Amedisys shares tumble 23% on earnings drop, Market Watch

Kudos to Sam Antar for the warning on this stock! – Ilene

Recall:

Open Letter to the Securities and Exchange Commission: Investigate Troubling Issues at Amedisys Missed by Wall Street Journal

Courtesy of Sam Antar of White Collar Crime

To Securities and Exchange Commission Chairperson Mary Schapiro:

On June 30, 2010, Amedisys (NASDAQ: AMED) announced that it "received notice of a formal investigation from the Securities and Exchange Commission (SEC) pertaining to the company, and received a subpoena for documents relating to the matters under review by the Senate Finance Committee." The SEC investigation follows an April 2010 Wall Street Journal report questioning Amedisys’s Medicare reimbursement patterns and raising serious questions about possible abuse by the company of Medicare’s reimbursement system. In mid-June 2010, several class action lawsuits were filed against Amedisys alleging securities fraud, based on the Wall Street Journal report.

In my analysis below, I will provide additional troubling data and issues missed in the Wall Street Journal report and not cited in the various class action lawsuits for the SEC to consider in its investigation.

Background

The analysis is based entirely on information derived from Amedisys’s public disclosures in various reports filed with the SEC. Those reports provide certain statistical information about Medicare episodic, non-Medicare episodic, and non-Medicare/non-episodic home health care visits, admissions, and recertifications for each reporting period.

Amedisys further categorizes that data by base/start-up entities and acquired entities for each reporting report. Amedisys defines Base/Start-up agencies as agencies that were originally opened by the company and acquired entities owned by the company for at least a year.

Therefore, the analysis below is based almost entirelry on Amedisys’s statistical data for base/start-up agencies to provide a consistent apple-to apples comparison of the data.

Note: Download entire work sheet here (formatted for legal sized paper).

What explains the sudden increase in the growth of in base/startup Medicare episodic visits per admission?

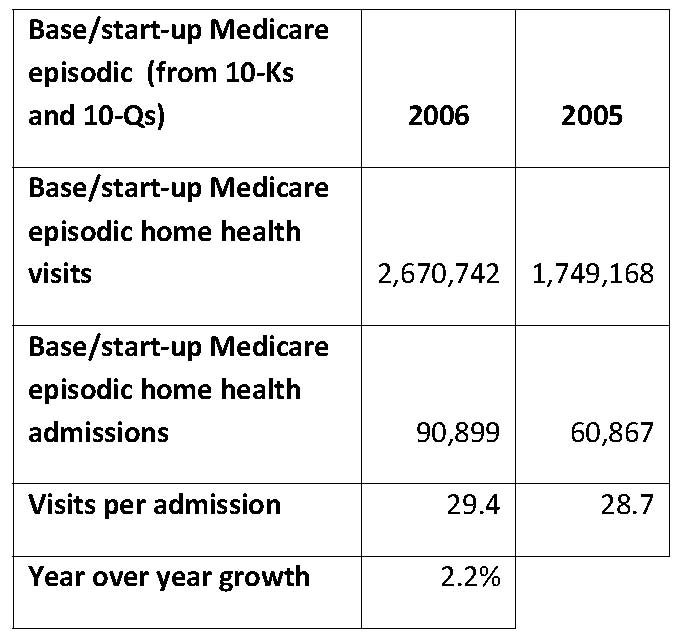

Prior to Q2 2007, Amedisys reported fairly typical (i.e., moderate) growth in visits per Medicare episode. For example, during 2006, the number of visits per Medicare admission for base/start-up agencies increased to 29.4 visits per admission from 28 visits per admission in 2005, or a 2.2% increase over the previous comparable period. See the chart below:

Similarly, in Q1 2007, base/start-up Medicare episodic visits per admission declined to 29.1 visits per admission compared to 29.4 visits per admission in Q1 2006 or a 1.2 decrease from the previous year comparable period. See the chart below:

Starting in Q2 2007, however, the amount of base/start-up Medicare episodic visits grew much faster than admissions. By Q3 2009, base/start-up agencies reported an increase to 36.5 visits per admission, an all time-high for the company. See the chart below:

Why did the number of visits per Medicare admission at base/start-up agencies suddenly begin increasing at such dramatic rates starting in Q2 2007?

Why did recertifications skyrocket in 2007?

Looking more closely at data provided in company filings, it appears that the increase in visits per admission was driven mostly by an increase in recertifications and recertifications per admission. Recertifications occur when a provider receives permission from Medicare, based on a doctor’s request, to provide another “episode” of care.

Note: Comparable was data not available for base/start-up Medicare episodes. Therefore, the chart above includes combined amounts for base/start-up and acquired entity Medicare episodes.

According to Amedisys, the number of Medicare recertifications grew 51.07% from the first half of 2007 to the first half of 2008. Yet admissions increased just 42.72% in that same period. What could cause such a discrepancy?

Why visits per Medicare admission suddenly begin declining in Q4 2009?

In Q4 2009, base/start-up Medicare episodic visits per admission suddenly began to decline, falling to 35.2 visits per admission compared to 36.5 visits per admission in Q3 2009, It was the first Q4 v Q3 sequential decline in base/start-up Medicare episodic visits per admission since 2006. See the chart below:

And in Q1 2010, base/startup Medicare episodic visits per admission declined to 33.7 visits per admission compared 35.2 visits per admission in the preceding Q4 2009 period and 34.4 visits per admission during the comparable Q1 2009 period. Thus, Amedisys reported its first decline in comparable prior year base/start-up Medicare episodic visits per admission since Q1 2007. See the chart below:

What explains this sudden trend reversal and does it have anything to do with the onset of scrutiny by journalists (such as the Wall Street Journal) or analysts (such as Citron Research)?

Amount of base/start-up Medicare episodic visits per admission is much higher than non-Medicare episodic visits per admission, despite similar reimbursement rates and procedures

In reviewing Amedisys’s filings, I was also struck by the gap between visits per Medicare admission and visits per admission for other payors. Visits per admission are greatest for base/start-up Medicare episodic, second greatest for non-Medicare episodic, and smallest for non-Medicare non-episodic.

For example, during 2009, I calculated that there were 35.3 Medicare episodic visits per admission compared to 29.6 non-Medicare episodic visits per admission and 22.7 non-Medicare non-episodic visits per admission.

In 2009, Medicare episodic visits per admission were 19.2% higher than non-Medicare episodic visits per admission and in 2008 Medicare episodic visits per admission were 24.5% higher than non-Medicare episodic visits per admission. See the chart below:

One might argue that differences in reimbursement procedures explains the above gap. Yet, according to Amedisys, non-Medicare episodic visits are reimbursed in a “similar manner” to Medicare episodic visits. See disclosure from the company’s 2009 10-K report below:

Payments from Medicaid and private insurance carriers are based on episodic-based rates or per visit rates (non-episodic based) depending upon the terms and conditions established with such payors. Episodic-based rates paid by our non-Medicare payors are paid in a similar manner and subject to the same adjustments as discussed …for Medicare; however, these rates can vary based upon negotiated terms.

If both base/start-up Medicare episodic and non-Medicare episodic visits are reimbursed “in a similar manner” why do Medicare episodic visits per admission far exceed non-Medicare episodic visits per admission?

Ratio of base/start-up Medicare episodic recertifications to admissions is much higher than non-Medicare episodic recertifications to admissions despite similar reimbursement rates

Likewise, the ratio of recertifications to admissions is greatest for base/start-up Medicare episodic treatment, second greatest for non-Medicare episodic treatment, and smallest for non-Medicare non-episodic treatment. See the chart below:

I also find it interesting that, during 2008, the ratio of recertifications to admissions for Medicare cases handled by base/start-up agencies was over 100%. See the chart below:

Then, during 2009, the ratio of recertifications to admissions fell dramatically, particularly after Q1. For the full year (2009) it was 93.7% versus 100.3% the year prior (2008). See the chart below:

What explains the substantial decline in recertifications to admissions, particularly after Q3 2009? And did it have anything to do with increased scrutiny of the company’s published financial disclosures?

Sudden resignation of two high level executives coincides with the recent declines in visits and recertifications per Medicare admission. Is it purely coincidental?

On September 3, 2009, Amedisys President and COO Larry Graham and Alice Ann Schwartz, its chief information officer, suddenly resigned from the company. Amedisys provided no reason for their resignations and simply said that the two execs “are leaving the company to pursue other interests.”

In my experience, sudden, unexpected executive departures are often a sign of problems beneath the surface. And while it could be entirely coincidental, the trends at Amedisys appear to be consistent with my experience.

After the sudden resignation of Graham and Schwartz, the ratio of Medicare episodic recertifications to admissions dramatically dropped from 96.3% in Q3 2009 to 89.3% in Q4 2009 and to just 81.7% in Q1 2010. The number of visits per Medicare admission also began to decline, as I described earlier.

In the months before Graham’s sudden departure from Amedisys, he unloaded over $2.6 million of stock. Was it shrewd timing in anticipation of a run to the exits before the fire bell sounded? In my world, I don’t believe in coincidences.

Written by:

Sam E. Antar

Disclosure:

I am a convicted felon and a former CPA. As the criminal CFO of Crazy Eddie, I helped Eddie Antar and other members of his family mastermind one of the largest securities frauds uncovered during the 1980’s. I committed my crimes in cold-blood for fun and profit, and simply because I could.

If it weren’t for the efforts of the FBI, SEC, Postal Inspector’s Office, US Attorney’s Office, and class action plaintiff’s lawyers who investigated, prosecuted, and sued me, I would still be the criminal CFO of Crazy Eddie today.

There is a saying, "It takes one to know one." Today, I work very closely with the FBI, IRS, SEC, Justice Department, and other federal and state law enforcement agencies in training them to identify and catch white-collar criminals.

Recently, I exposed financial reporting violations by Overstock.com (NASDAQ: OSTK) as an independent whistleblower. The Securities and Exchange Commission is now investigating Overstock.com and its CEO Patrick Byrne for securities law violations (Details here, here, and here).

In addition, the SEC is now investigating possible GAAP violations by Bidz.com (NASDAQ: BIDZ) after I alerted them about the company’s inventory accounting practices.

I do not own Overstock.com, Bidz.com, or Amedisys securities long or short. My investigation of those companies is a freebie to securities regulators to get me into heaven, though I doubt that I will ever get there. In any case, no good deed ever goes unpunished by the SEC. That’s life. I do not seek or want forgiveness for my vicious crimes from my victims. I plan on frying in hell with other white-collar criminals for a very long time.

Sam’s Antar’s opinions represents those of Sam Antar, and not the opinions of or endorsed by Phil’s Stock World.