{kind=link}

Woah, we're half way there – Woah, living on a prayer.

Woah, we're half way there – Woah, living on a prayer.

We're waiting on the Fed minutes today (2pm) and, hopefully, more indications that bad news is good news and yesterday's -0.2% Industrial Production and falling Housing Index and weak CPI and poor Redbook Sales were actually good news because the Fed will or won't tighten or whatever the narrative is at the moment – who even cares anymore, it's almost Christmas!

So far, this "rally" of the last few days has erased 30 points of the 90-point drop from S&P 2,010 back to 2,020 and now 2,050 again. Those of you who follow our fabulous 5% Rule™ know that, when we have a 90-point dip we expect at least a weak 18-point bounce (2,038) and a strong 36-point bounce (2,056) before we even begin to consider making bullish bets again. PS – the bounce needs to hold for 2 closes so we are, indeed, not even halfway there.

But we are, in fact, living on a prayer in the hopes that St. Janet and the Immaculate Fed will… oops, what is it we want them to do now? Seriously, I have lost track of the narrative as now we are, for some reason, rallying into the tightening or is it that the recent data is so bad that the Fed would not dare tighten at their next meeting (12/16) – just 7 shopping days before Christmas?

Seriously, I pay more attention to this stuff than pretty much anyone on the planet and I can tell you with absolute certainty that I have no idea what it is traders are now looking for. There is nothing but confusion in the marketplace – which is why we moved to the sidelines.

Seriously, I pay more attention to this stuff than pretty much anyone on the planet and I can tell you with absolute certainty that I have no idea what it is traders are now looking for. There is nothing but confusion in the marketplace – which is why we moved to the sidelines.

And we're not alone, by the way. Since we went to mainly cash back in July (the S&Ps previous trip to 2,100), Institutional Investors have been flying out of the market and hedge funds have been lightening up as well. Of course, some of them are our Premium Members over at PSW but we can't be responsible for ALL of the cashing out in the market, can we? No, I think this is part of a broad trend with the Top 1% rats leaving a sinking ship while the human retail traders are still arranging deck chairs on the Titanic (or shuffling their portfolios).

Here it is, November 18th and the Fed doesn't meet for another month yet we're waiting for clues from the minutes from their October 28th meeting – as if the 60 days of data between the two meetings won't obviate whatever they said almost a month ago. Do you read last month's newspaper to figure out what will happen next month? No, that would be idiotic – but let's treat the Fed Minutes like they came down from Mount Sinai etched in stone. After all, they've guided us so well all year, haven't they?

“It is folly for a man to pray to the gods for that which he has the power to obtain by himself.” – Epicurus

“It is folly for a man to pray to the gods for that which he has the power to obtain by himself.” – Epicurus

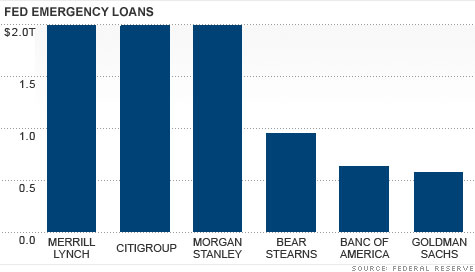

As noted in this month's Harvard Business Review: "On July 9th, 2007, Chuck Prince, then the CEO of Citigroup, made a comment that was to become notorious: “When the music stops, in terms of liquidity, things will be complicated. But as long as the music is playing, you’ve got to get up and dance. We’re still dancing.” Prince meant well. He wanted to reassure reporters in Japan that signs of weakness in the U.S. subprime mortgage market would not cause Citigroup, a major player in that market, to pull back from further lending there."

Two months later Lehman filed for Bankruptcy and Citigroup needed a $476 BILLION bailout to stay alive – costing US Taxpayers $4,000 per household to support Prince's flawed logic. This is what banks do (still) – they engage in lending practices that are as risky as they are legally allowed to and, once they have made TRILLIONS of Dollars worth of bad loans – they fall prey to that old joke that: "When you owe the Bank $1M and can't pay, you have a big problem but, when you owe the bank $1Bn and can't pay – THEY have a big problem."

Two months later Lehman filed for Bankruptcy and Citigroup needed a $476 BILLION bailout to stay alive – costing US Taxpayers $4,000 per household to support Prince's flawed logic. This is what banks do (still) – they engage in lending practices that are as risky as they are legally allowed to and, once they have made TRILLIONS of Dollars worth of bad loans – they fall prey to that old joke that: "When you owe the Bank $1M and can't pay, you have a big problem but, when you owe the bank $1Bn and can't pay – THEY have a big problem."

The big problem the banks have this time around is the $2Tn they have lent to companies over the past 7 years which was, for the most part, used to buy back their own stocks. Silicon Valley has it's own special problem as there are now 140 start-up companies that are valued over $1Bn – getting close to $500Bn in "unicorn" valuations. Now Reid Hoffman (founder of LinkedIn) is warning that as many as half of these companies will not even last long enough to go public. Nonetheless, Hoffman's company owns part of AirBnB – valued at $25.5Bn already – about half of Priceline (PCLN).

Just this week, Standard Chartered Bank (STAN) put $5Bn worth of India loans on an internal watch list. India, China, any shipping company, steel company, oil company, mining company, etc. loans made by any bank are being reviewed for year-end reports that are not likely to be pretty. As you can see from the chart above, debt levels in North America are now DOUBLE what they were in 2008, when the markets collapsed and it took us years to recover. What is it that we've learned since then?

Interest rates, fortunately, are half of what they were so everyone's cash-flow has remained the same, despite doubling down on the amount of debt they have outstanding but what happens when those rates begin to climb?

As Warren Buffett likes to say: "You never know who's swimming naked until the tide goes out" – or the rates go up!

Be careful out there.