Courtesy of Mish

Borrow-short lend-long strategies have caused more pain and grief than nearly any play in the book. They are virtually guaranteed to blow up given enough time if the duration mismatch and leverage is too great.

For those who do not know what I am describing, a couple examples below will help explain. The first example is a look at "cost of funds" and guaranteed profits that banks can make. It is not a borrow-short lend-long strategy but will morph into such a scheme as I vary the parameters.

Citigroup CDs

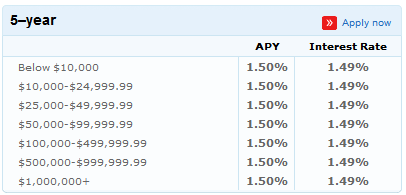

Inquiring minds investigating Citigroup’s cost of funds note that Citigroup 5 year CDs yield a mere 1.5%. For this example, Citigroup’s cost of funds is 1.5%, the rate it pays depositors. Here are a few snips from Citi’s website.

Who said there are no guarantees in life?

Some things in life are a sure thing. Like a Citibank CD, which offers a guaranteed—and highly competitive—interest rate. You also get a wide range of terms, from 3 months to 5 years.

Guaranteed Ripoff

Citigroup has the gall to brag about "guarantees in life" when the "guarantee" in question is a complete ripoff. It’s a ripoff because 5-year US treasuries currently yield 2.35%.

Anyone buying CDs at less than the treasury yield rate is a fool.

Rates at Bank of America, Northern Trust, JPMorgan Chase

I will tie this together shortly, but first make note that the Northern Trust, Bank of America, and JPMorgan Chase offer even lower 5-Year CD rates.

Here are some rates courtesy of Bankrate.Com as of 2011-02-15.

According to Bankrate, national average for 5 year CDs is 1.61% and the rock bottom low is .95%. The site average is 1.98% and the top yielding 5-year CD yields 2.75%. Thus Citigroup’s claim of competitive rates is absurd.

Although Bank of America makes no such claims, its CD rate is priced so preposterously low, that Bank of America must not even want to deal with them. Alternatively, B of A has an incredibly large pool of moronic depositors begging to be ripped off.

Guaranteed Free Money

Anyone buying 5-year CDs from Citigroup, Bank of America, Northern Trust, or JPMorgan Chase is giving those banks a shot at guaranteed free money.

All those banks have to do is take that money and invest in 5-year US treasuries to have a guaranteed profit. Here are the reasons for that statement.

- There is no duration mismatch. The banks secure funding for 5 years and invest that money for 5 years.

- The US government is not going to default no matter what nonsense you may hear elsewhere.

Purists may point out the play is not entirely risk-free because people can pay a penalty, cash out the CD, then take the money elsewhere. However, from a practical standpoint, fools dumb enough to accept 1.5% or lower are probably not bright enough to pay a penalty and take the money elsewhere even if rates dramatically shoot up.

Borrowing-Short and Lending-Long

Please note that those 5-year CDs are borrowed money. Banks have to pay that money back plus interest (pathetic interest in this case) to the depositor. Banks keep those deposits on the book as a liability.

However, what if the banks borrowed money for 5 years and lent it out for 21 years? Perhaps banks could get 4% interest on those loans (much higher if they assume more risk), but what if interest rates 5 years from now are 6%?

All that has to happen to turn this scheme into a guaranteed loss for the bank is for the cost of funds (CDs, savings accounts, or borrowing from the Fed), to rise above the rate the bank lent that money out.

Borrowing-short and lending-long thus poses a significant risk if interest rates raise. Moreover, duration mismatch and rising cost of funds are not the only risks. Banks also need to lend at a rate sufficiently high to cover default risk.

To be fair, banks can hedge the risk of rising rates, but then one must ask "who is the counter-party to that hedging risk, and what happens if they blow up?"

The Next Borrow-Short Lend-Long Guaranteed to Blow Scheme

With the discussion about duration mismatch out in the open, please consider Banks Go Straight to Public Borrowers

Banks are setting aside billions of dollars to do something that until now was rarely heard of: making big loans to cities, states, schools and other public borrowers that otherwise might have turned to the bond market.

When Riverside, Calif., was ironing out a bond offering recently to expand its performing-arts center, several banks pitched a radical idea: Why not take out a loan instead? The city scrapped the bond plan and borrowed $25 million from City National Bank in Los Angeles.

"This was a method we’d never even heard of before," says Scott Catlett, the city’s assistant finance director. He says Riverside now intends to seek a bank loan for a conference center that it had planned to build with bonds.

J.P. Morgan Chase & Co. is devoting billions of dollars to direct loans this year to both refinance deals and for new projects, according to a bank official. Last year, the bank made a few hundred million dollars of direct loans to municipalities. Now, the bank would consider making a single loan for hundreds of millions of dollars, the official said. It also is dispatching teams to explain the concept to wary public borrowers.

Citibank also is courting municipal borrowers with direct loans, according to several bond issuers. A spokesman for the Citigroup Inc. unit declined to comment.

"This used to be unheard of," says Eric Friedland, managing director of public finance at Fitch Ratings, noting that in the past, banks would occasionally loan a municipality less than $1 million to finance projects too small for a bond offering. For bigger loans, they would form a syndicate with other lenders.

It remains to be seen what land mines may be lurking for lenders and borrowers. Some municipalities are going through significant struggles, raising questions about whether they will prove good credits. And direct loans are less liquid, meaning banks can’t sell them as easily as bonds.

For banks, this is a potentially lucrative business at a time when they are sitting on cash that isn’t earning huge interest and are reluctant to make loans for mortgages and other areas they see as risky.

In the event of a bankruptcy, analysts say, it is unlikely that a bank extending a direct loan would be given priority over bondholders.

The city saved hundreds of thousands of dollars in issuance costs, says Mr. Catlett, the assistant finance director. Plus, he says, the interest rate is 3.85% versus at least 5% if it had floated a public offering. The term is slightly lower—21 years versus perhaps 30 years in the bond market.

"This was all new to us," he says. "I don’t know now when we’ll go back to the bond market. This is easier."

Fed or FDIC Should Stop this Fraudulent Scheme Now

The Fed or FDIC should step in right now. There is no way banks can secure cost of funds for 21 years for 3.85%. Moreover, the risk of default is hardly zero, and banks will not be first in line should default happen.

I think borrowing-short and lending-long is fraudulent. How can you lend something for 21 years when you only have the right to use it for 3, 5, or 7?

Want to know what those banks thinking? This is what ….

- They are too big too fail

- The Fed will bail them out

- Cities won’t default but who cares anyway because the Fed will bail them out

- They have a hot pile of cash the Fed crammed down their throats at 0% and they want to put it to use

- They got burnt badly on mortgages and home equity loans so they need to find something new

- One idiot bank made an absurdly risky deal so like sheep they all want to do it

Right now they are all thinking there is nothing to lose from this. The Fed or Congress will bail them out at taxpayer expense if they get in trouble.

Then, when this does get out of control and blows sky high, they will all scream, "no one could possibly have seen it coming".

Addendum:

For a follow-up post with further discussion including an email from a reader about someone being taken advantage of by B of A, please see Bank of America Preys on Elderly Depositors; Culture of Greed, Arrogance, Incompetence.