Introduction, courtesy of Michael Panzner of Financial Armageddon, ‘Who Benefits?’

It’s not often that I highlight material from the same blog more than once over the course of a few days or weeks. But then again, there are not too many commentators who are as thoughtful and insightful as Charles Hugh Smith, author of Survival+ and publisher of Of Two Minds blog, a long-time favorite of mine. Last time around, he gave us a no-holds barred assessment of the so-called recovery. In "The Root of the Housing Bubble Remains Unchanged," he suggests, among other things, that for many people, there’s little to gain — and lots to lose — from pursuing the traditional American dream.

The Root of the Housing Bubble Remains Unchanged

Courtesy of Charles Hugh Smith

Courtesy of Charles Hugh Smith

Banks and Wall Street profited immensely from millions of unqualified home buyers reaching out for the simulacrum of middle class "ownership."

The fundamental root of the housing bubble–the collusion of the Central State and banks to extend home ownership to millions of citizens who did not qualify for that burden– remains firmly in place.

The Federal government continues to pour tens of billions of dollars into this "home ownership should be for everyone" project via subsidies to Fannie Mae, Freddie Mac and FHA. Mortgage lenders have been delighted to write mortgages in our completely nationalized market in which the government backs literally 99% of all mortgages and the Federal Reserve bought $1.2 trillion in mortgages that no sane private investor would touch.

Fannie Mae seeks $8.4 billion from government after loss: Fannie Mae, the largest U.S. residential mortgage funds provider, on Monday asked the government for an additional $8.4 billion after the company lost $13.1 billion in the first quarter.

Because of current trends in housing and financial markets, Fannie Mae expects to continue having a net worth deficit in future periods and to need to tap more funding from the Treasury.

"Promoting sustainable homeownership and maintaining ready access to liquidity are our guiding principles in serving the residential markets," said Michael Williams, the firm’s chief executive.

The government has relied heavily on both companies, which buy mortgages from lenders to stimulate more lending, to stabilize the housing market.

In other words, the housing market would collapse without this massive Federal support, and there is no end to the losses this subsidy will require. Propping up the nation’s fundamnetally insolvent housing market is truly a financial black hole.

Meanwhile, the default rate on low-down-payment FHA loans is a staggering 20% on loans written in 2008–after the housing bust had already unfolded and the risk was undeniable: F.H.A. Problems Raising Concern of Policy Makers:

F.H.A. commissioner, David H. Stevens, acknowledged that some 20 percent of F.H.A. loans insured last year — and as many as 24 percent of those from 2007 — faced serious problems including foreclosure.

The Federal government has thus shown that it is so committed to propping up an unsustainable policy and housing market that it is ready to write off 1 in every 4 mortgages within a year of origination.

The problem with that willingness to absorb risk for the sake of incentivizing borrowing for home ownership is that next year another 20% will default, and then the following year another 20% will default, and by year Five the vast majority of those loans backed by FHA will be in default.

FHA Facing "Cataclysmic" Default Rates:

The Federal Housing Administration (FHA) has guaranteed about 25% of all new U.S. mortgages written in 2009, up from just 2% in 2005.

The key phrase here is "borrowing," not "home ownership." The key feature of State support of housing is not legitimate "home ownership," it is the enabling of massive new sources of income and transactional churn for lenders and Wall Street loan and derivatives packagers.

Home "ownership" when there is no equity in the purchase and no equity being built via principal payments is a simulacrum of ownership.

If a buyer puts almost no money into the purchase–even now, FHA and VA loans can be had with a mere 3% down payment–and the loan is of the interest-only or adustable-rate (ARM) variety favored during the housing bubble’s heyday, then there is no principal payment being made and thus no equity being built.

These "buyers" don’t "own" anything; all they’re doing is renting the money in the hopes that rising home prices will create equity for them out of thin air. What they "own" is essentially an option on a property which they "rent" monthly. If the government manages to reinflate the housing bubble (it won’t, but hope and greed spring eternal), then the option will pay off handsomely. The "owner" put no money into the speculative bet, but they can then sell their option for a huge profit.

If housing plummets, then the "bet" was lost. But since "renting" the mortgage didn’t cost much more than renting a real house, and there was no capital at risk, then the downside is modest indeed.

In other words, heavily subsidized mortgages at low rates with little money down incentivizes not home "ownership" but speculation in credit-based bubbles.

In the "old days" (circa 1994), the expectation was that equity would be built by paying off the mortgage principal over time. Equity was a result of reducing the mortgage due, not the result of speculative gambling on future asset bubbles.

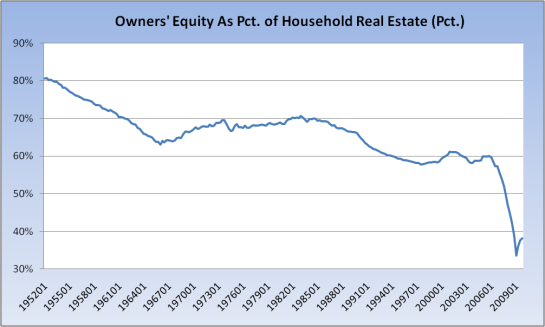

The FDIC foresaw the risks of the subprime mortgage gambit to extend "ownership" of a mortgage back in 2006, when they issued this chart.

As I noted in Housing and the Collapse of Upward Mobility (April 16, 2010), according to the Census Bureau, the U.S. has 51,487,282 housing units with a mortgage and 23,875,803 Housing units without a mortgage as of 2008.

As I go on to document in that entry, massive equity extraction and credit-based speculative purchases of homes has had a disastrous consequence to home equity: there is only about $1 trillion–a mere 1.85% of the nation’s total net worth– of equity left in the 51 million homes with mortgages.

So much for the progressive-sounding goal of extending home ownership to all: the pernicious consequence is that equity has been all but wiped out for mortgage holders.

Let’s ask cui bono of this "home ownerhsip should be for everyone" policy: who benefitted? Certainly not the "owners," most of whom have either been wiped out (some 25% of "owners" have negative equity, and this probably understates reality), or who are left with shreds of equity which won’t survive the next downturn in housing prices.

Who benefitted? The mortgage lenders, banks and Wall Street debt packagers.While undoubtedly some do-gooders in Washington were convinced that home ownership was the key feature of middle class wealth, events have proven their belief to be tragically in error.

The key feature of middle class wealth is thrift, not massive leveraged debt. What Washington and its financial Power Elite partners presented as "the road to middle class wealth" was in fact a mere chimera, a simulacrum of the road to middle class wealth. That road is fiscal prudence and thrift.

Immigrants have prospered in the U.S. for generations because they were thrifty and sacrificed for their children by sweating blood to save money for college educations and for 20% down payments on homes. They did not prosper by snagging Central State supported mortgages with no down payment on homes they could not afford under any prudent calculation of risk.

From this point of view, the entire "home ownership is for everyone" policy was a gigantic fraud, a con job sold to an American public greedy for a short-cut to middle class wealth. The bankers and the Central State government both profited immensely, as the bankers and Wall Street minted tens of billions in profits off the mortgage machine and its derivative spin-offs, and the government (at all levels, Federal, state and local) gorged on billions of dollars in transfer fees, capital gains taxes and the sales taxes on all the gewgaws home "owners" bought to fill up their new McMansions.

Back in 2006 (when I’d already been covering the coming housing bust for almost two years), the FDIC reckoned 5% of home "owners" were at risk of default. 5% of 75 million is 3.75 million. As near as I can calculate from these media accounts, (Homes in foreclosure rose 79% in ’07, Record 3 million households hit with foreclosure in 2009), about 4 million mortgages have already been foreclosed.

So the "at risk" "buyers" are gone. Their "bet" on future housing appreciation has been lost.

But 14% of all mortgages are still in default, (about 7 million) which suggests that rather than being drained, the foreclosure pipeline is full to bursting.

I addressed this more fully in The Foreclosure Pipeline Is Full.

The basic problem which cannot be solved is that the entire housing policy was founded on two presumptions which are both failing: prosperity (jobs) will grow forever, and housing values will rise forever.

The policy did not consider the possibility that household income and wealth would actually decline, and that housing valuations would decine by substantial amounts, year after year.

The housing subsidy policy was in effect a speculative scheme in which a simulacrum of "ownership" was extended on the faith that rising income and house prices would make good that bet. Now that assumption has been revealed as false; incomes and house prices are both in structural declines, yet the Federal government is insisting on issuing hundreds of billions of dollars in new "options" (simulacra of ownership) in the vain, absurd hope that issuing enough speculative bets will actually re-inflate the housing bubble and thus bail out the banks, Wall Street, Federal revenues and the hapless marks who bought into the con.

But issuing leveraged options is not the same as creating capital or equity. Thus the government’s plan of reflating the housing bubble will fail.

Let’s take a look at home ownership rates over the past century. As we can see, prior to the Federal government’s massive subsidy of housing via 3% down payments and guaranteed mortgages, ownership hovered at around 45% of households. Clearly, home ownership (the real thing, not a simulacrum) was not for everyone for the simple reason less than half the populace could afford to buy a home when a substantial down payment and private lending were required.

I know this sounds "impossible" (just like it was "impossible" for stocks and housing to crash) but what if the government is forced to repudiate its housing policy and ownership falls from 67% to 47%?

According to the Census Bureau ( home ownership rates), there are 111 million occupied dwellings, 19 million vacant dwellings (of which only 6-7 million are truly vacation/second homes), and 75 million owner-occupied homes.

Even after 4 million foreclosures, that puts home ownership at 67%.

If the entire edifice of mortgage subsidies (which result in 20% default rates) collapses under its own weight, and home ownership (the real thing) declines to 47% of households, that would leave about 52 million owners and 59 million renters.

Since 24 million home owners already own their houses fee and clear (without mortgages), then that implies that mortgage holders would decline from 51 million to 28 million.

Would that really be such a terrible thing for the nation? How beneficial is the current simulacrum of home "ownership" anyway, when a pathetic 1.8% of the nation’s wealth is spread amongst 51 million home "owners" staggering under unprecedented debt? Can that even be called "ownership"? What exactly is "owned" other than a call option on future bubbles?

What is owned is the debt–by banks and "investors," all backed by Federal guarantees. Who would suffer from the end of this perverse subsidy of a false "ownership" is Wall Street and the big mortgage lenders, who would see the pool of mortgage money diminish to what the private debt market would support.

All those fat transaction fees, the re-financing fees, the plump profits from home equity lines of credit, the enormous profits booked from packaging mortgages and writing derivatives against them–all gone.

As I wrote in Survival+, always start by asking cui bono: to whose benefit?

Here are a few of the dozens of entries I’ve written over the past 5 years on the housing bubble/bust:

Housing Wealth Effect Shifts Into Reverse (May 2, 2006)

Will Delinquencies Trigger a New American Revolution? (April 7, 2008)

Can 4% of Homeowners Sink the Entire Market? (February 21, 2007)

Housing and the Paradox of Credit Bubbles, Equity and Demand (March 29, 2010

Picture credit: Jr. Deputy Accountant