{kind=link}

We're still bearish.

We're still bearish.

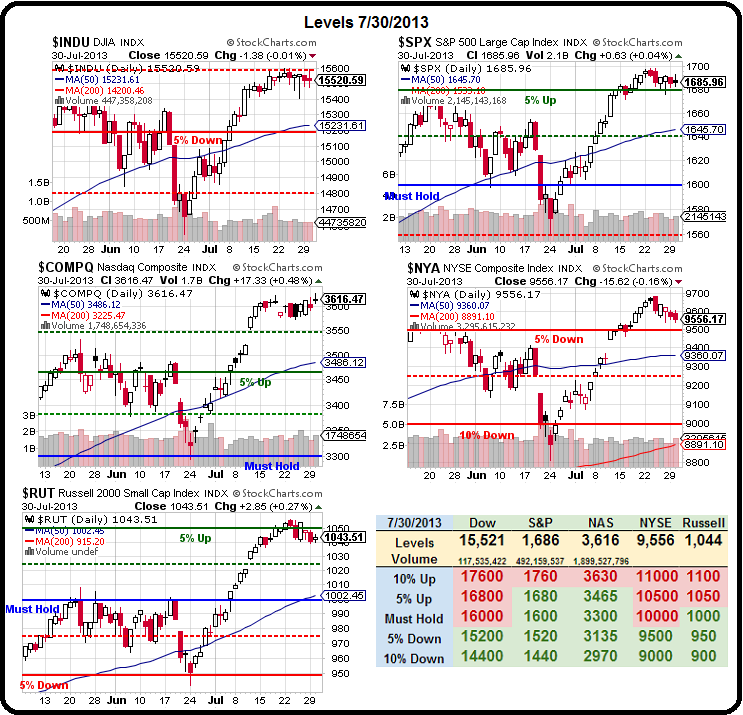

I wish we weren't but the odds favor the bears as we flatline after a 5% run for the month of July. The 5% Rule isn't complicated – we expect a 20% pullback of the run (1%) and we kind of have it on the RUT and the NYSE but, so far, the other indexes are in denial.

In the bigger picture, we ran up from 1,350 on the S&P in November to 1,700 (just shy) last week and that's 25% and again, a 20% overshoot is predictable in our 5% rule so we expect a pullback to 120% of 1,350 to 1,620. We did get that already from the initial run to 1,687 in May so we could call that the correction we needed and, if so, then this is not exhaustion but healthy consolidation for a breakout.

That's why, on Friday, I reiterated our 500% bullish hedges for our Members in Chat – we MIGHT be wrong to be bearish because the Fed MIGHT, the GDP MIGHT be better than we thought and Draghi MIGHT actually do something, rather than just jibber jabber for the 4th consecutive ECB meeting. It COULD happen…

That's why, on Friday, I reiterated our 500% bullish hedges for our Members in Chat – we MIGHT be wrong to be bearish because the Fed MIGHT, the GDP MIGHT be better than we thought and Draghi MIGHT actually do something, rather than just jibber jabber for the 4th consecutive ECB meeting. It COULD happen…

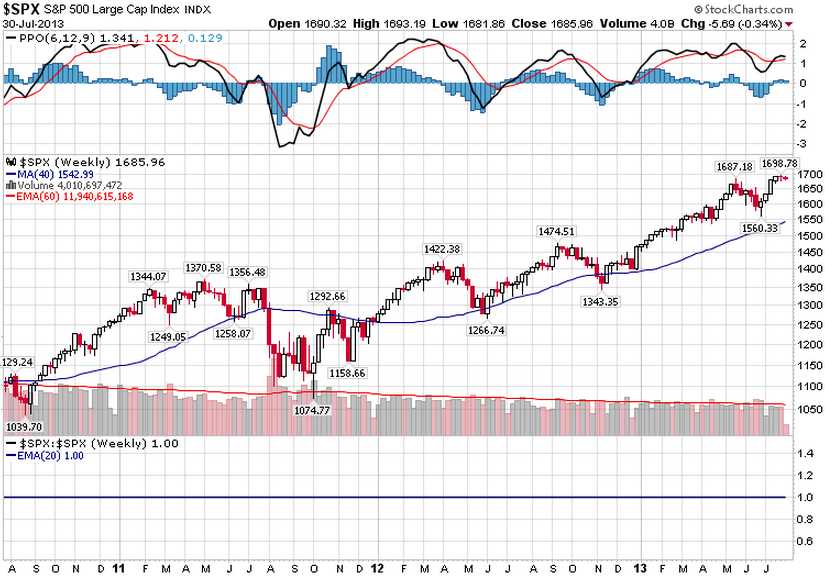

Just in case it doesn't though, we're leaning a bit bearish but, over 1,700 – call us bulls! As you can see from Doug Short's SPY chart, the volume sure doesn't look like what you expect if we're going to break higher and it's downright scary to be bullish when your 200 dma is 10% below your index. Now, a sudden pop over 1,700 isn't going to raise the 200 dma, is it? So, how much higher than the 200 dma do you think the index is likely to go without a pullback?

Clearly, as you can see from the longer-term S&P chart, it DOES happen. Sometimes we get to 15% over the 200 dma (1,773 at the moment) and, as I said, if we pop over 1,700, that's exactly how long we'll play it bullish before going short again. USUALLY, however, 10% is plenty and we tend to get a correction all the way back to the 200 dma (currently 1,542) again over the next quarter:

Can this time be different? Not really. Even though the Fed may ride to the rescue – how do you think we got those out-sized pops in the first place? QE2 was announced in Q4 2010 and that sugar rush got us to 1,344 but then nothing until we corrected. Operation Twist came in Q4 or 2011, saving us from a collapse at the time and ultimately driving us to 1,422 and QE3 hit in November of last year and here we are at 1,700.

The difference is, each time the Fed has stepped in and upped the ante – the market was crashing and they felt it was necessary to get the markets back on track. Why on Earth would they fire off what could be their last barrel when the market is already at record highs?

There is one possible reason: The Fed may feel that we need one more big push to really get things popping and they are willing to gamble that one last ditch, all-out effort to boost the economy to a self-sustaining level will finally work. It's crazy, but it's possible. As Marc Faber says about Central Banker actions: "Insane people don't realize they're insane."

And that is, essentially, the only thing we can be bullish about – that bad news is good news because, despite $105 oil and $4 gas and rising food prices and rising home prices and record market highs – we STILL need more stimulus to go higher NOW!!! Of course it sound crazy when you write it down – that's why they prefer to say it on TV….

8:30 update: GDP is up a whopping 1.7% but they've completely changed the way they calculate it so who the Hell knows what's real. Is this good news that's bad news? Finer minds than mine will have to calculate the "normalized" GDP without the very drastic changes the Government made on this report, which count the development of intellectual propery (books, movies, TV shows, this article) as R&D investment rather than expenses. A change this drastic is adding an estimated $400Bn (2.5%) to our GDP.

8:30 update: GDP is up a whopping 1.7% but they've completely changed the way they calculate it so who the Hell knows what's real. Is this good news that's bad news? Finer minds than mine will have to calculate the "normalized" GDP without the very drastic changes the Government made on this report, which count the development of intellectual propery (books, movies, TV shows, this article) as R&D investment rather than expenses. A change this drastic is adding an estimated $400Bn (2.5%) to our GDP.

I think this good news is bad news because the Fed has to pretend the jacked-up GDP number is real and, based on their completely irrational logic – this news is good so they can't add more stimulus. Also, ADP came in at +200,000 vs +180,000 expected, also good news that can't be ignored by the policy makers.

Well, I'm not seeing any finer minds so far analyzing the GDP, so forgive me for taking a crack at it. Last year's GDP has been revised up from 2.2% to 2.8% using the new R&D calculations. That's a nice 27% upward revision to GDP and that means that we should take 18% off the 1.7% to get to a more realistic 1.24% and that's still pretty good. Another huge benefit of recalculting our GDP to be 27% higher is we lower our debt to GDP ratio by 18% – isn't that BRILLIANT!

Who said our Government can't lower our debt ratio? Between changing the way we calculate GDP and dropping the value of the Dollar 20% – we've made tremendous progress! In reality (I know, ugh) consumer spending, which accounts for more than two-thirds of U.S. economic activity, slowed to a 1.8 percent growth pace after rising at a 2.3 percent rate in the first quarter.

Who said our Government can't lower our debt ratio? Between changing the way we calculate GDP and dropping the value of the Dollar 20% – we've made tremendous progress! In reality (I know, ugh) consumer spending, which accounts for more than two-thirds of U.S. economic activity, slowed to a 1.8 percent growth pace after rising at a 2.3 percent rate in the first quarter.

The acceleration in real GDP in the second quarter primarily reflected upturns in nonresidential fixed investment and in exports, a smaller decrease in federal government spending, and an upturn in state and local government spending that were partly offset by an acceleration in imports and decelerations in private inventory investment and in PCE.

Pre-revision, the GDP was $15.984Tn, post revision we're at $16.535Tn so a nice $550Bn boost, primarily from the Entertainment industry (I read somewhere that Sienfeld alone added $70Bn to the GDP over the years under the new calculations!). Overheard just now at Chinese Finance Ministry: "You can't trust those American GDP numbers. They cook the books!"

Just ahead of the open, the markets are flat but TLT is way down to 106 as sentiment has shifted away from more easing on this "great" GDP report. The Dollar popped back over 82 and I'll be very surprised if we don't get a sell off and a sell-off today can turn those chart ugly very quickly.

So please – be careful out there!