Asset Inflation/Deflation: The Fed’s QE2 vs. $15 Trillion in Losses

Courtesy of Charles Hugh Smith, Of Two Minds

Given that the economy faces $15 trillion in writedowns in collateral and credit, the Fed’s $2 trillion dollars in new credit/liquidity is insufficient to trigger either inflation or another speculative bubble.

"Don’t fight the Fed" is supposed to be a strong argument for being bullish on the U.S. economy and stocks. We all know the Federal Reserve is about to unleash a torrent of money into the financial markets via its QE2 (quantitative easing) campaign of buying Treasury bonds directly and pulling various other monetary levers to open the liquidity gates.

But before we succumb to the excitement that accompanies the unleashing of the Fed’s supernatural powers, perhaps we should look at some numbers first.

Size of U.S. economy: $14 trillion. Probable size of QE2: $1 trillion. That means QE2 is perhaps 7% of GDP. Even a whopping $2 trillion QE would equal about 14% of GDP.

In contrast, by some measures China opened the floodgates of credit to the tune of fully 35% of their GDP to combat the contraction caused by the global financial meltdown in late 2008: China’s Creative Accounting.

How much collateral and credit will be destroyed as the U.S. economy rolls over into recession/depression in 2011-14? Based on the latest (September 17, 2010) Fed Flow of Funds, here is my back-of-the-envelope estimates of losses yet to be booked in assets (collateral) and credit (debt):

1. Residential real estate: current value, $18.8 trillion. Estimated value in 2014: $13.8 trillion, i.e. a decline of $5 trillion or 26%. If all impaired mortgages are written down or sold for fair market value, I am guessing the full $5 trillion will need to be written off by somebody, somewhere.

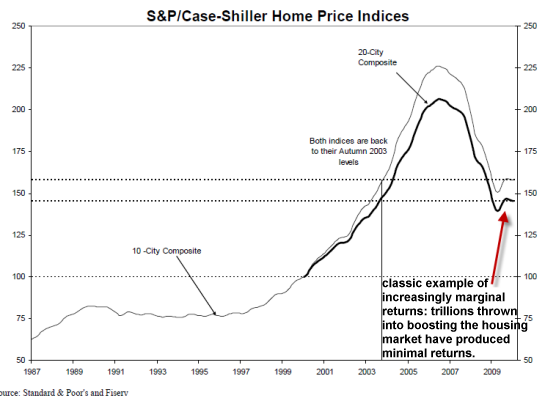

My 26% estimate is conservative; according to the Case-Shiller Index chart, a decline of 40% would be required to return the index to the year-2000 level.

2. Commercial real estate (CRE): The Flow of Funds only reports "nonfarm nonfinancial corporate business" so the CRE number of $6.5 trillion is a few trillion light (that is, we need to add in CRE owned by financial corporations). I am estimating writedowns of $3 trillion–a number others have also guesstimated.

Empty malls, empty office parks, empty warehouses, empty retail: they’re all worth essentially zero. The cost of bulldozing them is higher than their auction value.

3. Consumer durable goods: All this "stuff" is supposedly worth $4.5 trillion, but when the millions of bulging storage units are emptied and sold, the actual market value of all this will be more like $3 trillion at best. So knock off another $1.5 trillion in collateral.

4. Corporate bonds: A huge steaming pile of junk bonds have been sold in the last year, bonds which will be four paws to the sky once inflated profits and corporate balance sheets adjust to the 2011-14 reality. Let’s tag the losses here at $1 trillion, which is probably conservative.

5. U.S. stocks: Roughly $14 trillion: $6.7 trillion owned outright, $4 trillion in mutual funds and another $4 trillion in pension funds (which total about $11.6 trilion total). Once skyhigh estimates of future profits fall to Earth and the risk trade fades, then equities will get a $4 trillion haircut (i.e. they are about 30% overvalued).

Investors are already exiting equities as an asset class (once burned, twice shy, and they’ve been burned twice in 8 years) and the next downturn will accelerate this prudence:

6. Equity in noncorporate business: The Fed sets this at $6.6 trillion, and as the economy rolls over, households and business deleverage their massive debts and taxes rise, then a fair accounting of this non-publicly-traded equity would probably drop by at least $1 trillion.

I consider each of these estimates to be conservative, and they total $15 trillion.The Fed estimates total assets of households and nonprofits (which is of modest size compared to households) at $67 trillion, and net worth at $53 trillion (that is, liabilities are "only" $14 trillion).

A reduction in collateral of $15-$20 trillion (including the $3 trillion in CRE losses) would still leave tens of trillions in assets. But it would certainly impair the economy’s ability to leverage up trillions more in new debt.

Rather, uncollectible, impaired or defaulted debt would have to be written down or written off. Those holding the debt–the "too big to fail" banks–would be bankrupted by these reductions in collateral.

This is an essential function of classic Capitalism–"creative destruction" and the disavowal of uncollectible or impaired debt.

So how do you generate the "modest inflation" which is the Fed’s stated goal when $15 to $20 trillion in collateral and credit are disappearing from balance sheets? How do you goose credit enough to inflate a new asset bubble?

Well, I suppose you could create $15 trillion out of thin air and try to get households and businesses to borrow it, but that still wouldn’t create the demand for goods and services which undergirds the real economy.

The Fed might make $15 trillion in new credit available and the only people wanting to borrow it are speculators within the Financial Power Elites who can rig the markets in their favor.

Gee, that sounds like the present. Did all that previous QE solve any of the economy’s structural imbalances? No, it simply bathed balance sheets with the magic of "extend and pretend."

Excessive debt and speculative bubbles cannot be "fixed" with additional doses of debt and speculation. The Capitalist reality is this: if the Fed truly wanted to fix the U.S. economy rather than protect its over-extended, debt-ridden Financial System, then it would force the liquidation of trillions in bad debt and force a "marked to market" valuation on every balance sheet, household and corporate alike.

Instead, we have the "don’t ask, don’t tell" method of calculating asset values.

Anyone who believes a meager one or two trillion dollars in pump-priming can overcome $15-$20 trillion in overpriced assets and $10 trillion in uncollectible debt may well be disappointed.

The Fed’s tinny little QE "bazooka" will be rolled over by the M-1 tanks of deleveraging and the recognition of $15-$20 trillion in losses.