Atlanta Fed asks: How "Discouraged" are Small Businesses?

Courtesy of Mish

The Federal Reserve Bank of Atlanta Asks How "Discouraged" are Small Businesses? Here are some Insights from an Atlanta Fed small business lending survey.

Roughly half of U.S. workers are employed at firms with fewer than 500 employees, and about 90 percent of U.S. firms have fewer than 20 employees. While estimates vary, small businesses are also credited with creating the lion’s share of net new jobs. Small businesses are, in total, a big deal.

Many people have noted the decline in small business lending during the recession, and some have suggested proposals to give incentives to banks to increase their small business portfolios. But is a lack of willingness to lend to small businesses really what’s behind the decline in small business lending? Or is it the lack of creditworthy demand resulting from the effects of the recession and housing market distress?

We at the Federal Reserve Bank of Atlanta have also noted the paucity of data in this area and have begun a series of small business credit surveys. Leveraging the contacts in our Regional Economic Information Network (REIN), we polled 311 small businesses in the states of the Sixth District (Alabama, Florida, Georgia, Louisiana, Mississippi and Tennessee) on their credit experiences and future plans. While the survey is not a stratified random sample and so should not be viewed as a statistical representation of small business firms in the Sixth District, we believe the results are informative.

Indeed, the results of our April 2010 survey suggest that demand-side factors may be the driving force behind lower levels of small business credit. To be sure, when asked about the recent obstacles to accessing credit, some firms (34 firms, or 11 percent of our sample) cited banks’ unwillingness to lend, but many more firms cited factors that may reflect low credit quality on the part of prospective borrowers. For example, 32 percent of firms cited a decline in sales over the past two years as an obstacle, 19 percent cited a high level of outstanding business or personal debt, 10 percent cited a less than stellar credit score, and 112 firms (32 percent) report no recent obstacles to credit.

Perhaps not surprisingly, outside of the troubled construction and real estate industries, close to half the firms polled (46 percent) do not believe there are any obstacles while only 9 percent report unwillingness on the part of banks.

Banks Want To Lend

The report should bury the idea that banks do not want to lend.

Outside of the overbloated construction industry, businesses simply do not want to expand. With rising health care costs (Please see Double Digit Health Insurance Hikes Crush Small Businesses), and with excess capacity and tepid consumer spending why should businesses expand.

Now let’s take a closer look at the Atlanta Fed Small Business Credit Report.

Reasons for Not Seeking Credit

Excluding construction and real estate only 5% of businesses thought credit terms were unfavorable, and only 13% thought lenders would deny the request. Bear in mind the numbers add up to greater than 100% because the survey allowed multiple responses.

28% said sales did not warrant expansion, and 26% said they simply did not need credit. A whopping 37% said they had sufficient cash and another 34% said existing credit lines were sufficient. There may not be much overlap in those last two categories.

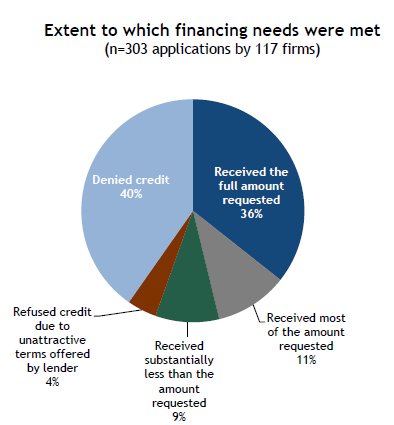

Extent to Which Financing Needs Were Met: Applications

From the report: A total of 122 applications (40%) were denied, but only 22 of the 117 firms that sought credit were denied on all applications they attempted. Thus, 81% of firms seeking credit received credit at some level.

Obstacles to Accessing Credit

Excluding construction and real estate, of those denied credit, only 9% said the "bank was unwilling to lend". Across all industries the total was only 11%.

The moral of the story is as I have stated many times over the past two years. Banks are willing to lend but credit-worthy businesses do not want to borrow. Indeed businesses in general do not want to borrow.

Of the 9% of business owners who blame the banks, how many of those do you think need to look in a mirror and admit a failing business? I suspect all of them.