Is it Wednesday already?

What a fun week we've been having. I had told Members when we were looking forward in the weekend post: "Wednesday is a biggie with Mortgage Applications, Challenger Job Cuts, ADP Jobs Report, Productivity and Unit Labor Costs, ISM, Construction Spending, Oil Inventories, Auto Sales AND the Fed Beige Book, which I think may show optimism building into the holidays (as they want to spin it that way) so, if we are going to get a push up, Wednesday should be the day." Well, it's 7:15 and it looks like we're peaking out at 1% in the futures. Europe is up 1.5% at noon.

Yesterday's very poor finish to November left us in no mood to go bullish into the close and we'll probably be shorting this open as I'm just not seeing any real news out of Europe to justify this rally so I have to think it's entirely a relief rally that's pushing the Euro higher ($1.31) along with the Pound $1.56 while the Dollar drops to 80.80 and that's down 0.6 from yesterday's close and we generally have a 1.5x negative correlation so there's your "rally" named in just one note. We pulled our longs and went back to cash in the $10K-$50K Virtual Portfolio with another $300 gained on the day and that's on track (up $1,000 on day 2), but we still have $1,500 at risk on the bear side so we'll be a little nervous if the Dollar can't hold 80.50. Overall, I'm still very pleased with my October call to get to cash and this morning Bloomberg decided to congratulate me, saying:

The dollar proved to be last month’s best investment, beating stocks, bonds and commodities, confounding officials around the world who said Federal Reserve policies would debase the U.S. currency. The U.S. Dollar Index, which tracks the currency against those of six major U.S. trading partners including the euro, yen and pound, rose 5.2 percent in November. The Thomson Reuters/Jefferies CRB Index of 19 commodities was little changed. The MSCI All Country World Index of stocks fell 2.2 percent after accounting for reinvested dividends. Bonds lost 1.1 percent including reinvested interest as measured by Bank of America Merrill Lynch’s Global Broad Market Index.

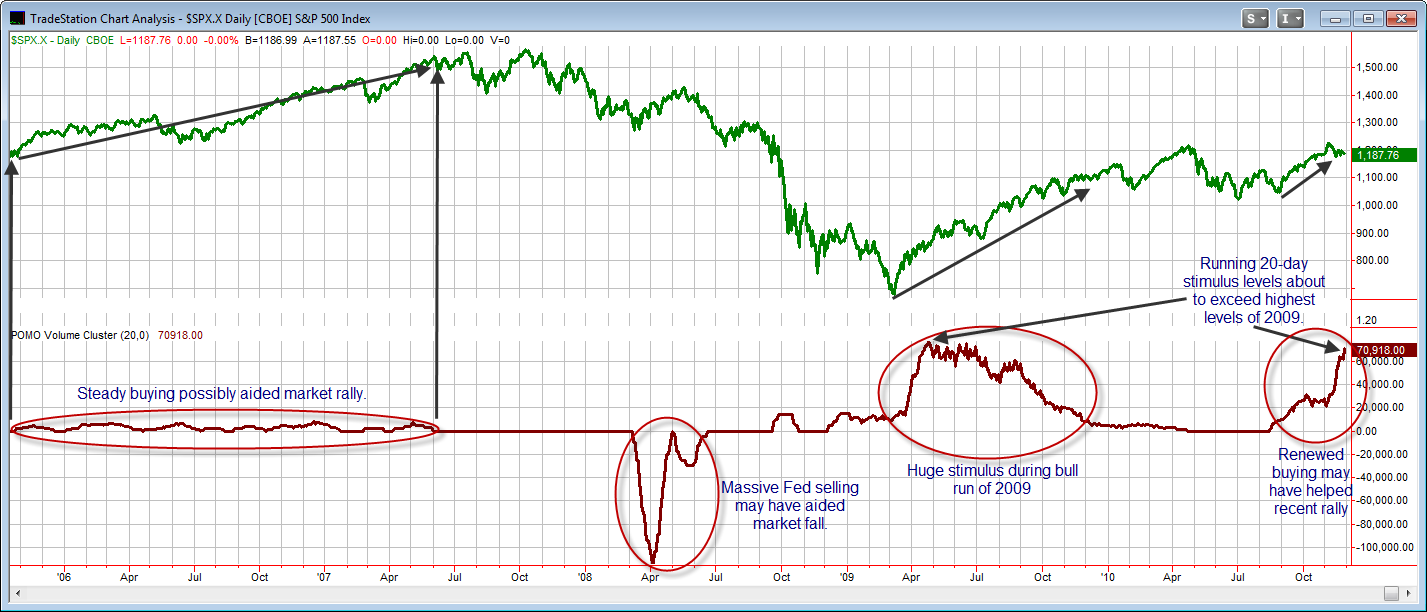

The Fed is certainly doing their best to push us higher and here's a great chart that shows you EXACTLY how that works. QE2 inflationary pumping is our SOLE bullish premise on the markets at this level but so far, so lame as far as the market's reaction to an even bigger stimulus than we had in April and we're not even holding our highs – what happens when this round is over? Well, probably there will be another one because investors are like children and the Fed is like an overly indulgent parent who can't stand to see us cry and they've already moved us from low-rate candy to quantitative liquor and now it's QE2 crack they are providing to give us a quick fix – I'm sure Uncle Ben is cooking up some speed-balls for QE3 because that's just good parenting, isn't it?

If we don't wind up economically dead in an alley, it's going to be a wild ride – that's for sure! We're watching several levels and today's bounce goals for our indexes are Dow 11,120, S&P 1,195, Nasdaq 2,525, NYSE 7,550 and Russell 735 – if we can hold those, then POMO fever may be more than just a passing phase and we can start taking a serious look at our breakout levels again and the Russell has never really lost the faith (which is why they are a key downside hedge for us) and hopefully we'll have the opportunity to take those QID calls we missed an opportunity on yesterday, when the Nasdaq gapped down at the open.

Once we have some high-leverage downside protection, we'll be ready to look up again. That's why we like to take bearish hedges as we test our upsides – they give us a solid floor we can play aggressive longs off. We did add a few long trade ideas in Member Chat yesterday, of course, as we always do a little bottom-fishing on a good down-turn. Today we'll be looking for an opportunity on QID, TZA and USO to go short (I mentioned shorting oil at $86 yesterday and they fell all the way to $83.70 into the NYMEX close, now back to $85.50 on the weak dollar) while, at the same time, probably looking at FAS again to go long.

The big pump in Europe today was caused by what is being considered softening language in Jean-Claude Trichet's testimony to the Euro Parliament, which suggests future bond purchase decisions were "on-going" as opposed to "off the table" as had been the previous case. Trichet has that Greenspan quality where the market's move based on the slightest nuance in his statements. Our Fed, on the other hand, has made it clear that they will gladly put this nation into 1,000 years of servitude to foreign debt-holders no matter what the economy actually looks like, which is why we can rally despite strong ADP Numbers (+93,000 jobs), that would logically suggest (along with other positive data) that the Fed should be easing up on the free money express.

The big pump in Europe today was caused by what is being considered softening language in Jean-Claude Trichet's testimony to the Euro Parliament, which suggests future bond purchase decisions were "on-going" as opposed to "off the table" as had been the previous case. Trichet has that Greenspan quality where the market's move based on the slightest nuance in his statements. Our Fed, on the other hand, has made it clear that they will gladly put this nation into 1,000 years of servitude to foreign debt-holders no matter what the economy actually looks like, which is why we can rally despite strong ADP Numbers (+93,000 jobs), that would logically suggest (along with other positive data) that the Fed should be easing up on the free money express.

But everybody loves FREE MONEY and President Obama and the Republicans both hinted that we may get more of it in the form of extended tax cuts – just like the ones that doomed us less than a decade ago – isn't that special? FREE MONEY allows us to ignore the 16.5% drop in Mortgage Applications last week despite the fact the 30-year note hovered around 4.5%. And yes, that includes an adjustment that takes Thanksgiving into account! Refinances were down 21.6% for the week, the lowest level since June when our market took a dive.

That's pretty much in-line with the dreadful Case-Schiller numbers we saw yesterday and it does look like we're heading to a double-dip in housing but, hey – don't let that stop you from buying PCLN! We were short PCLN but took that trade off the table on yesterday's dip as we are still very much in "take the money and run" mode on both long and short plays. Challenger Job Cuts jumped to 48,711, the highest level in 8 months, indicating big corporations are not done downsizing. Why should they be with Q3 Productivity up another 2.3% and Unit Labor Costs down 0.1%. It's a perfect jobless recovery – well, jobless in America anyway, US corporations are still hiring tons of people in Asia! Marcroeconomic Resilience put it very well yesterday, saying:

Although corporate profitability is not at an all-time high, it has recovered at an unusually rapid pace compared to the nonexistent recovery in employment and wages. The recovery in corporate profits has been driven by a rise in worker productivity and increased efficiency but the lag between an output recovery and an employment recovery seems to have increased dramatically. So far, this increased profitability has led not to increased business investment but to increased cash holdings by corporates. Big corporates with easy access to debt markets have even chosen to tap the debt markets simply for the purpose of increasing cash holdings.

Again, incumbent corporates are eager to squeeze efficiencies out of their current operations including downsizing the labour force but instead of channeling the savings from this increased efficiency into exploratory investment, they choose to increase holdings of liquid assets. In an environment where incumbents are under limited threat of being superceded by exploratory new entrants, holding cash is an extremely effective way to retain optionality (a strategy that is much less effective if the pace of exploratory innovation is high as an extended period of standing on the sidelines of exploratory activity can degrade the ability of the incumbent to rejoin the fray). Old jobs are being destroyed by the optimising activities of incumbents but the exploration required to create new jobs does not take place.

This discussion of profitability and unemployment echoes many of the common concerns of the far left. This is not a coincidence – one of the most damaging effects of Olsonian cronyism is its malformation of the economy from a positive-sum game into an increasingly zero-sum game. The dynamics of a predominantly crony capitalist economy are closer to a Marxian class struggle than they are to a competitive free-market economy.

This isn't new stuff people – that cartoon is 100 years old and we fought against the evils of corporate greed and won at some point but now they've changed tactics and moved onto taking over government and brainwashing the masses so the American people now confuse the good of the corporation with their own welfare when they are, almost by definition – diametrically opposed. As I've said since November, when you people voted the same idiots back into office who destroyed the country in the first place – I wash my hands of it, you get the Government you deserve but it does still make me angry as I haven't completely lost my liberal nature as I try to pursue the path of true capitalism and just get mine while the getting's good – so forgive the occasional flash of conscience I may still show from time to time – I am trying my best not to give a damn about the bottom 99% – just like our leaders!

Jobs are booming in Asia and Chinese workers there are getting raises as China's Manufacturing PMI increased to 55.2 in November. That would be fantastic except the Input Price Index rand up to 73.5, another indication that China has a long way to go to get inflation under control but HBC considers it "manageable," which is code for "keep giving us money." The Hang Seng gained 1.1% this morning but the Shanghai held flat while India put up an impressive 1.7% gain, trumping the Nikkei's 0.5%. I mentioned Europe earlier and the Euro is up 1.15% against the dollar at the moment (9 am) but the dollar is holding that 80.50 line so far. The CAC is up 1.3%, the Dax is up 2.2% on Trichet Fever and the FTSE is up 2% as Chancellor Osborne does a victory lap, congratulating the Brits for NOT being part of the Euro, saying: "I feel that our view has been vindicated by recent events – I'm very pleased the U.K.'s not part of the euro."

Jobs are booming in Asia and Chinese workers there are getting raises as China's Manufacturing PMI increased to 55.2 in November. That would be fantastic except the Input Price Index rand up to 73.5, another indication that China has a long way to go to get inflation under control but HBC considers it "manageable," which is code for "keep giving us money." The Hang Seng gained 1.1% this morning but the Shanghai held flat while India put up an impressive 1.7% gain, trumping the Nikkei's 0.5%. I mentioned Europe earlier and the Euro is up 1.15% against the dollar at the moment (9 am) but the dollar is holding that 80.50 line so far. The CAC is up 1.3%, the Dax is up 2.2% on Trichet Fever and the FTSE is up 2% as Chancellor Osborne does a victory lap, congratulating the Brits for NOT being part of the Euro, saying: "I feel that our view has been vindicated by recent events – I'm very pleased the U.K.'s not part of the euro."

How's that for a ringing endorsement of global economic health? Europe is simply ignoring the 9% drop in Carrefour, the World's 2nd largest retailer, who are plunging after reporting weak performance across Europe as well as costly write-downs in its Brazilian stores. Carrefour has lost market share in France since September after competitors opened more stores, while price deflation “is evidently pressing margins.” According to their CEO: An increasingly competitive environment in France, as well as economic weakness in Europe cited by the company suggest Carrefour may struggle to retain the benefit of its cost-cutting initiatives. That is why the CAC is lagging the FTSE and DAX but this is not just a French problem.

I think the entire XRT (Retail Index) is due to come under pressure as non-stop sales lead to margin squeezes. I mentioned last week that we know the promotions are out of control when my 8 year-old daughter comes home from school and tells me how important Black Friday is. All it will take is another small child (perhaps my 10 year-old because nobody listens when I say it) to point out the the Retail Emperor has no margins on clothing to knock this whole sector back to the low $40s. The Jan $44 puts are just .95 and should be less than that if we have a silly pump open so that will be my Free Trade Idea of the week. We'll see how it goes…

Trichet has to do more than just talk to keep a lid on the crisis in Europe and we still have plenty of issues here at home that need to be addressed like Nevada getting their ratings outlook cut to negative by Moodys based on declining gaming revenues – the same ones that LVS and WYNN are making new highs in anticipation of.

We are up based on the hope Trichet begins dropping Bernanke-sized wads of money from helicopters and we're up based on the hope that Obama, the Democrats and the Republicans will all sing Kumbaya and quickly pass another round of massive tax breaks (because the first one worked sooooo well) which we hope will boost the economy and we hope all that happens before any countries, states or banks go bust and, of course, we hope all the positive retail numbers we are hearing will extrapolate out to something in the vicinity of justifying our massive market rally.

Hopefully yours,

– Phil