If We Can’t Get Oil from Mexico…

Courtesy of Lawrence Delevingne at Clusterstock

Courtesy of Lawrence Delevingne at Clusterstock

This was originally posted at The Oil Drum, and has been reprinted under the Creative Commons Attribution-Share Alike 3.0 United States License.

***

The news from Mexico just continues to get worse with bad news from all three of their biggest oil fields, even as our perennial cornucopian talks of “a Mexican surprise.” As Gregor noted recently (h/t ft energysource) at the beginning of the year Cantarell was producing 862,000 bd and at the end of July this was down to 588,000 bd. The graph plotting decline continues to show a linear decent at the rate of 35,000 bd per month or roughly 100,000 bd every three months – giving it just 17-months at that rate (ending right at the end of next year) until there is nothing left. Somewhere in there the drop is likely to stabilize, but suddenly and soon the questions as to where the replacement hundreds of thousands of barrels are going to come from is going to stop being an almost academic exercise.

The peak and decline of Cantarell – where Mexico once got most of its oil.

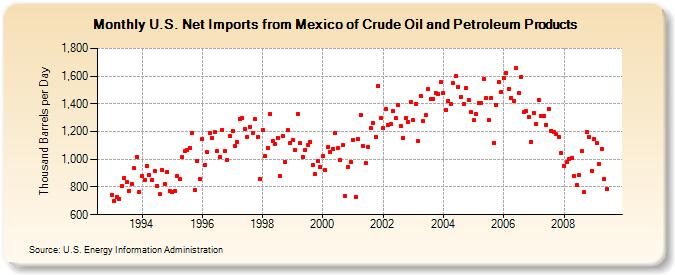

But they aren’t the only ones in trouble. Consider U.S. net imports from Mexico over the same period. That decline also looks pretty linear, with a projected intersection with zero in 2014, depending on where you draw the line.

Net Imports From Mexico (EIA)

Mexico itself is not likely to be able to come up with much of an answer.

The President just changed the head of Petroleos Mexicanos (Pemex) as the revenues that the state gets from sale of its oil (making up nearly 40% of the federal budget) dropped 30% in the first half of the year. Current Mexican Government predictions that overall Mexican production will stabilize at 2.5 mbd over next year don’t reflect the collapse of Cantarell, and also fail to recognize that the promised increases in production from other fields are not reaching the goals set. It is only a few days since the production at Chicontepec was “evaluated” after falling some 12,000 bd short of target. This field is still in development, with ultimate production targeted at 550,000 to 700,000 bd by 2017, but as it is already 16% behind the mark that does not augur well for that future.

As Euan Mearns pointed out the fields at Ku-Maloob-Zaap (KMZ) which lie adjacent to Cantarell are being produced in the same way as Cantarell, and thus production has recently risen dramatically.

Ku Maloob Zaap (KMZ) adjacent to Cantarell in the Gulf of Campeche is the largest source of new production growth. It recently overtook Cantarell as Mexico’s biggest producer, with record output of 814,000 b/d in April. The KMZ complex produced 740,000 b/d of crude in 2008, up from 550,700 b/d in 2007. Production has doubled in the last 3 years with a nitrogen reinjection program similar to one at Cantarell. Pemex expects KMZ production to peak at 820,000 b/d before declining to 810,000 b/d next year.

Read that last sentence again! Now the oil in KMZ is proving to be much heavier than that from Cantarell and so may not decline at quite the same rate, but given the very rapid increase in production, and that the peak is already here, this does not bode well for sustaining Mexican production using that region for any great period into the future. Rather it might increase the already precipitate drop in total production levels going into 2011.

Mexican exports of heavy crude (that from Cantarell and KMZ) had fallen, by July to 1.06 mbd from 1.22 mbd in January. Pemex had domestic sales of 1.8 mbd in July which is up some 45,000 bd from January, largely due to increases in sales of motor gasoline. The country imports some 550,000 bd of refined products.

If we go back to the Export Land Model, if internal demand continues to grow, and if Chicontepec proves to consistently fail to produce the needed production by as much as 20% or more (assuming that they are now working the best prospects first) and if we start to see the decline in KMZ next year . . . . . .

And to quote an “expert” on the subject:

Michael C. Lynch, president, Strategic Energy & Economic Research Inc., differs from the generally pessimistic consensus on Mexico. “I think Mexico will probably surprise many,” he said.

Lynch said, “[Pemex’s] first need has been capital; the government has a long tendency to starve them of money, and only recently has this been reversed. Mexican drilling activity is twice what it was a couple of years ago, and they have a lot of medium-sized fields that could make a serious contribution. (The decline in rigs rates has helped them, but the peso decline offset that somewhat). Deregulation and outside investment would certainly help, but capital is the main thing.”

Perhaps somebody could explain to Michael that when one uses the word “surprise” it generally means you’re going to hear good news – none of this is!