Courtesy of Bruce Krasting.

At one point or another, all the big name politicians have indicated they would support changing the minimum Early Eligibility Age (EEA) rules for Social Security. Obama has said it, so has Boehner. Even guys who love Social Security, like Sen. Harry Reid, thought it might be okay. Many economists have publicly opined that raising the EEA for benefits is good economics, as the average life expectancy is higher than it was forty years ago. To me, the most significant evidence that a consensus is forming on this important issue is the fact that the ultimate supporter of the Grey Panthers, the AARP, came out with its support last year.

I think that all of these deep thinkers are wrong. In fact, a good case can be made for lowering the minimum retirement age from 62 to 60. From the Congressional Budget Office report on the consequences of increasing the Early Eligibility Age (EEA):

If that doesn’t convince you, consider these words:

Budgetary Effects

The budgetary effects of a rise in the EEA in the short term would be different from those over a longer period. Federal outlays would decline in the short term because people would have to wait until they were older to apply for Social Security benefits. Over time, higher subsequent monthly benefits would offset an increasing share of the savings from delayed eligibility.

How is it possible that all of the folks pushing for an increase in the EEA could be wrong on this issue? Intuitively it makes sense. Delaying the age for benefits should reduce expenses for SS and therefore save it money, thus keeping it solvent for longer. It sounds so simple. Why doesn’t it work?

The answer is that increasing the EEA won't improve the finances of Social Security (or the country as a whole). SS discounts the amount payable if early retirement is opted for. It is calculated so that SS is “expense neutral” if benefits are taken at today’s EEA of 62 years versus the higher benefits available by waiting until 64 years.

The following formulas are a simplified look at how this works:

Case #1

Benefits payable at age 62 = $1,000 per month

Average Life / (years of benefits)= 78 / (16 years)

Total life time benefits = $192,000

Case #2

Benefits payable at age 64 = $1,142

Average Life / (years of benefits) = 78 / (14 years)

Total life time benefits = $191,856

The formula that SS uses to discount benefits for those seeking payments prior to their Full Retirement Age (FRA) is quite simple:

The reductions are based on the month of claiming: A benefit is reduced by 5/9 of 1 percent for each of the first 36 months before the FRA.

For example, if a man was expecting a monthly check of $1,000 at FRA, he would receive $810 monthly if they took benefits three years earlier. This simple formula immunizes SS from the cost of those seeking benefits early.

I hope that this discussion proves the point. There is no economic consequence to SS (or to the overall fiscal position of the US) from raising the EEA. Now consider what would happen if the EEA were to be lowered from age 62 to 60 years.

Using the same 5/9th% monthly discount rate, the individual who seeks benefits at age 60 would get a check 13% less than what he would have received by waiting until he was 62 to quit working. Using the formula from above:

Case #3

Benefits payable at age 62 = $1,000 per month

Benefits payable at age 60 = $870 per month

Average life (years of benefits) = 78 / (18)

Life time benefits = $188,000

Note: The $188,000 number above does not take into consideration the time value of money and changes in payments of Disability Benefits. When these factors are built into the equation, the numbers between the various ages of retirement all equal out.

Today, approximately 60% of eligible beneficiaries elect to get their SS checks at age 62 (EEA). I can't’ accurately project how many people would elect to retire at age 60 or 61, if it were possible to get discounted benefits at earlier ages. I think it's a large number.

Of the 3.6mm individuals who will get new SS benefits this year, 2.2mm (60% of total) are getting their checks upon reaching the EEA. If the EEA were lowered to age 60, how many people would take advantage of the change? Given that there are two years worth of individuals who would be eligible for reduced benefits, an estimate for the number of people who might opt-in to early retirement, if given the chance, is between zero and 4.4mm. For the sake of discussion, call it 2mm. That would be very helpful.

What would this do for the economy? It would shrink the supply of available workers. It would happen fairly quickly over the course of the first two years that the EEA adjustments became effective. As older workers leave the workforce earlier, the demand for younger workers would increase. People at all ages (including older workers not seeking to retire) would “move up the ladder” faster. There would be more new job openings for younger workers coming into the labor force.

High unemployment is corrosive to society. It’s particularly problematic when the shortage of jobs creates very high rates of unemployment for young workers. High youth unemployment is the scourge of Europe today. Total unemployment in some of these countries is around 10%, but youth unemployment is over 20%. The situation is similar in the USA. The numbers have not yet reached the levels in Europe, but the trend in the USA is firmly in place. If nothing is done, the likely outcome is for youth unemployment north of 20% in the USA.

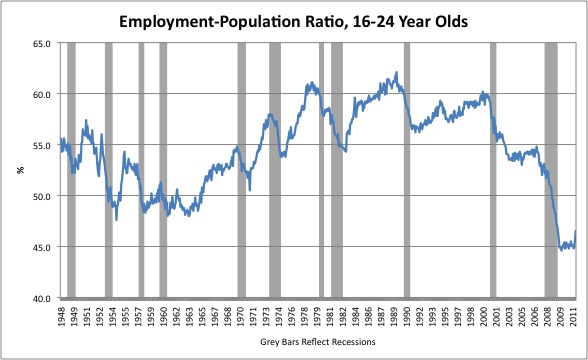

Based on the information provided by the CBO, I think it should have analyzed changing the EEA down (as well as up). Lowering the EEA would be neutral to the long-term finances of both SS and the country. It would also open up a few million jobs. Many of those jobs would be entry level positions. Just what we need. This chart illustrates the problem we face. Employment for younger workers is currently at a post WWII low.

I can’t figure out why the CBO didn’t consider the implications of a reduction of the EEA. A team of analysts must have worked on the report for weeks. But they only looked “inside of the box”; the CBO needs to look “outside of the box” to find options for the issues we face.

Note: The CBO also looked at raising the Full Retirement Age (FRA) from 67 to 70. This is a different kettle of fish than increasing (or decreasing) the EEA. This approach would benefit SS. But it would have a range of negative consequences as well. I’ll discuss increasing the FRA in a separate post. Enough on SS/CBO for one day.

{kind=link}