217 TIMES the median family income of $49,777 – you can see why I’m motivated! Oprah left a big job opening as she clocked in with $290M of income in 2010 and U2 made $190M touring (but they will lose it on Spider Man). Leo DiCaprio got $77M and I have no idea what movie he was in last year and Tiger Woods may have gone soft but he’s still good for for $75M. Another tip if you want to be very, very rich is make sure you don’t forget your penis – as only 6 of the top 100 highest income Americans were women!

CNBC’s Rick Santelli, who is the proud owner of a penis, says the problem is Government Spending, not the fact that there are single people who make as much money as 35,000 middle-class families – as if the money made by one person isn’t taken from others. Buffett is wrong, Santelli says – taxing the above 100 people who make as much as 500,0000 middle class Americans won’t solve the problem but cutting government support for those 500,000 middle class Americans will. And, of course, we won’t even discuss the $600Bn that Corporate America is failing to pay (and that’s only counting on what they declare as profits), that’s enough for 12M other families to get $50,000.

Bill Buckler presents an amusing compendium of facts, which Zero Hedge calls "inconvenient truths," in the latest edition of his newsletter, some of which would make for entertaining anecdotes if presented at the Biden "deficit cutting" talks, which also, and very paradoxically, aim to cut US debt by increasing it.

- Not one penny of US debt has been repaid for 51 years: the last time US government funded debt actually decresed on a year-over-year basis was 1960

- 97% of today’s funded debt has been accumulated since August 1971 – the end of the Bretton Woods era by Nixon, and the terminal delinking of all fiat currencies from any and all hard assets, ushered in the era of modern-day hyper-debt insolvency

- Obama projects 2.5% Fed Funds rate in budget calculations through 2020. Average Fed Funds rate since 1980: 5.7%; Since 2008: 0.00%, If average 5.7% rate was used, projected US deficit would increase by another $4.9 trillion by 2020

- Obama projects 4.2% growth rate over next 3 years. If a normal growth rate of 2.5% is used, deficits would increase by another $4 trillion by 2020

- The US government borrows 40-50 cents for every dollar it spends. A balanced budget would mean cutting government spending in half.

- Implementing a balanced budget would not reduce current debt outstanding. It would merely stop it from growing.

- Over the past three fiscal years US debt grew by over $1.5 trillion per year: this is more than three times the record annual debt increase in any previous year in US history

- Last night deficit reduction targets were cut from $4 trillion to $2 trillion over the next decade, in exchange for a $2.4 trillion debt ceiling hike, which will last the Treasury until the next presidential election. Said otherwise, the Treasury needs to fund a $2.4 trillion hold over the next 15 months. Over a decade this come to $20 trillion: ten times more than the proposed deficit reduction.

Meanwhile, Eric Fry points out that: “Bankruptcy” may look like πτ?χευση in Greek and bancarrota in Portuguese. But the Greeks and the Portuguese both understand that sovereign bankruptcy in Europe means great, big handouts from their neighbors. It means “promise a bunch of stuff, but do almost nothing until the money runs out. After that, bankruptcy will mean what it always means: the borrowers will stiff the lenders and life will move on." The Greeks and the Portuguese will emerge from their dungeon, free from the shackles of debt and austerity, with pocketfuls of drachma and escudos.

Meanwhile, Eric Fry points out that: “Bankruptcy” may look like πτ?χευση in Greek and bancarrota in Portuguese. But the Greeks and the Portuguese both understand that sovereign bankruptcy in Europe means great, big handouts from their neighbors. It means “promise a bunch of stuff, but do almost nothing until the money runs out. After that, bankruptcy will mean what it always means: the borrowers will stiff the lenders and life will move on." The Greeks and the Portuguese will emerge from their dungeon, free from the shackles of debt and austerity, with pocketfuls of drachma and escudos.

How do we know that the story will play out this way? Well, we don’t, but it always does. And one reason we think the bankrupt nations will continue begging money until they ultimately declare bankruptcy is that the Greeks are already at it again. “Barely a day after a multibillion-dollar bailout from the IMF,” Investors’ Business Daily reports, “Greece’s prime minister has his hand out again for yet another loan, this one from Europe. Has his mendicant state become the Oliver Twist of nations?” Yes, is the obvious answer.

Why not beg when the begging is so easy? Papandreou is asking the European Union to lend Greece another $173 billion, on top of the $156 billion bailout the EU and IMF have already approved, and partially dispensed. “Successive rescues, guarantees and bailouts have put the grand total spent so far at $394 billion,” Investors’ Business Daily relates. But Europe seems oblivious to reality as it scrambles to find more money…

The London Telegraph points out that the second bailout sought by Greece is likely to last only until 2014 and will leave an even bigger debt after that. Someone will have to pay. Papandreou’s call for more money after the IMF bailout is a clear signal of a flawed economic model.” “I think this will ultimately be a case in which the doctors kill the patient,” predicts Johns Hopkins University economist, Steve Hanke.

Unfortunately for Dr. EU – we have a highly contagious patient! It doesn’t stop with Greece and Portugal and Italy is already teetering on the brink with their bond rates creeping up to that 7% line, which is generally considered unpayable for countries with Debt to GDP ratios above 2/3 – which is pretty much everyone these days…

You can see how Portugal can break Spain and Spain and Ireland owe Britain $232Bn in addition to the $39Bn from Portugal and Greece the UK has probably already written off but Spain and Italy owe France $731Bn, which would be added to the $180Bn they are unlikely to see again from Portugal, Ireland and Greece so that’s a cool $1Tn of default against France’s total GDP of $2.65Tn so that’s 38% of their GDP that, POSSIBLY, may get flushed down the drain but, of course, it’s far worse than that because the banks that count those loans to Sovereign nations as cash have leveraged those "assets" 10 to 1 and we all know how that movie ends once things start to collapse. Fortunately – the US and Japan are "too big to fail" (more famous last words will never be spoken!) because the economies of the UK and France are pillars of stability compared to us!

Jimmy Galbraith (JK’s son) says: "Europe is in a dire situation. If it doesn’t address the underlying causes of the Greek crisis quickly, Europe’s political project will face the same fate as communism and the US Confederacy."

Europe’s structure is also suspended between two stable formations: the federated nation state and the international alliance. This in-between structure is called aconfederacy, and it is something that was tried and which failed in North America on two occasions, most recently in 1865.

The South lost the US Civil War, in part, because it left too much power in state hands, and so could not in the end raise the funds or the men required to keep its armies in the field.

And following defeat, it took almost 70 years – until Roosevelt’s New Deal in 1933 – before sufficient measures were taken to begin to overcome the dire poverty and economic stagnation of that region. This history too has been walled off in modern (Congressional) minds.

This is how yields have soared on PIIG debts, while they fell simultaneously on US, German, French and British bonds. There was no sudden discovery that Greece was ill-managed or that Ireland had had an unsustainable construction boom. Those facts were known. The new event was the meltdown, the flight to safety, and the waves of predatory speculation that have followed. Therefore what happened was a solvency crisis of the banks, as always happens in debt crises.

This is how yields have soared on PIIG debts, while they fell simultaneously on US, German, French and British bonds. There was no sudden discovery that Greece was ill-managed or that Ireland had had an unsustainable construction boom. Those facts were known. The new event was the meltdown, the flight to safety, and the waves of predatory speculation that have followed. Therefore what happened was a solvency crisis of the banks, as always happens in debt crises.

It was true in the 1980s, when the Reagan administration, no less, felt obliged to prepare a secret plan to nationalize all the major New York banks should a single major Latin American debtor declare default. It was true in 2008-09, when preventing the imminent collapse of Bank of America, Citigroup and others trumped all other US policy concerns. It is obvious that the entire recent thrust of European policy has been to find ways to paper over the problems of Europe’s banks: with phony stress tests, with new loans, with loud talk, with denunciations of profligacy in Greece or anywhere else – with anything except an honest examination of what lies at the heart of the problem.

PIIG loans that are immediately recycled to the European banks, Galbraith says, will add nothing to Greece’s prospects except more debt. This will not lower interest rates, restore growth, or bring success to ongoing internal reforms. It is an intolerable situation and it will not continue for long. Along one road there lies a future of defaults, panic, dissolution of the eurozone, and hyperinflation in the exiting countries, with a collapse of the export markets for those that remain. The final consequence will be large population movements – as happened from the American South. For if Europe insists on reducing its periphery to poverty, it cannot expect those affected to sit still and accept their fate. The same could easily be said of US States that believe they will be able to solve their problems by taxing the poor and cutting services.

In Barron’s, Alan Abelson discusses a Reinhart & Rogoff paper: "The Aftermath of Financial Crises," which says:

Broadly speaking, financial crises are protracted affairs. More often than not, the aftermath of severe financial crises share three characteristics.

First, asset market collapses are deep and prolonged. Real housing price declines average 35 percent stretched out over six years, while equity price collapses average 55 percent over a downturn of about three and a half years.

Second, the aftermath of banking crises is associated with profound declines in output and employment. The unemployment rate rises an average of 7 percentage points over the down phase of the cycle, which lasts on average over four years. Output falls (from peak to trough) an average of over 9 percent, although the duration of the downturn, averaging roughly two years, is considerably shorter than for unemployment.

Third, the real value of government debt tends to explode, rising an average of 86 percent in the major post–World War II episodes. Interestingly, the main cause of debt explosions is not the widely cited costs of bailing out and recapitalizing the banking system. Admittedly, bailout costs are difficult to measure, and there is considerable divergence among estimates from competing studies. But even upper-bound estimates pale next to actual measured rises in public debt. In fact, the big drivers of debt increases are the inevitable collapse in tax revenues that governments suffer in the wake of deep and prolonged output contractions, as well as often ambitious countercyclical fiscal policies aimed at mitigating the downturn.

In "Decline of the Empire," David Cohen points out:

I’ve got some news for people like John Mauldin, Barry Ritholtz, Carmen Reinhart and Ken Rogoff—this time isdifferent, but not in the sense you intend. To understand what is happening in the United States, it is necessary to go far beyond an historical survey of financial crises. You must consider the specific historical circumstances that led to the current crisis. Such a review would include but not be limited to the following observations—

The United States has been hemorrhaging manufacturing jobs for 30 years.

- Almost all of the income gains made during that time went to the top 10% of wage-earners, with most of them going to the top 1%. Wealth inequality grew accordingly.

- Health care costs have been soaring all that time.

- College tuition costs skyrocketed at a pace far beyond the rate of inflation.

- Households took on more and more debt to replace lost income.

- We had not one, but two, substantial economic bubbles during the last 15 years. Without those bubbles, how much would the U.S. economy have grown?

- The private debt to GDP ratio grew and grew, clearly indicating that more and more debt was required to add an additional point of GDP.

- The Federal Government more and more became the tool of monied special interests.

And so forth. When people endorse Reinhart and Rogoff, we are supposed to understand that the Tough Times we’re experiencing now have a well-defined beginning—the financial crisis after the fall of Lehman—and will have a well-defined end—however many years it takes to work through the credit problems. This is utter nonsense. The "historical obversations" I listed above are in fact the root causes of our current predicament.

And in each case, the historical trend has not changed, or has gotten worse. Households now have only slightly less debt than they did before the crisis, but trillions of dollars of housing wealth has disappeared. Health care costs continue to soar, as do college tuitions. Income gains still go to the wealthiest Americans. In short, nothing has changed.

That leaves those who want to believe that All Will Be Well with the same unsolvable dilemma we started out with: how do you tell a credible story that everything will turn out OK? I’m sorry, but no amount of convenient, hopeful rationalization is going to change the American disaster while the roots of the crisis remain in place. The financial meltdown was the proximate, not the ultimate, cause of America’s economic woes.

I hope the cute baby pictures were helpful because this is some really depressing frigging stuff! As I said, I almost didn’t want to write this post as it has not been a happy weekend of reading for me but we do need to be realistic when assessing the economic dangers we face and, when people ask me why I think a quick rally on no volume looks like Bot-driven BS to me – it’s because I have to assume that human traders can read and might be aware of at least a couple of these issues and thus, would not be buying CMG, an upscale version of Taco Bell (YUM has a p/e of 23), for a p/e of 55 – the bond traders certainly are aware of these issues and are trading accordingly!

Graham Summers of Phoenix capital makes the case that the Fed is approaching the end game, which sums up the situation very nicely, saying: "If we step back and look at this plainly, we will see that reality does not in any way match the view that the Fed’s liquidity will solve the financial world’s problems. In fact, we see that each Fed move is having a smaller and smaller impact on the financial markets. Extend this idea out a bit further and you find that we will reach a point at which the Fed will no longer have any control over the financial markets. I believe that we are rapidly approaching that point. Indeed, the Fed has already hit a wall in the sense that the negative impact of its policies (inflation/ prices soaring) far outweigh any positive impact (stocks rallying)."

Graham Summers of Phoenix capital makes the case that the Fed is approaching the end game, which sums up the situation very nicely, saying: "If we step back and look at this plainly, we will see that reality does not in any way match the view that the Fed’s liquidity will solve the financial world’s problems. In fact, we see that each Fed move is having a smaller and smaller impact on the financial markets. Extend this idea out a bit further and you find that we will reach a point at which the Fed will no longer have any control over the financial markets. I believe that we are rapidly approaching that point. Indeed, the Fed has already hit a wall in the sense that the negative impact of its policies (inflation/ prices soaring) far outweigh any positive impact (stocks rallying)."

Simon Johnson asks "Will the United States Default?" He says that the people on Capitol Hill have three distinct views: "The first is, hopefully yes, and this August offers a good opportunity. The second is, possibly yes, but this would be bad, so we need some form of fiscal austerity. The third is, under no circumstances, and any talk of a need for austerity is a hoax. The first view is mistaken. The second view hides a dangerous contradiction. And the third view borders on complacency. So how can we find our way to fiscal responsibility? We need tax reform." Yes, such a simple solution but you look at our "leadership" and you know it’s not going to happens so, perhaps, we are truly doomed.

We’ll see how all this news is digested next week and, of course, we’ll see how earnings look in our first week but we are still very bearish with a few bullish covers and watching those 2.5% lines very closely as we sure won’t be needing those upside hedges if we fail to hold those support levels.