Bennet Sedacca discusses his reasons for believing we are heading into a depression, and the worst is yet to come.

Welcome to the Depression

Recession:

A recession occurs when a nation’s living standards drop and prices increase. This downturn in economic activity is widely defined as a decline in a country’s gross domestic product for at least 2 quarters.

Depression:

An economic condition caused by a massive decrease in business activity, falling prices, reduced purchasing power, excess of supply over demand, rising unemployment, and other negative economic factors.

– Bloomberg financial definitions

Truth or Dare: Recession or Depression?

As unpopular as it may have been, I have been writing about the impending recession over the past several years. I am rather used to being called a "perma-bear" as it relates to the asset-based, over-leveraged mess we call our economy.

Truthfully, it’s been no fun whatsoever to call ’em as I see ’em. An outlier view has been a necessary evil, however, and one that I’ve been proud to have had the guts to provide.

I will now turn to what, in my view, is the biggest risk of all: We’re in a recession – and the economy can actually shrink. And shrink it has, is, and will likely continue to do. The question now: Are we going through a traditional recession, or a once-in-a-lifetime depression?

I actually hoped the unprecedented credit unwind would end up in a nasty recession; but I fear a depression is either upon us or will soon be upon us. To be truthful is essential in markets and life: To face head-on the bad news which isn’t at all fun or exciting to face.

I hate to say this, as unpopular as it may be: Welcome to the depression. For my reasoning, please read on.

Putting the Recession Question to Bed

GDP estimates for 2008’s fourth quarter are due to be released on Friday morning at 8:30 a.m., with estimates coming in the -5.5% range, which follows a -0.5% number in the prior quarter. Many believe the economy will turn around in the second half of the year, when the Obama administration’s fiscal stimulus plan makes things all better.

I couldn’t disagree more. We have seen these stimulus plans before: Dropping $500 checks into the mail has produced more savings and debt repayment – but not a flow of steady consumption by consumers. Seriously, with new claims for unemployment benefits now averaging over 500,000 per week, the economy losing 600,000 jobs per month, and leverage still piled up on top of leverage, I think the odds of the economy being in growth by the end of 2009 (and possibly the end of 2010) is nothing more than a pipe-dream.

GDP Quarterly Change Since 1994

Are We in a Economic Depression?

There are several criteria that an economy must meet to be in a depression:

- Massive decrease in business activity

-

Falling prices

-

Reduced purchasing power

-

Excess of supply over demand

-

Rising unemployment

-

Other economic factors.

I would like to address these factors one by one in an attempt to determine if we have actually landed in an economic depression – one that sadly may be global in nature.

The Chicago Purchasing Managers Index

The Chicago Purchasing Managers index has fallen off a cliff. The index is a monthly regional index of Midwestern manufacturing activity. An index reading below 50 (we are now at 35.1) means manufacturers are reporting deteriorating business conditions.

Richmond Federal Reserve Manufacturing Survey

Just in case you would like to believe that the Chicago manufacturing number is a fluke, get a load of the chart above, which covers states like Virginia and North Carolina.

Furthermore, if you thought manufacturing alone was under attack, you may wish to reconsider. As the US economy has become more of a service economy and less of a manufacturing economy, many have pointed to the ISM Non-Manufacturing Index for hope. Sadly, that index is plummeting as well.

Everywhere we turn, no matter the industry, no matter the country, the answer is the same: A massive economic slowdown so pervasive that nothing seems to be able to stem the tide.

ISM Non-Manufacturing Index since Inception (1997)

What about falling prices? No matter where we turn, the prices of everything — from equities to commodities (with the notable exception of gold) to esoteric securities to real estate — are falling. I could fill the next 5 pages with gory details, but anyone who opens their brokerage statements knows what I mean.

There used to be "inflation in the things that we need and deflation in the things we want," but that saying is no longer apropos. Everything is falling in price, which is, at best, deflationary; at worst, it signals the depression we may very well be in.

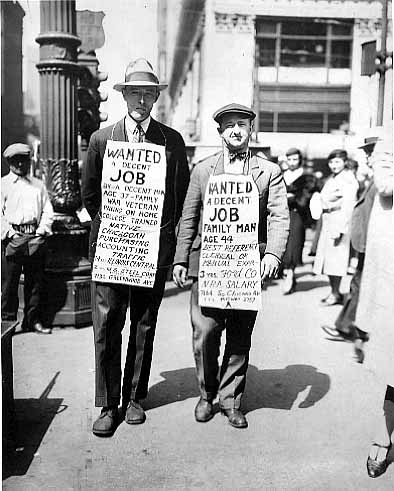

Rising Unemployment – the Really Big Problem

Reduced purchasing power is evident (thus the question of whether supply exceeds demand can be bracketed). The charts above are quite simply proof these issues exist.

The really big problem: unemployment. Like the old saying goes, "It’s a recession when your neighbor loses his job; it’s a depression when you lose yours." As I write this, Caterpillar (CAT), the international leader in heavy equipment, just posted an abysmal quarter; it’s laying off 20,000 people.

Many would have you to believe this is a domestic issue. Nothing could be further from the truth. Since much of Caterpillar’s business is conducted outside the US, it confirms my suspicions that the economic issue is indeed global; anyone hanging their hat on an economic recovery due to a 1933-style infrastructural improvement had better take a look at Caterpillar’s news release.

Just to give you a flavor for how far-reaching the unemployment situation is, the following companies have recently announced job cuts and layoffs – all are global, best-of-breed and industry leaders: Caterpillar, Kimberly-Clark (KMB), Pfizer (PFE), Royal Bank of Scotland, ING (ING), Harley-Davidson (HOG), Philips International, Microsoft (MSFT), Deere (DE), Starbucks (SBUX), United Airlines (UAUA), Schlumberger (SLB), Xerox (XRX), Toyota (TM), Sony (SNE), Union Pacific (UP), Bentley, Reebok, Fiat and Clear Channel (CCO).

OK. Are you depressed yet? If you think that list is scary, consider this: All those layoffs have been announced since last Thursday.

To get a sense of just how bad things have become, I offer up these rather sobering charts:

US Initial Jobless Claims

The difference between this cycle and past cycles is the persistence of the high numbers of laid-off workers and the rather high absolute number.

Sadly, I don’t expect this trend to change for quite some time, with a terminal unemployment rate between 12-20%. Once again, depression-like numbers.

US Continuing Jobless Claims

While the reported unemployment rate in the US creeps toward 7.5%, it’s nowhere near the highs reported in the early 1980s, let alone the rates of prior depressions. The $64,000 question is whether or not we can trust the numbers being reported. As a cynic, I certainly do not. Whether it’s the flawed "Birth/Death Rate Model," which arbitrarily adds jobs via "hedonic adjustments," or other manipulations of the unemployment rate, it’s nearly always understated.

A recent study showed that, when we add in "discouraged workers" — those who have given up looking for a new job and have run out of unemployment insurance — then add part-time workers who want to work full-time, the US unemployment rate is closer to 13.5%.

And with economic activity dropping off a cliff, the 13.5% number seems much more logical to me than 7.2%.

Unemployment Rate, Courtesy of Shadow Government Statistics

According to the data from John William’s website, www.shadowstats.com, the rate stands at 13.5%.

The main point I would wish to deliver here: An economy built on so much leverage, deteriorating so quickly, is going to collapse, no matter what the stimulus (bailouts, buyouts, TARP, Stimulus packages, quantitative easing, mortgage market manipulation, etc).

The economic avalanche is upon us. And if you’ve ever witnessed an avalanche, there is no way to stop it.

In fact, with Ex-Fed Chairman Paul Volcker as President Obama’s economic advisor, I would expect some tough times ahead. Mr. Volcker has a tough-guy reputation (recall he snuffed out double-digit inflation in the early 1980s – I was there to see it, and can tell you it wasn’t fun) by raising short-term rates to near 20%, causing an ugly recession, double-digit unemployment, and pain for all asset classes. The tough decisions he made, however, paid off with a 26-year bull market for Treasuries, which I believe is now over. Finally, I believe Mr. Volcker will be the real force behind the Treasury Department’s actions – not Tim Geithner.

In short, buckle your seatbelts. I continue to avoid credit, under-weight equities, and to batten down the hatches. Unfortunately, I believe the worst is yet to come.