Yes We Can – Turning Change into Debt. Musical selections below.

TURNING JAPANESE – THE AUDACITY OF REALITY

Courtesy of James Quinn, at Financial Sense

I can’t believe the news today

Oh, I can’t close my eyes and make it go away

How long…

How long must we sing this song?

How long? how long…

U2 – Sunday, Bloody, Sunday

Every day seems worse than the previous day. Five hundred thousand people are getting laid off every month. Our banking system is on life support. Retailers are going bankrupt in record numbers. The stock market keeps descending. Home prices continue to plummet. Home foreclosures keep mounting. Consumer confidence is at record lows. You would like to close your eyes and make it go away. Not only is the news not going away, it is going to get worse and last longer than most people can comprehend. The Great Depression lasted 11 years, but the more pertinent comparison is Japan from 1990 until today. A two decade long downturn has a high likelihood of occurring in the United States. There are many similarities between the U.S. and Japan, but in many areas the U.S. has a much dire situation. If the next decade resembles the Japanese experience, there will be significant angst and social unrest.

The talking heads on CNBC were almost unanimously predicting a second half recovery for the economy in the 1st week of January. Most of these people manage money and only earn money if dupes invest their hard earned dollars in their funds. Their analytical case for predicting recovery is that it was so bad last year that it has to go higher in 2009. This is what passes for analysis on Wall Street. The market is already down 7% in four weeks. These “experts” fail to see the big picture and have no sense of history. It took 28 years to get to this point and it will take at least a decade to repair the damage. If the politicians running this country try to take the easy way out (very likely), add another decade to the recovery timeframe. Some indisputable facts will put our current predicament in perspective:

- The U.S. National Debt was $930 billion in 1980, or 33% of GDP. Today it is $10.7 trillion, or 76% of GDP. The National Debt has grown by 1,150% in 28 years. With the planned fiscal stimulus (taxing future generations), the National Debt will reach 100% of GDP during the Obama administration. When Argentina’s economy collapsed in 1998, their National Debt as a percentage of GDP was 65%. The Great Deniers say we are not Argentina. They say we are safe because the U.S. dollar is the reserve currency of the world. This is like jumping off a 20 story building and as you pass the 10th floor someone yells out the window asking how you are doing. You answer, “Good, so far”.

Source: Creditwritedowns.com

- GDP was $2.8 trillion in 1980. Today it is $14 trillion and declining. GDP has grown by 500% since 1980. Our National Debt has grown more than twice as fast as GDP. This is an unsustainable trend. Our economic disaster took 28 years to create and will not be fixed in a year or two.

- Total US consumer debt in 1980 was $352 billion. Today, US consumer debt totals $2.6 trillion. Consumers have increased their total debt level by 738% in 28 years. Revolving credit increased from $56 billion in 1980 to $982 billion today, a 1,750% increase in 28 years.

Source: Mike Shedlock

- The real median household income was $41,258 in 1980. The real median household income in 2007 was $50,233. Over the course of 28 years households are bringing home 22% more. The trickledown theory turned out to be a drip.

- The personal savings rate was 12% in the early 1980’s and reached negative 1% during the Bush administration. It has inched above 2% in the last few months. Based on the previous data, it is not surprising that the savings rate dropped below zero. With virtually no income growth in three decades, consumers have lived hand to mouth and utilized easy debt to maintain their desired lifestyle. This was encouraged by government, banks, big media, corporate America and advertising industry.

Source: Creditwritedowns.com

It is unambiguous, after examining the data, that we have borrowed ourselves to the brink of disaster. Both government and consumers have leveraged themselves to an untenable level. The only logical way to resolve this quandary is to reduce spending, pay down the debt, and increase savings. This is what consumers have begun to do. With consumer spending accounting for 72% of GDP, we are experiencing a serious recession due to the decrease in consumer spending.  The excesses are being painfully wrung out of the system. This process is unacceptable to the socialist politicians who are in domination of the United States today. The government and Federal Reserve have already committed $8 trillion of taxpayer funds to bailing out criminally negligent insolvent banks. Now the Obama administration is going to spend in excess of $1 trillion in an effort to stimulate the economy. They insist that it must be bold and swift. How about well thought out, deliberative, and effective?

The excesses are being painfully wrung out of the system. This process is unacceptable to the socialist politicians who are in domination of the United States today. The government and Federal Reserve have already committed $8 trillion of taxpayer funds to bailing out criminally negligent insolvent banks. Now the Obama administration is going to spend in excess of $1 trillion in an effort to stimulate the economy. They insist that it must be bold and swift. How about well thought out, deliberative, and effective?

Every single dime of the $1 trillion will be borrowed. The government will borrow $1 trillion from foreign countries, hand it out to their constituents, while encouraging them to resume borrowing and spending. Barney Frank and Charlie Rangel will force insolvent banks to lend money to companies, consumers, and deadbeats in foreclosure proceedings. The change we can believe in is – we will borrow and spend our way out of the largest debt bubble in history. Consumers and companies are acting rationally and trying to purge themselves of debt. The government will not allow that to happen. A massive additional dose of leverage will revive the patient. The definition of insanity is doing the same thing over and over, expecting a different result. Are the politicians running this country insane, unintelligent, or just so corrupt that special interests outweigh the interests of the American people? The current pork laden stimulus package will lead to a rerun of Japan’s lost decade, with one vast difference. Our lost decade will terminate in a hyperinflationary collapse.

Japanese Experience

For all of the buy and hold, stocks for the long run, and indexing advocates, please take a long hard look at the following chart.

Source: Mike Shedlock

On December 29, 1989 the Japanese Nikkei Index reached 38,957. Today, the Nikkei Index stands at 8,106, an 80% decline over the course of two decades. It was at this same level in 1983, twenty six years ago. This is what you call a secular bear market. There have been three bear market rallies of 60% and one rally of 140%, but the market is still 80% lower than the peak. The “experts” on Wall Street will tell you this could never happen here. They also won’t tell you that we’ve already lost a decade.

Source: Mike Shedlock

The S&P 500 reached 1,553 in 2000 and took seven years to breech that level in late 2007 at 1,576. It currently stands at 850, 46% below its all-time high. It is at levels reached in 1997, twelve years ago. As the U.S. makes all of the same mistakes Japan made in the 1990’s, another lost decade with stock prices going lower is in the cards. History does not repeat, but it does tend to rhyme. The events and actions by government that led to Japan’s lost decades are eerily similar to what is happening in the U.S. today.

Causes of Japanese Bubble

When talking head cheerleading economists appear on CNBC, the only reference that is made about Japan’s bubble bursting is that the Bank of Japan did not react quickly enough in reducing interest rates. As usual, these economists ignore the big picture. Every economic crisis is caused by some action. No one is delving into how Japan reached the point where their economy crossed the threshold into a deflationary two decades. See if you recognize any of these origins of a crisis:

- The Bank of Japan cut its discount rate from 9% in 1980 to 4.5% by 1986. At the behest of the U.S. government, to comply with the Louvre Accord of 1987, they reduced the discount rate to 2.5% and kept it there for three years. This lax monetary policy created a bubble in the stock market and the real estate market. The monetary supply grew at a 9% rate for the entire 1980’s. The stock market jumped from 15,000 to 39,000 in the space of three years, a 160% gain. A speculative frenzy took hold of the Japanese public.

- With interest rates at historic lows, Japanese banks provided cheap and easy credit to companies and consumers. Consumer debt grew 700% from 1980 to 1990. Japanese corporations took advantage of the soaring stock market to raise $638 billion through stock offerings. Consumers and corporations were incentivized by the low rates to take on more risk to get a positive return. This easy money policy, along with deregulation, tax incentives, and zoning regulations, led to the biggest real estate bubble in history. Mass hysteria that real estate could only go up gripped the nation. Prices reached such heights that intergenerational mortgage loans were required to buy a home. The land around the Royal Palace was said to be worth more than the State of California.

Source: Mike Shedlock

- When it became clear that there was an out of control speculative frenzy, the Bank of Japan raised rates to 6% in five steps from 1989 into 1990. This is given as the cause for the collapse of the stock and real estate bubbles. Both the stock market and land values are 80% below their peak 1989 levels. They are currently at levels seen in the early 1980’s. The scary part of the Japanese experience is that their government did not sit by idly. They used all the tools at their disposal and made the conditions much worse. Government actions caused the crisis and then exasperated the situation. Are you getting the picture?

The cumulative losses in the stock market and by landowners total $15 trillion since 1990.

Japanese Government Blunders

When you listen to the Obama marketing team selling their $1 trillion socialist stimulus package, they say we must avoid the disastrous course of Japan. After examining their lost decade, the results weren’t very bad. The economy was not dynamic, but Japan has retained its position as the 2nd largest economy on the planet.

After growing at a 3.9% annual rate during the 1980’s, Japan’s GDP grew at only an annual rate of 1.1% between 1991 and 2003. Considering the missteps by the government and the huge demographic headwinds blowing against them, Japan still grew their economy. Japan’s cumulative per capita growth this decade has been 13.7%, compared with 12.5% for the United States. And the horrible deflation was not so horrendous.

Consumer prices have been relatively flat for fifteen years. CPI has declined in a few years, but has never reached -1% in any particular year. The lack of demand from consumers has been a function of people being burned in the dual bubble collapse and an aging, declining Japanese population. Japanese consumers have rationally paid down debt and increased savings. The actions of the Japanese government were not rational or intelligent. A replay of these blunders is taking place in the United States today.

- The Japanese government has prolonged their downturn for an additional decade by not allowing bankrupt banks and corporations to liquidate. Zombie banks and corporations existed for decades without writing off the billions of bad debts. They hoarded all of the money provided by the government. Sound familiar?

- The Japanese tried every trick in the Keynesian playbook. Zero interest rates, public works projects, tax rebates and tax decreases. The government built thousands of bridges and roads, driving up government debt to enormous levels. Between 1990 and 2000, the Japanese government instituted 10 fiscal stimulus programs totaling $1 trillion. None of these programs worked. Sound familiar?

- The Bank of Japan purchased commercial paper. The government bought shares of public companies to prop up the stock market. Japan created a $500 billion bank bailout fund, with over $200 billion going towards the direct purchase of stocks. Politicians chose which companies would be propped up. This further distorted the free market. Sound familiar?

- Japan has the highest elderly population of all the developed countries in the world. With the huge loss of real estate and financial wealth, the aging population of Japan needed to increase saving and reduce consumption to insure that they would not starve to death in their old age. An aging population deciding to save for the future made a rational decision. Sound familiar?

Dr. Benjamin Powell clearly explains what happens when the government intervenes in the free markets:

“Japan created a structure of production that did not meet consumers’ particular demands. Producing things that nobody wants and propping up mal-investments cannot possibly help any economy. This policy is equivalent to the old Keynesian depression nostrum of paying people to dig holes and fill them. Neither policy will revive the economy because neither forces businesses to realign their structures of production to match consumer demands.”

It is obvious that the Japanese government created the enormous stock market and real estate bubble through its loose monetary policies in the 1980’s. No matter how much money the Japanese government threw at the problem, they could not convince consumers or companies to borrow and spend. Even with zero interest rates, Japanese companies continued to pay down debt. The billions spent on infrastructure added to the National Debt and did nothing to revive the economy.

If Japan had faced up to the bad debt on its banks balance sheets immediately, they would have experienced a short painful recession of a couple years. By not honestly assessing the true extent of the bad debt and propping up insolvent banks and corporations, Japan sentenced itself to two decades of stagnation. Japan entered this difficult period as a net exporter, with consumers who saved 12% of their income, and a government that had leeway to increase governmental debt. The U.S. has entered a more dangerous period with none of those advantages.

Audacity of Reality

Hope will not get the United States out of our current predicament. It took decades to get to this point and it will take decades to extract ourselves from this debt induced disaster. A few charts will hammer home the reality of the U.S. situation.

Source: Creditwritedowns.com

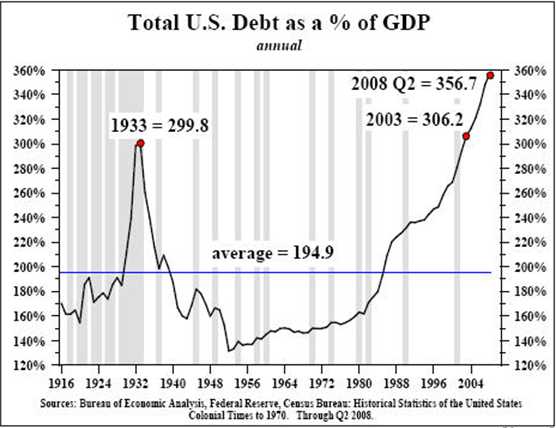

The chart above shows that we enter this financial crisis with total U.S. debt at record levels as of the end of the 2nd quarter of 2008. Since that time we’ve added billions more in debt. At the end of the 3rd quarter, total U.S. credit market debt was $51.8 trillion. The proposed stimulus package of $1 trillion combined with declining GDP will result in the percentage exceeding 400% of GDP by the end of 2009. Japan entered their “lost decade” with total debt of 260% of GDP. Therefore, they had more leeway to expand government debt. Their biggest advantage over the U.S. was that they did not have to convince foreign nations to buy their debt. With large trade surpluses and high savings rates, the debt was purchased by their own citizens.

Source: John Mauldin

American consumers enter this economic downturn as the most indebted people on earth. The materialistic frenzy of the last two decades has left the American consumer saddled with $2.6 trillion of credit card and auto loan debt. Japanese consumers entered their “lost decade” with personal savings rates of 12% annually. Japanese consumers were able to utilize savings to pay down their debt throughout the 1990’s. The American savings rate, which was 12% in 1980, fell below zero in 2006. It has since inched up to 2% in recent months. There are over 300 million credit cards in use today in the U.S. The average American with a credit card is carrying debt of $16,635, according to Experian. With unemployment skyrocketing, wage growth stagnant, and home equity extraction a thing of the past, American consumers are rationally paying down debt. The result is devastating the economy. When 72% of the economy is dependent upon consumers borrowing and spending, deleveraging by consumers will bring the economy to its knees.

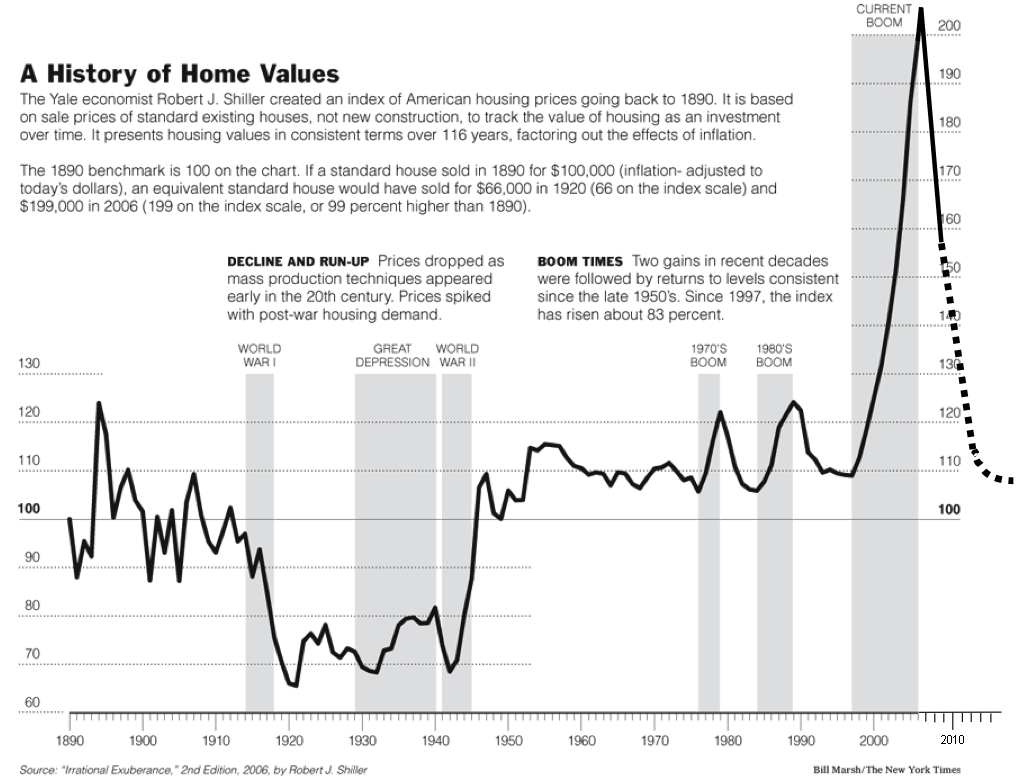

The crux of our current crisis is housing, just as Japan’s crisis was related to real estate. Irrational exuberance, as described by Yale economist Robert Shiller, led to the most outrageous housing boom in U.S. history. It was aided and abetted by greedy investment bankers, sleazy mortgage brokers, dishonest appraisers, Alan Greenspan, clueless ratings agencies, and Congressmen in the back pocket of Fannie Mae and Freddie Mac. Delusional home buyers were convinced that flipping houses was a road to riches. Instead, they’ve skidded off the road and fell into a bottomless ravine.

Source: Robert Shiller

The amazing thing about reversion to the mean is that it always ensues, eventually. The sad thing is that people keep praying that reversion won’t happen this time. Home prices have tracked very closely to CPI for over a century. The housing boom from 2000 to 2006 was so off the charts that people can not come to grips with the dramatic fall that is needed for reversion to the mean to work its mathematical magic. Politicians want house prices to stop falling in the worst way. There is nothing they can do to stop prices from falling to their natural long term equilibrium. Government intervention will only prolong the time frame and delay the recovery. Home prices in Japan fell for 14 years before bottoming in 2004. Home prices have been dropping in the U.S. for 3 years. How does another decade of home price declines grab you? It is entirely possible if the government tries to intervene in the free market process of supply, demand and price.

Bitter Medicine Needed

I know that many Americans are looking for President Obama to solve this crisis in a sound bite way, with no pain and no sacrifice. They want this to end like an episode of CSI with the murder solved within a one hour time slot. Instead we have a Jonestown massacre that will never be fully understood or solved. Was it mass murder or mass suicide? We have experienced a mass hysteria of debt accumulation by consumers, banks, corporations and the government. There is no easy way out. The debt must be paid off and/or written off.

The politically unpopular steps that need to occur are as follows:

- From an overall standpoint, when you have entered a recession due to fiscal irresponsibility, you don’t get out of it by becoming even more fiscally irresponsible.

- Housing prices need to drop another 15% to 20% to reach fair value. This will result in more foreclosures. When prices fall far enough, the houses will sell and inventories will fall. If you cannot afford the payment on your home, you should become a renter. Not everyone should own a home.

- The government and Federal Reserve need to shine a bright light on the bad debt within the financial system. The collateral or lack thereof backing up the government loans needs to be revealed by Treasury and the Federal Reserve. Covering up the worthlessness of these assets is contributing to the frozen system.

- The remaining mega-banks that have caused this crisis need to be put out of our misery. The shareholders and bondholders of Citigroup, Bank of America, Goldman Sachs, Morgan Stanley and any other insolvent banks need to be wiped out. The bad banks should go out of business. The prudent banks that did not take financial system destroying risks should be allowed to succeed based on their merits.

- Failed companies with failed strategies must go bankrupt. If the American auto industry is propped up by taxpayer money the capitalist process of rationalizing manufacturing capacity to final demand will never happen. Allowing companies to fail brings about restructuring and the remaining healthy companies buy the good assets.

- Only infrastructure projects that benefit the citizens of the country should be undertaken. These would include water pipe replacement, electrical grid upgrades and repairing structurally deficient bridges. If the money is spent on worthless make work projects, good investments will be crowded out.

- Tax rebate checks are just a redistribution of wealth from future generations to the spend thrift generation of today. A tax decrease today that is borrowed is a tax increase on our children. They will not stimulate spending.

- Keeping interest rates at zero in an effort to force savers to borrow and spend is penalizing the frugal to benefit the profligate. Borrowing our way out of a debt crisis will never work.

- Consumers should be encouraged to pay down their debt loads and increase their savings rate. The sooner this can be accomplished, the sooner the country can resume growth. Savings will lead to investment.

- The median 401k balance was $18,942 at the end of 2007, with 39% of workers having a balance below $10,000. Approximately 8,000 Americans turn 65 every day. By 2012, 10,000 people will turn 65 per day. Twenty percent of the U.S. population will be over 65 by 2030. An aging population with virtually no retirement savings must increase their savings and cut their consumption dramatically.

- The CEO’s who brought down the entire financial system need to be brought to justice. Angelo Mozilo, Dick Fuld, Charles Prince, Jimmy Cayne, John Thain, Stanley O’Neal, Ken Thompson, Robert Steele, Martin Sullivan, Hank Greenberg, Richard Syron, Daniel Mudd, Kerry Killinger, Raymond McDaniel, Terry McGraw and probably a few I’ve missed, need to be investigated and prosecuted for lying to shareholders about the true financial condition of their firms.

- Fannie Mae, Freddie Mac, and AIG are wards of the state. The U.S. taxpayer is obligated to pay $150 billion to AIG and $200 billion to Fannie Mae and Freddie Mac. AIG is using these funds to undercut other insurance companies in pricing insurance policies. This will result in insurance companies that did nothing wrong being put out of business by the government supported goliath that almost brought down the financial system. Fannie & Freddie are being pushed by Barney Frank and his distinguished colleagues in Congress to provide more 3% down loans to people who won’t pay them back. The Fed then buys the loans and pretends they are good collateral, while not revealing the true value to the public. Sounds like good policy to me. These companies need to be euthanized and any decent assets sold to viable companies.

- Moody’s and S&P should be banned from the rating business. They proved that a AAA rating could be bought. Pension plans, governments, companies, and individuals relied on their ratings. They colluded with the investment banks and must be punished. Their monopoly needs to be ended.

- The SEC needs to be disbanded. We need to push the start over button. They are in bed with Wall Street. They are unable to enforce their vast array of regulations, ignore proof of ponzi schemes, and are a revolving door to top Wall Street jobs. The organization has failed miserably. An agency that does not work needs to be scrapped.

Easy Button Solutions

The solutions described above are too politically difficult to implement. There are not enough courageous people in Washington DC to do what is right and necessary. They want a way out that is easy and painless, like the Staples commercial. The easy solution is to print a trillion dollars, hope the Chinese, Japanese, and oil exporting countries continue to buy our debt, and try to inflate our way out of this mess. And that is just what will happen. The following steps will be taken by our cowardly, short term, blundering politician leaders:

- Despite the fact that this crisis was caused by the Federal Reserve keeping interest rates too low for too long, investment banks leveraging their balance sheets 40 to 1, banks marketing 120% loan to value mortgage loans on overpriced houses, consumers borrowing at obscene levels from their overpriced homes and credit card companies handing out credit cards like candy, the solution will be to keep interest rates at zero, force banks to lend, prop up insolvent banks, stop foreclosures, and give consumers tax rebates so they can resume spending.

- The Democrats controlling Congress will use the remaining $300 billion of TARP funds to allow people who are living in houses they can’t afford to not be foreclosed upon. They will encourage bankruptcy judges to reduce mortgage balances. This will result in a reduction in mortgages available to credit worthy people with higher rates to cover the possibility that a judge could adjust the loan amount in the future.

- With banks not willing to lend, the government bureaucrats running our financial industry will force Fannie Mae and Freddie Mac to make additional bad mortgage loans to unworthy borrowers and guarantee more bad loans from other unworthy borrowers. The Federal Reserve will then buy these bad loans at full price and hide them on their bloated balance sheet.

- Rather than letting the bad banks go bankrupt and allowing good banks to rise up and replace them, the U.S. taxpayer will continue to pump in hundreds of billions into these zombie banks for years before their toxic waste balance sheets are cleaned up. The “Bad Bank” created by the government will overpay for worthless assets and pretend that they will eventually recover the cost. This will be done because the people running the Treasury go to the same Manhattan cocktail parties as the bad bankers and Congressmen have their campaigns financed by these bad bankers.

- General Motors, Chrysler and Ford will come back to Congress in March with restructuring plans that are dead on arrival. They will explain that conditions have deteriorated and they need another $20 billion to keep going. The Democratic led Congress, who is beholden to the UAW, will give them our money. Plants and dealerships that need to close will remain in business.

- Whenever I hear the term “Shovel-Ready” projects, I’m reminded of a line by Paul Newman in Butch Cassidy and the Sundance Kid. “Don’t ever hit your mother with a shovel. It will leave a dull impression on her mind. The U.S. taxpayers are about to be hit in the head with a shovel. The States say they have thousands of projects that are shovel-ready. If an infrastructure project is to the point where it is shovel-ready then it has already been funded. The infrastructure spending by the Federal government will just replace the funding that was already in place. This will produce zero stimulation.

- President Obama has vowed that there will be no earmarks. Who needs earmarks when the bill already has this much non-stimulating pork:

- $44 million for repairs at the Agriculture Department headquarters in Washington.

- $200 million to rehabilitate the National Mall.

- $360 million for new child care centers at military bases.

- $1.8 billion to repair National Park Service facilities.

- $276 million to update technology at the State Department.

- $600 million for General Services Administration to replace older vehicles with alternative fuel vehicles.

- $2.5 billion to upgrade low-income housing.

- $400 million for NASA scientists to conduct climate change research.

- $426 million to construct facilities at the Centers for Disease Control and Prevention.

- $800 million to clean up Superfund sites.

- $6.7 billion to renovate and improve energy efficiency at federal buildings.

- $400 million to replace the Social Security Administration’s 30-year-old National Computer Center.

- The tax rebates of $500 for individuals and $1,000 for couples will sail through unopposed. Just as the previous rebate checks were used to pay off debt, or saved, these rebates will not be spent. Therefore, we will have just transferred money from future generations to the current generation.

- The Federal Reserve will keep interest rates at zero, buy up bad assets from financial institutions, buy bad mortgages, buy Treasury bonds to artificially depress rates, and keep printing money until glorious inflation comes back to save the day. Everyone has faith that they will turn the spigot off in time. Their past record of seeing crucial turning points should give us all a sense of calm.

- Timothy Geithner has fired the first shot across the bow of China. He accused China of currency manipulation. Hopefully, this is just rhetoric. When you owe someone $500 billion and you need to borrow an additional $2 trillion in the next year it isn’t too smart to piss the lender off. Whiffs of trade restrictions and tariffs are reminiscent of Smoot-Hawley and the Great Depression.

Source: Wikiperdia

- Rather than scrapping the SEC, Congress will significantly increase their annual budget, hire more bureaucrats, and increase the regulations on businesses. Sarbanes Oxley has cost U.S. companies in excess of $1 trillion and has done nothing to make accounting more transparent. The lack of transparency is the main reason the financial system remains frozen today.

- Congress will hold hearings where they embarrass CEO’s, but will not prosecute anyone. They know that they are just as culpable in the financial disaster and would not want to shine too bright a light on the subject.

- The single biggest dilemma facing President Obama is something he has absolutely no control over. The American public has been traumatized over the last year. They have been misled by the government, lied to by Wall Street, and now they are losing their jobs by the millions. Their homes are worth 20% to 50% less and their retirement funds are worth 30% to 50% less. Consumer spending has made up 72% of GDP for the last few years. Based on the trauma they have experienced and having their illusions shattered that home price appreciation could fund their retirement and stocks will go up 10% per year, they have wisely begun to pay down debt for the 1st time in history.

- The combination of devastating losses to their net worth, miniscule retirement savings, and rapidly aging population will change the entire dynamic of U.S. society. Baby-boomers have been hit over the head with a shovel and it has knocked some sense into them. Fear is a great motivator. The government cannot influence this dynamic in any way. Americans will pay down debt for the next decade and increase their savings rate to 10% because they have to. They have no choice. They either reduce consumption and increase savings, or go hungry in their old age. This is the same conclusion that Japanese consumers came to in 1990.

Source: Mike Shedlock

We know what should happen and we know what will happen, but the ultimate result will be far different than the Japanese experience.  Owing to their large trade surpluses and high rates of saving, the Japanese have experienced a lethargic economy for two decades, but it has grown with relatively low unemployment in the 3% to 5% range for most of the two decades. They have been able to muddle through. The U.S. will refuse to muddle through. We still see ourselves as the leader of the world, and will not acknowledge the reduction in status that would transpire from a decade of reduced spending. America will choose to follow Neil Young’s advice that, It’s better to burn out, than to fade away.

Owing to their large trade surpluses and high rates of saving, the Japanese have experienced a lethargic economy for two decades, but it has grown with relatively low unemployment in the 3% to 5% range for most of the two decades. They have been able to muddle through. The U.S. will refuse to muddle through. We still see ourselves as the leader of the world, and will not acknowledge the reduction in status that would transpire from a decade of reduced spending. America will choose to follow Neil Young’s advice that, It’s better to burn out, than to fade away.

With an annual trade deficit of $700 billion, a National Debt that will surpass $12 trillion next year, a banking system that will need $2 trillion of additional capital, foreigners owning $3 trillion of our debt, zero percent interest rates and a weakening currency, something has to give. The Federal Reserve will do anything to defeat deflation. Deflation is fatal to a debt ridden society. There will be many more stimulus packages after this one fails. Eventually, we will reach a tipping point where too much debt will result in a hyperinflationary crash. It may be in two years or ten years. I don’t know. Ben Bernanke, Timothy Geithner, and Barrack Obama also don’t know. It will catch us all off-guard, just like the current crisis caught them off-guard. Turning Japanese would be a best case scenario for the U.S.

![]()

© 2009 James Quinn

Bio: James Quinn is a senior director of strategic planning for a major university. These articles reflect the personal views of James Quinn. They do not necessarily represent the views of his employer and are not sponsored or endorsed by his employer.

Turning Japanese – The Vapours

Sunday Bloody Sunday – U2