{kind=link}

I told you we would be DOOMED!!!

I told you we would be DOOMED!!!

That's right, in Monday morning's post I said:

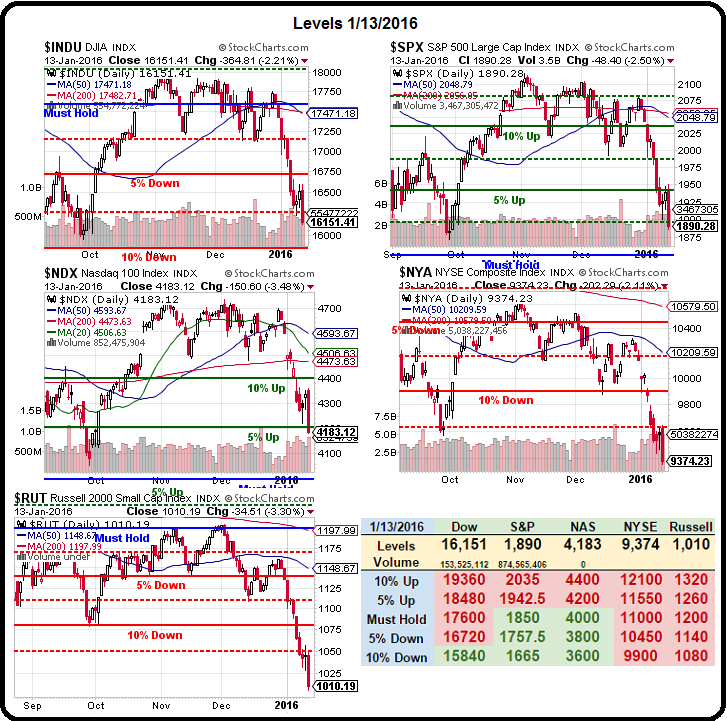

Unfortunately, it's too late for the Russell, which already blew through that line and is back at 1,050, where it MUST HOLD or we are DOOMED!!!

That's right, DOOMED!!!, and I'm not afraid to say it. Panic is in the air and the VIX hit 27 on Friday, just shy of the August high and that means people are FREAKING OUT and the markets can be very dangerous when that happens.

Now we will be watching the 1,000 line on the Russell and, if that fails – we could be looking at another 5% drop for the S&P – all the way to about 1,760 before the next time we'll want to play for a bounce. As I pointed out in my Morning Alert to our Members, none of this is a surprise to us as we called for cashing out when the S&P was at 2,085 back on August 13th (see: Thoughtful Thursday – Contemplating the S&P 500) and, I've repeated it every time the S&P hit 2,100 since.

Now we will be watching the 1,000 line on the Russell and, if that fails – we could be looking at another 5% drop for the S&P – all the way to about 1,760 before the next time we'll want to play for a bounce. As I pointed out in my Morning Alert to our Members, none of this is a surprise to us as we called for cashing out when the S&P was at 2,085 back on August 13th (see: Thoughtful Thursday – Contemplating the S&P 500) and, I've repeated it every time the S&P hit 2,100 since.

Why? Because the VALUATIONS of the actual S&P 500 components did not support 2,100 for the index, that's why! This isn't rocket science folks – over time, value does tend to win out over price – and certainly over Technicals… At the time (8/13), I had concluded:

Over the last year, those overseas revenues have been in rapid decline and we're not picking up the slack at home so there is NOTHING here that justifies the S&P trading at an all-time high – especially when it's 10% higher than last year's trading range with a negative overall growth rate (mostly energy/commodities dragging it down).

So, upon further examination, there is no change to our stance of being short the markets at these levels which, on the Futures this morning, are 17,400 on the Dow (YM), 2,095 on the S&P (ES), 4,550 on the Nasdaq (NQ) and 1,212.50 on the Russell (TF) and, as usual, we look to short the laggard of the set with tight stops above. We also took on a more aggressive SDS (ultra-short S&P) position yesterday afternoon – as we felt the run-up was nonsense anyway – this post just confirms our gut reaction.

I don't want to make you cry if you didn't follow our call, but those S&P Futures finished at 1,875 and, at $50 per point, per contract – that's an $11,000 per contract gain and the Russell Futures were good for a $21,250 per contract profit now that we're long at 1,000. See yesterday's post for why we are getting long here but, in reality, it's no different than why we were short back in August – THIS is the right price for the S&P – so now we are BUYBUYBUYing at the bottom. See how that works?

I don't want to make you cry if you didn't follow our call, but those S&P Futures finished at 1,875 and, at $50 per point, per contract – that's an $11,000 per contract gain and the Russell Futures were good for a $21,250 per contract profit now that we're long at 1,000. See yesterday's post for why we are getting long here but, in reality, it's no different than why we were short back in August – THIS is the right price for the S&P – so now we are BUYBUYBUYing at the bottom. See how that works?

But let's not get carried away. When I say "buying," I mean we are taking advantage of the high VIX levels to SELL premium and position ourselves to own stocks AFTER they fall an additional 20%. We do this by selling puts at prices we'd like to pay (see earlier posts this week and last for examples as well as the famous "How to Buy a Stock for a 15-20% Discount") and we do it SLOWLY because there is no rush to jump back in when we have all this lovely CASH!!! on the sidelines.

In that video (from June, 2014), in fact, AT&T (T) was trading at $30 and we used it as an example for a stock we could buy at a discount. T is now $33.74 but, because of the high VIX, we can once again sell 2018 $30 puts for $3 for a net $27 entry, which is exactly 20% off the current price. The way that works is we get PAID $3 in exchange for our promise to buy AT&T for $30 between now and Jan, 2018. If the stock stays over $30, the contract expires and we keep the money. If it goes lower – we have our T at a 20% discount to the current price.

The dividend on T is $1.92 a year so we're collecting 75% of 2 years' dividends up front and we don't have to tie up $33.74 in the stock nor do we have to protect the position since it has a built-in 20% cushion. Ordinary margin is $3 per contract so your return on margin is 100% in 3 years if T stays over $30 (doesn't drop 13%).

The other stock mentioned in that video was Apple (AAPL), which was $495 pre-split ($71 in current stock) so of course that was a 100% winner too. Who else gives you such great trades FOR FREE? In AAPL's case, we just so happen to have sold the 2016 $50 (converted) puts for a whopping $30 or $3,000 per contract. Those contracts expire tomorrow and, after 18 months, we will pocket 100% of our $3,000s on that trade too. Now that AAPL has dipped back to $97 – I gave you my new trade idea for them earlier in the week – don't miss out on your $3,000!

AAPL is now a key Dow component and note the Dow Futures (YM) are more pessimistic than the Dow but also keep your eye on the bigger picture – 16,000 is huge support – it was our old breakout line on the previous Big Chart levels but we had to adjust the Dow 10% higher when they changed the components (notably adding AAPL). Don't forget, the Must Hold line (17,600 on the Dow) means that line MUST HOLD for us to remain bullish – the Big Chart is a fantastic indicator to help you keep your head in the game.

In the bigger picture, we're simply consolidating for a move over 17,600 and, to determine whether we should be under 16,000 of over 17,600 (10% swing), we need to examine our Dow components. We did the same thing with the S&P on Aug 13th and that is why we went short on the market and cashed out ahead of the flash crash: Thoughtful Thursday – Contemplating the S&P 500

- AAPL ($97.39) is certainly worth more than $97, at least $110 this year (conservatively) so let's say that's good for +100 Dow points.

- AXP ($62.85) has been ripped apart with good cause as they lost their relationship with Costco (COST) but I think they can retake $70 so call that +65 Dow points

- BA ($128.12) is fairly valued here – especially with terrorism on the rise, which gives you the constant risk of a sudden 20% drop. No help.

- CAT ($60.89) is too dependent on China but I love the value down here. No immediate catalyst for a turnaround so: No help.

- CSCO ($24.60) has gone way lower than we thought they should before, so I hesitate to call a bottom here so: No help BUT I will point out you can sell the 2018 $20 puts for $2 for a net $18 entry (26.8% off the current price) and that's a no-brainer bet on the Internet of Things.

- CVX ($81.33) is an oil company and that's BAD. This is the biggest danger to the Dow (and the S&P) as energy earnings are going to be a train wreck with no sign of improvement ahead and, if anything, CVX should be 10-20% LOWER so let's say $10 lower would cost the Dow -80 points.

- DD (56.79) benefits from low oil and nat gas prices (they are input costs) but with Global Manufacturing in a clear Recession – they are another component that could lose 15-20% so call it -60 Dow points.

- DIS ($98.48) we put our foot down at $100 so we're bullish here, of course. Should be at least $110 for +90 Dow points.

- GE ($28.24) also suffering by being a massive multi-national. In addition to the Recession, they get paid in foreign currency that has lost a lot of value vs the Dollars they report earnings in. Sadly, $28.24 is no bargain and I expect to see $25 or less. -30 Dow points.

- GS ($158.99) is the devil and they thrive on chaos in the markets. Much as I hate them, this is a silly-low price for a company dropping $15 a year to the bottom line in a rough year. They should be good for $180 and the good news is that's +160 Dow points.

- HD ($121.40) finally calmed down a little after a MASSIVE 3-year run from $70 to $135 (about 100%) so the $13 pullback is a textbook weak retracement and is in no way bearish. Back to $140 and maybe more is good for +160 Dow points.

- IBM ($131.17) is our runner-up for Stock of the Year 2016 and $150 is a certainty so +160 Dow points, at least.

- INTC ($31.91) reports earnings today and are very fairly priced at $32. The only worry I have is that PC sales have slipped considerably but server sales are through the roof (clouds). This one could go either way so no call.

- JNJ ($97.02) has gone a couple of years now without having to recall a medical device and that's a huge improvement (hips, heart stents, meshs, etc.) and that was the reason I didn't like them. Otherwise, they are a fantastic company and reasonably priced here but no particular reason to be over $100 unless earnings crush on 1/26 ($1.42 expected). No effect.

- JPM ($57.34) like GS is also a good deal down here and, like GS, good for a 10% bump but only $6 in their case so +50 Dow points.

- KO ($41.85) is still a bit overpriced but $40 is fair so let's call it No effect.

- MCD ($115.12) is the comeback kid this year after dipping to $85 in Aug. Not at all cheap and possibly a drop to $100 would be fair if their numbers (1/25) aren't so good but we'll split the baby and call it $107 and that's -65 Dow points.

- MMM ($138.72) has pulled back to a reasonable price and would be a buy in a healthy economy but this isn't one so let's say No effect though, as a long-term play – I like taking a poke here (with short puts, of course).

- MRK ($50.66) is the one we never buy (vs PFE) but not a bad price at $50 – especially with the $1.84 dividend (3.6%). Good for $55 would be +40 Dow points.

- MSFT ($51.64) has been on fire since dumping that dead-weight Ballmer. That guy was costing shareholders $200Bn in market cap! Well, maybe not $200Bn because $414Bn (current cap) is a bit silly and figure they can use a 10% drop to get realistic for -40 Dow points.

- NKE ($58.78) has been everybody's darling and it too was up 100% in 3 years at $67.50 and now down about 10% is nothing more than a healthy correction. As a New Yorker, I have always understood that poor people will spend $100 on sneakers – when you don't have a car – this is how you flash money! So no recession for NKE and GPRO is getting cheap enough that NKE can pick them up for pocket change (which is all they are worth) to add to their tech holdings (though they might be saving up for FIT, which is another disaster that would make a good NKE accessory). Anyway, NKE is only fairly priced here and could go lower with the market or could go back to $65 so No effect.

- PFE ($30.37) is back in our sweet spot and certainly worth 10% more but that's only $3 or +25 Dow points.

- PG ($75.85) is fairly priced at $75 and could go either way. No effect.

- TRV ($106.06) is 70% Business Insurance, which is nice and steady compared to Personal so they should get a better premium than most insurance companies but they don't, so they are a bargain here. Good for at least 10% is +80 Dow points.

- UNH ($109.23) is still a good, steady grower and getting to be a bargain as they close in on our $100 buy line. Not that they can't go down first but certainly good for $120, which is +80 Dow points.

- UTX ($88.83) makes most of their money in Climate Control Systems (36%) and 25% elevators (Otis, my man!) and we know more and more people need their climate controlled these days. China is killing the elevator business but this is a fantastic entry price for a long-term hold on UTX, though no immediate catalyst so I reluctantly say No effect on this one, but I am bullish.

- V ($73.10) is not a good stock to jump into in a recession and may even be still 10% overpriced at $73 so I have to call it at least a $4 drop for -30 Dow points.

- VZ ($44.15) always loses to T when we're deciding what to buy but we like T (see above) for 10% and we like VZ for 10% too so +30 Dow points.

- WMT ($61.92) we already grabbed under $60 and we already had a nice bounce and they are certainly good for $65 but that's just +25 Dow points.

- XOM ($75.65) is more realistically priced than CVX but also faces a lot of headwinds and could easily drop 10% so let's call it -50 Dow points at least.

So, overall, our 30 Dow components look like they are only good for about 700 Dow points, which is only twice as much as they lost yesterday. The good news is we can call a bottom here (16,000) but the bad news is we're not likely to go anywhere from here and what goes for the Dow likely goes for the other indexes as well.

There are very profitable ways to trade flat markets (see "The Secret to Consistent 20-40% Annual Returns") – especially when we can begin our entries with 20% discounts to start the year and we'll be practicing them in our Member Portfolios. This is not to say we can't go 10% lower than we are now before we turn but those valuations won't change (unless the facts do, of course) just because the prices go lower so we will continue with our plan to gradually accumulate stocks from our Buy List at these low levels – happy to add more if they get cheaper!