Bernanke’s Conflict of Interest

Courtesy of Bruce Krasting

I, and a few thousand others, have been bashing the Fed on a nearly daily basis. But actually we should be dishing out some praise for a job well done. $76b still goes a pretty long way these days. The even better news is that in 2011 the Fed will make us even more money than last. Way to Go Ben B! Here’s how they made the long green:

A graph of the Fed balance sheet as of 9/30. The total balance sheet comes to a modest $2.2 trillion. The net income generated from all these holdings is the $76b estimated by the CBO:

The net income number comes to an interest spread on the portfolio of 3.45%. There are some folks in the portfolio management business who would die for that result. The Fed did it the easy way. They borrowed money at no cost thanks to ZIRP.

We know the Fed is going to be buying in more paper during 2011. Jon Hilsenrath at the WSJ tells us that just about every day. If you don’t believe him just read the Fed minutes. QE-2 is baked in the cake. The leaks and guesses suggest that we are looking at another Trillion of POMO buys over the next year. The thinking is that the Fed will acquire a portfolio with an average maturity of around seven years. The yield on that maturity today is about 1.8%. Based on that a pro-forma look at the Fed BS a year out:

This quick calculation overstates income and average yield. The reason is that a significant amount of high coupon MBS will be prepaid over the course of the year. Given that a primary objective of QE-2 is to reduce mortgage costs and therefore encourage refinancing at lower rates I am going to assume a high prepay rate that will result in $300b of reduction in the MBS portfolio. The adjusted estimates for the portfolio as of 10/1/2011:

When I look at this I conclude that the Fed will Not raise the Funds target to 3% for many years to come. To do so would imply that they would incur an annual loss. No one wants losses. When you have losses you are a squeaky wheel. In D.C. they don’t oil squeaks. They investigate them and put collars on the problem. No one at the Fed would want that.

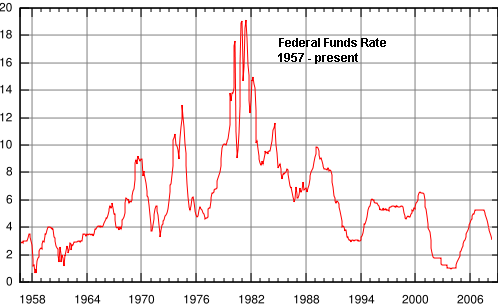

Here is a chart of Funds rate up to 2008. It does not include the madness of ZIRP. I would call this “normal”. We had extreme highs to fight inflation and we have had several periods where rates where well below average. But look at this chart and tell me where a 2.75% break even rate comes into play. For the past 70 years we have been above that level 90+% of the time.

Mr. Bernanke’s sole objective with monetary policy at this point is to create inflation. Given that he is hell bent for leather on this I think we will get want he is engineering. And like every other historical Fed effort they will overshoot on stimulus and inflation will come back at some point. But Bernanke will not have the balls to pull the trigger on Fed policy and tighten as he may have to. To do so would straddle him with big losses.

The Fed is creating a conflict of interest between its own institutional best interests and the proper choices for monetary policy. That is the definition of a systemic risk. Bernanke needs to address this conflict. I want him on the record acknowledging the risks of what he has done and is about to double up on:

The Fed commits to all interested parties that it will act in all future periods consistent with its mandate for stable prices. Should circumstances arise that require a rapid tightening of monetary policy the Fed would act accordingly and ignore the consequences to its own financial position. Should this occur substantial and sustained losses would be incurred. The Fed accepts in advance the full consequences of its actions.

Of course we will never hear these words or anything close to it. That is why most people do not trust QE and believe it will end badly. For the record, the annual cost to the Fed assuming a Federal Funds rate rise at some point (keep in mind that we were at 5.5% just three years ago):