96,000 Multifamily Housing Buildings in Chicago Area are Underwater ; 42 Percent of Small Rental Buildings at Risk of Default

Courtesy of Mish

Citing a DePaul University study, the Chicago Tribune reports More than 42 percent of small rental buildings in Cook County are ‘underwater’

Owners of 96,000 two- to six-unit rental buildings in Cook County are upside-down on $12.6 billion of mortgage debt, potentially putting 42 percent of small rental buildings in the county at risk of default, new data show.

A study by DePaul University’s Institute for Housing Studies, released Wednesday, also found that $3 billion in multifamily building mortgages already are in foreclosure, affecting more than 32,000 rental units in Cook County, or 6.8 percent of multifamily mortgages. That compares with about 38,000 single-family homes in foreclosure in Cook County.

Researchers analyzed 25,822 sales of existing small rental buildings and 591 sales of buildings with seven or more units in Cook County.

Multi-family foreclosure rate spikes in Cook County

Here are some additional facts in a Chicago Sun Times article Multi-family foreclosure rate spikes in Cook County

The foreclosure rate on multi-family rental properties in Cook County has spiked, and falling property values have put 30 percent, or more than $13 billion in Cook County’s multi-family mortgages at default risk, according to a study released today by DePaul University’s Institute for Housing Studies.

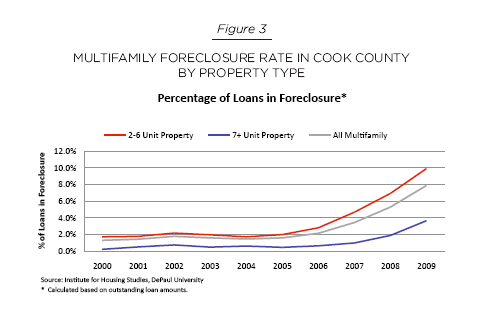

The report found that there are more than 32,000 rental units in Cook County impacted by foreclosures. The percent of loans in foreclosure on small two- to six-unit properties jumped to 8.75 percent in the fourth quarter of 2009 from 1.67 percent five years ago. On large seven-plus unit rental properties foreclosure rates jumped from 0.3 percent in 2004 to 3 percent in the fourth quarter of 2009.

For one in eight rental apartment units, revenues are falling below operating costs for owners. Owners of about 74,000 rental units in Chicago or 13 percent of the market, are currently spending more to operate buildings than they are collecting in revenues, placing them at significant risk of decreased or discontinued maintenance.

“The multi-family foreclosure crisis has not received as much attention as the crisis in the single-family housing market, but the trends outlined in this report demonstrate that it should,” study author James Shilling, chair of Real Estate Studies, said in a statement.

He added the problem is not just a Chicago issue, noting the same trends are happening in New York, Los Angeles, San Francisco, Phoenix, Atlanta and other cities.

Multifamily Housing Market Analysis

Inquiring minds are investigating the DePaul University Multifamily Housing Market and Value-at-Risk Study By James Shilling

Summary of Key Findings

- Prices of large (7+ unit) rental properties in Cook County have declined from an index value of 166 in the third quarter of 2006 to 123 in the second quarter of 2009, a decline of 26%. Prices of small (2–6 unit) rental properties in Cook County have fallen from an index value of 193 in the second quarter of 2007 to 104 in the second quarter of 2009, a decline of 46%.

- Falling property values in Cook County have put roughly $13 billion of multifamily mortgages (or approximately 30% of the total outstanding multifamily mortgage debt) at risk of default. Total value-at-risk for small 2–6 unit rental properties is $12.6 billion. For large 7+ unit rental properties, the total value-at-risk is $747 million.

- Falling property values have forced many lenders to “pretend and extend.” Lenders have delayed foreclosures on about $1.5 billion of multifamily mortgage debt in Cook County.

- As local lending institutions have scaled backed their lending to large 7+ unit properties in 2008 and 2009, Fannie Mae and Freddie Mac have essentially become indispensable to the Cook County multifamily mortgage market. The GSEs’ share of the large 7+ unit multifamily mortgage market in Cook County is around 65 to 70% of all lending. Fannie Mae and Freddie Mac are also indispensable to the small 2–6 unit multifamily mortgage market in Cook County, but for an altogether different reason.

- Net rental revenues are currently at or below total operating costs for about 74,000 rental units in the city of Chicago.

- Long-run policy must necessarily take into account the extent to which Fannie Mae and Freddie Mac subsidize interest and create an incentive to take on excessive debt.

Loan to Value Ratios for 2-6 Unit Properties

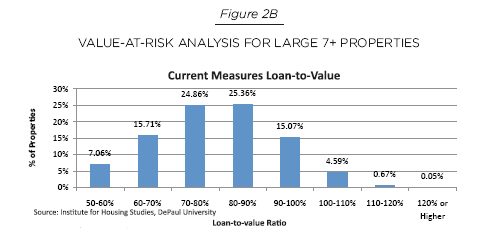

Loan to Value Ratios for 7+ Unit Properties

Multifamily Foreclosure Rates In Cook County

Multifamily GSE Originations

As is typically the case in such studies, the author’s proposed solutions leave much to be desired. Shilling discusses an expanded role for the FHA, I suggest shutting it down. Shilling discusses proposals for Fannie Mae and Freddie Mac, I suggest shutting them down.

To be fair, Shilling discusses the pros and cons of many ideas, including two paragraphs on Japan that hit the nail on the head.

Fannie Mae and Freddie Mac could be required to expand their multifamily housing lending, which already has been expanded under the 2010–2011 Enterprise Affordable Housing Goals. Expanding lending in these areas could be risky. But presumably the public should be willing to bear some of this increased risk, especially if this increased lending activity were to reduce the feedback effects in the short-run from falling property prices to increased foreclosures, back to reduced property prices and increased foreclosures.

But there are some caveats to this policy prescription: if the US economy were to stumble along for years—like Japan’s economy did during the “lost decade” in the 1990s—then presumably it would be best to accelerate foreclosures and abandonment, rather than take steps that might prolong the process. The sooner properties are removed from the housing stock, the sooner rents will begin to rise and the sooner the long-run equilibrium will be restored.

Property Tax Policy Exacerbates Problems

Glen who sent me one of the links writes …

Cook, Lake, and DuPage counties have some of the highest property tax rates in the nation, higher than California and parts of New York/New Jersey! By and large, these counties have so far refused to lower actual absolute tax amounts on individual properties consistent with the real decline in market value.

This situation that has effectively raised property tax rates for thousands of homes by 1%+ and translates into real annual tax rates of 2.5%-5% of actual market value!

This is a powerful and devastating anchor on rental property cash flows for every property rented in these counties regardless of the purchase price, financing terms, or rental management challenges that owners face.

Preventing Japanese Malaise

It should be obvious by now, that government interference in housing, especially the creation of Fannie Mae and Freddie Mac has been a total disaster. Going forward, the best approach would be to dismantle Fannie and Freddie in a reasonable timeframe, and let prices settle where genuine buyers will step up to the plate and invest.

Unfortunately, Shilling quickly discards that idea in favor of government intervention to prevent Japanese malaise. The sad thing is, government intervention is exactly what will guarantee Japanese style malaise.