Freefall In Small Business Loans

Courtesy of Mish

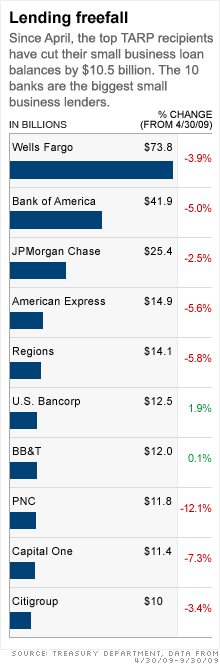

Eight months after President Obama began prodding the nation’s banks to increase their small business lending, the loan numbers continue to move in the opposite direction.

The 22 banks that got the most help from the Treasury’s bailout programs cut their small business loan balances by a collective $10.5 billion over the past six months, according to a government report released Monday.

Three of the 22 banks make no small business loans at all. Of the remaining 19 banks, 15 have reduced their small business loan balance since April.

Credit crunch: Obama administration officials, including Treasury Secretary Tim Geithner and Small Business Administration head Karen Mills, will host a forum Wednesday in Washington to discuss the lending challenges small businesses face. Bankers, members of Congress, and a selection of small business owners will participate.

While credit conditions have improved in some parts of the financial system, lending remains very tight for businesses that rely on banks for their financing, Federal Reserve Chairman Ben Bernanke acknowledged on Monday.

The article details the plight of Frank and Ingrid Brown who owns retail art and gift shops and wants to expand.

They applied for $35,000 in small business loans and "after filling out mountains of paperwork, the couple got a loan for $14,000 — less than half the $35,000 they applied for. Frank complained "By the time you get through everything, it is not even worth it."

They also applied for a $50,000 credit line and were only approved for $10,000.

So what is it they need, $35,000, $50,000, or $85,000? If I was a bank I would be extremely nervous about making loans to expand small retail gift shops in this environment especially when they want a large line of credit to go along with it.

Bear in mind we do not have all the facts, nor does the article. But these tales of woe are useless without the facts. I see no reason to believe this couple is a good business risk. Perhaps they are, perhaps they are not but my inclination is to side with the banks.

Pump Runs Dry

Flashback March 16, 2009 Obama: Pumping money into small biz

President Obama vowed Monday to ease the financial plight of the nation’s small businesses, which have been hit hard by the recession.

"Small businesses are the heart of the American economy," Obama said in a speech at the White House. "They’re responsible for half of all private sector jobs, and they created roughly 70% of all new jobs in the past decade. They’re not only job generators, they’re at the heart of the American Dream."

Many small businesses, drowning from dried-up coffers and unpaid bills, are having a tough time getting loans from lenders.

"Too many entrepreneurs can’t access the capital to start, operate or grow their business," Obama said. "Too many dreams are being deferred or denied by a form letter canceling a line of credit."

The stimulus bill allocated $730 million for direct spending on small-business programs, including expanded financial support for the SBA’s two key lending initiatives, the 7(a) and 504 programs. Under those programs, the SBA guarantees loans made by banks to small-business borrowers. If the business defaults, the SBA picks up the tab for the insured portion of the loan.

Supply Side Economics Lesson

The articles are presenting things from the supply side as if there is a supply problem (banks are refusing to lend and there is not enough money to lend). Yet, Keynesians and Monetarists in general can hardly moan about the supply of money.

The Fed Funds Rates is zero, Bank excess reserves are close to a $trillion, another $trillion is stimulus is floating around.

Combined, all this money could do is raise GDP estimates up to a now downward revised 2.5% (probably low-balled so we can beat the street by a couple tenths yet again).

See 3rd Quarter GDP +2.5% : Is That All? for details.

So Why Aren’t Banks Lending?

1) There are no credit-worthy businesses that want to borrow.

2) Consumers are tapped out and do not want to borrow.

3) Banks are scared to death of pending commercial real estate losses, credit card losses, residential real estate losses, home equity lines of credit losses, and losses in general.

4) Asset prices are simply too high (and banks know it) and the securitization market has dried up

Demand Side Economics

Let’s now take a look at the demand side of things.

It’s easy to find cases like the plight of the Brown family as noted above and trump up "Banks aren’t lending tales". But what if there are fewer credit-worthy businesses that want to borrow?

More to the point, what if in general, actual demand for small business loans is plunging?

Actually there is no "what if" there is simply "is".

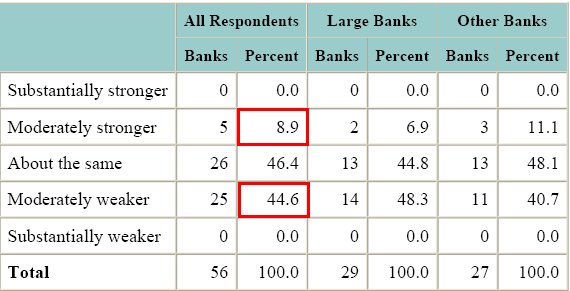

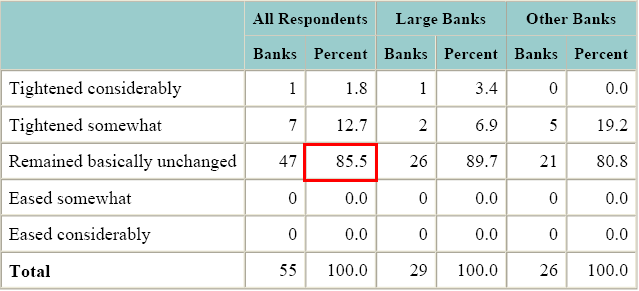

For proof, inquiring minds are digging for facts in the latest Fed Senior Loan Survey.

Please consider these charts.

Demand for C&I loans from small firms

Lending Standards For Small Firms

There you have it. 85.5% of banks responding to the survey have lending standards that basically remained the same yet 44.6% of banks report moderately weaker demand for loans, with only 8.9% reporting moderately stronger demand for loans.

There is plenty of money available for lending. However, there are fewer businesses wanting loans, and fewer still credit worthy businesses who want loans. That is what the data shows but it is not what is being reported.