{kind=link}

Entering the Intervention Zone

Courtesy of Bruce Krasting

One Around Two

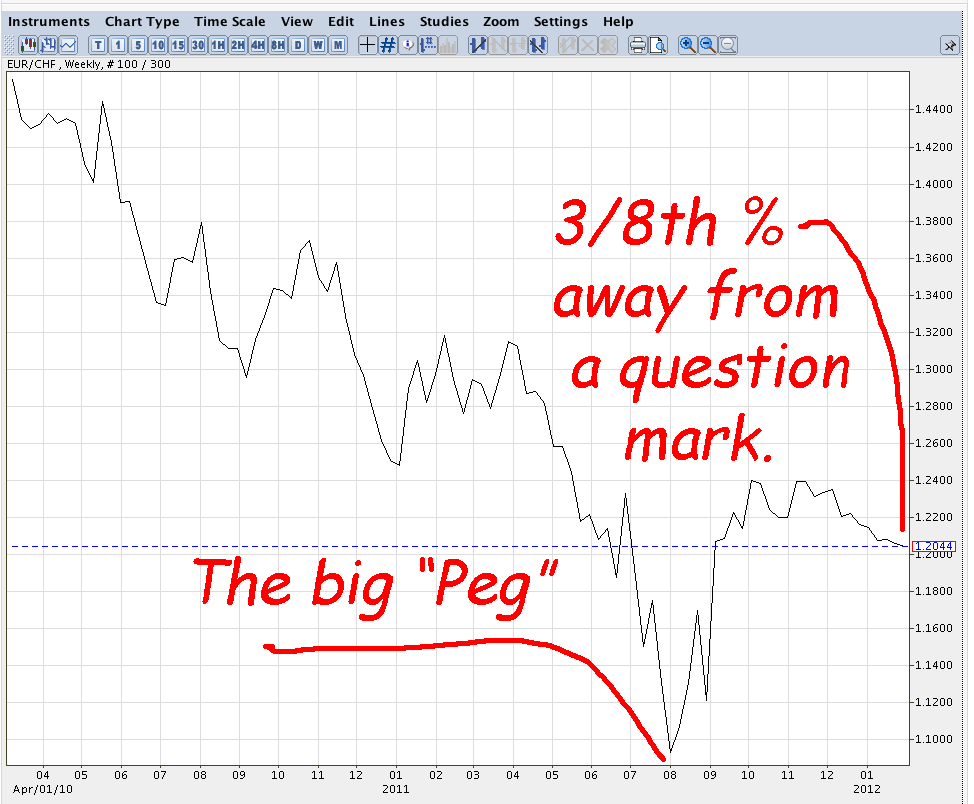

We are near the edge on a few situations in the FX markets. I'm watching the EURCHF and the USDYEN. The market traded EURCHF to a low of 1.2032 today. It closed at a (slightly) safer 1.2044. I would not be surprised to see this cross trade very close to the official peg of 1.20 in the not too distant future.

There is no doubt in my mind that the Swiss National Bank (SNB) will be involved when and if the EURCHF hits the 1.2000 mark. My guess is that 99% of everyone else who “votes” in this market believes the same. This begs a question.

“If everyone knows the cross can’t go below 1.20, then why in hell is it sitting 44 lousy pips away from the peg?”

The EURCHF is a very good funding currency for a carry trade. Yields on French and Italian bonds make it attractive, given that Swiss money can be had through the swaps with a negative Vig. It seems like the market wants to trade the EURCHF very close to the peg for the time being. That’s odd, given that it’s a “100% sure thing” that the SNB will protect the downside.

The Dollar is a sideshow for the Swissie. I doubt many are trading USDCHF these days. It’s worth noting that the Dollar got beat up for five big figures against the Euro the past week or so. Normally when you see Euro strength versus the dollar, you also see it in the EURCHF cross. Not this time around. It does make me go Hmmmm.

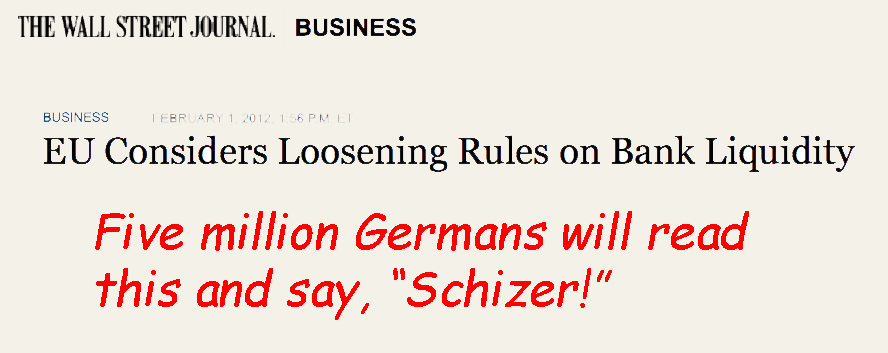

I think there are scenarios where the EURCHF could trade to the peg. If, by surprise… the Greek deal fell apart, money would move into the Franc. It could be something subtler. A reminder of just how fragile the Euro system is these days might do it. For example, this headline from the WSJ that came out after the NY close may scare the crap out of many people with bank accounts in the EU.

If the EURCHF does test the peg, it will probably happen during European trading hours. I expect the SNB’s new boss, Thomas Jordan, will stand up and bid 1.1999 for all the Euros the market has on offer.

A side story to this is what happens if the cross breaks the peg outside of Euro trading hours. What if some hedge-fund types lean on it at 3 PM on a Friday in NYC? The same question arises during Asian hours. If Monday morning, in Australia, the cross is offered at 1.1997, without a bid, it will create a big splash. That "100% sure thing" will immediately come into question. Mr. Jordan doesn’t want that.

There are only two possibilities for intervention outside of the Euro time zone:

1) The SNB can rely on the Central Banks of Australia, Japan and the USA. Those CB’s would act on behalf of the SNB during their respective market hours.

But, realistically, there is no chance in hell for this. The US Fed can’t play in this sandbox. For the Fed to participate in an effort to weaken the Franc would make it (and Tim Geithner) look silly. The USA has been threatening China with all manner of sanctions over China’s policy of maintaining an artificially weak currency. The Fed simply can’t help Switzerland do the same thing.

2) The SNB will give “resting” orders to commercial banks. The most likely name for this would be UBS. It would not surprise me if one of the other big banks had a turn at doing the SNB’s calling. JPM and Bank of Tokyo are likely candidates, Barclays may get put on the list if persistent intervention was required. The resting order might be:

To: Bank of Tokyo, Tokyo – FX Department

Firm order, good till cancelled. SNB offers to purchase up to Euro 200 million versus CHF at 1.1999. Call Hans -immediately- if the first E50mm is executed.

With this, we get the EURCHF trading “one-around-two” (one pip around 1.200 or, 1.1999 – 1.2001).

A few thoughts about resting orders from CBs.

*The information always leaks.

*The bank operating for the SNB will be named.

*A bank that has a large resting order from a CB has a huge tactical advantage against other market players. (I know, I played this game.)

*A move into the intervention zone will rile other markets, most notably in the Euro funding markets.

A Yen for a Yen Trade

The USDYEN is dangerously close to becoming an issue (again). The NYC low was 76.08. Anything under 76.00 might bring in the Bank of Japan (BOJ). The last time we were here was on 10/27. The chart:

Japan desperately needs a stimulus. It has gone to the cupboard for more ZIRP and deficit spending too many times. At 220% debt-to-GDP, its credit card is maxed out. My reading of the Japanese press is that more debt as a stimulus is not a viable alternative. (They are talking about doubling the VAT to 10%, to cover a portion of the deficits. Given that painful effort, they are not going to turn around and borrow more.)

The only option left is to fiddle with the FX rate. It would make a very big difference if the USDYEN was 85. The Japanese Finance Ministry folks must be looking at the SNB's actions with envy. A 15% devaluation off the low, coupled with a future exchange rate that was (somehow) pegged to the USD, or a basket of currencies, would be just the ticket.

Here again, I don’t think this will happen. The boys at the BOJ know that they would have to absorb a trillion in additional reserves if they drew a line in the sand with a currency peg. That doesn’t mean that they are not thinking about it. Some “Peg Talk” by some MITI types might get the ball rolling.

I think we'll see a break of 76.00 soon. The sparks will fly somewhere around 75.60. Given the deteriorating conditions in Japan since the October intervention, I do wonder if the BOJ might be somewhat more aggressive this time around.