As Apple’s market value explodes, questions abound…..(AAPL)

Courtesy of The Alpha Ninja

Brett Arrends of the Wall Street Journal has a must-read for anyone owning Apple (APPL) shares, titled "Seven Reasons Apple Shareholders Should Be Cautious." It pretty much implies to anyone invested in the stock market, as Apple is the S&P500’s second biggest weight, behind ExxonMobil.

I won’t list all 7 reasons Brett cites, but among the more important are:

5. The cellular networks. At what point will they stop giving away the store? Right now they’re paying most of the cost of each new iPhone, and under-charging for the data plans too. That’s great for customers and great for Apple, and bad for the networks.

3. The share price. At $260, Apple’s stock price has more than doubled in a year. Amateur investors say, "It’s going up." Present tense. Serious investors say, more accurately: "It has gone up." Past tense. No one knows the future. And the more it rises, the less attractive it gets. It’s now 20 times annual cash flow and 5 and a half times annual sales. At $235 billion, the company is being valued at more thanSony, Research In Motion, Dell, Motorola, Nokia, HTC,SanDisk and Palm … put together. That assumes a lot.

To the first point, I’m not in agreement. AT&T signs people up for a two year contract pulling in $70-120 per MONTH, on a device that sells for $500ish without a contract, and even that is only to protect the Apple "brand." If anything, networks could GIVE the phones away, with economics like that. Ever heard of a car that costs $30,000 to buy, but $$8,000 per month to USE? Neither have I.

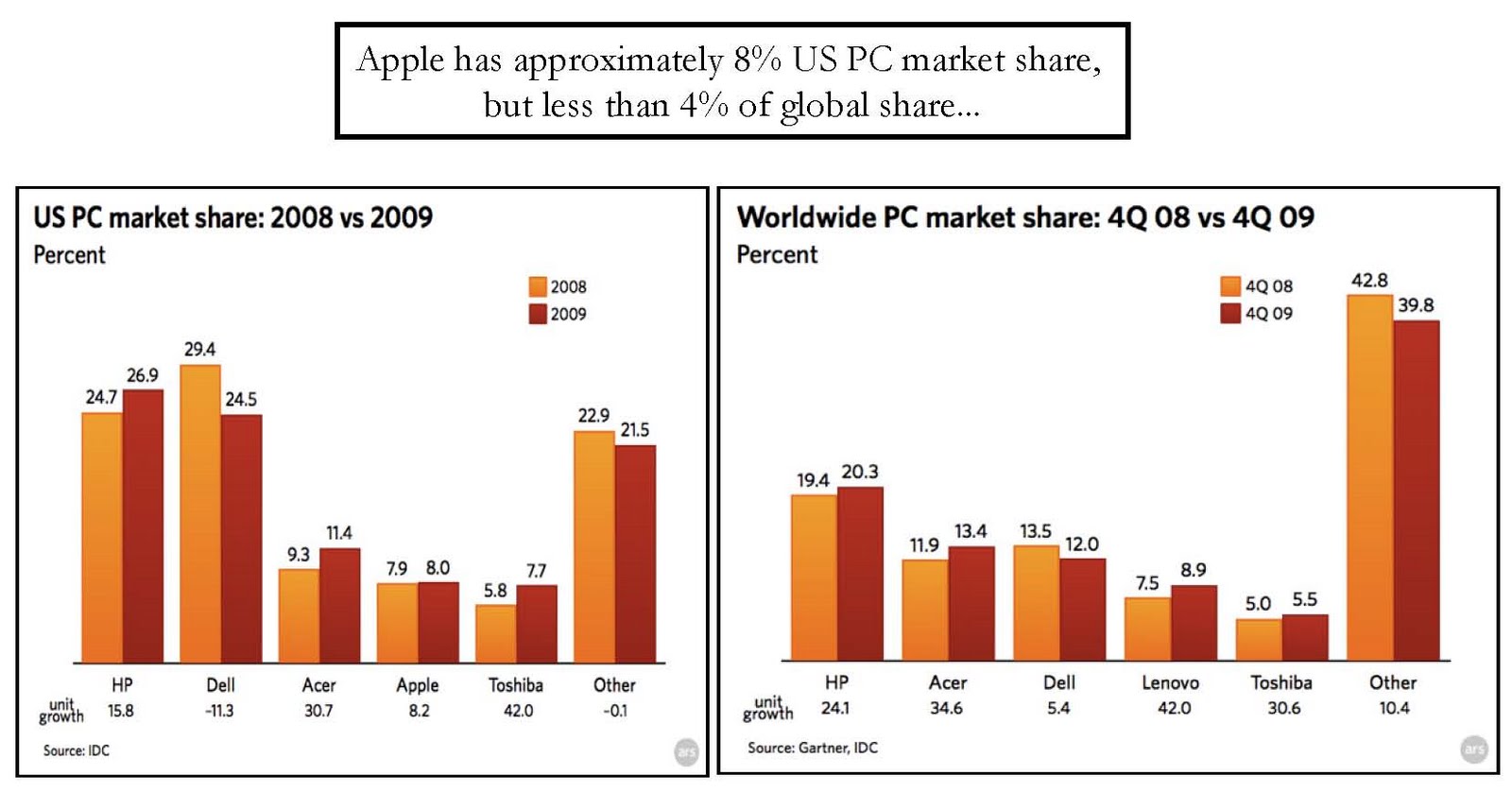

The second point is the bigger worry. At what point does the "law of large numbers" intervene, capping Apple’s market value? I simply don’t know. In the meantime, Apple’s market share in both the US and internationally only has to budge a little to have a huge impact for their profits. Critics cite Apple’s higher price points as a reason this can’t happen, but they forget how fast the iPod and iPhone’s went from uber-expensive to generally affordable.

Below is a chart that shocked me as I graphed it. It’s the top ten S&P500 companies by market value, in terms of market value per employee. Apple blows away even Microsoft, despite Apple being a HARDWARE maker…crazy:

It’s important to note of course, that estimates have climbed in part to changes in revenue recognition that previously delayed recognized iPhone revenue. But that doesn’t account for even half the increase in earnings estimates, so the point remains that as soon as we figure out a Price-to-Earnings ration for Apple, the earnings in that equation shoots higher. Net of $45 dollars in balance sheet cash & investments, Apple trades in the mid/low teens. I still like the shares and see them headed higher, but continue keep an eye on what we’re assuming…

Copyright 2010 AlphaNinja