{kind=link}

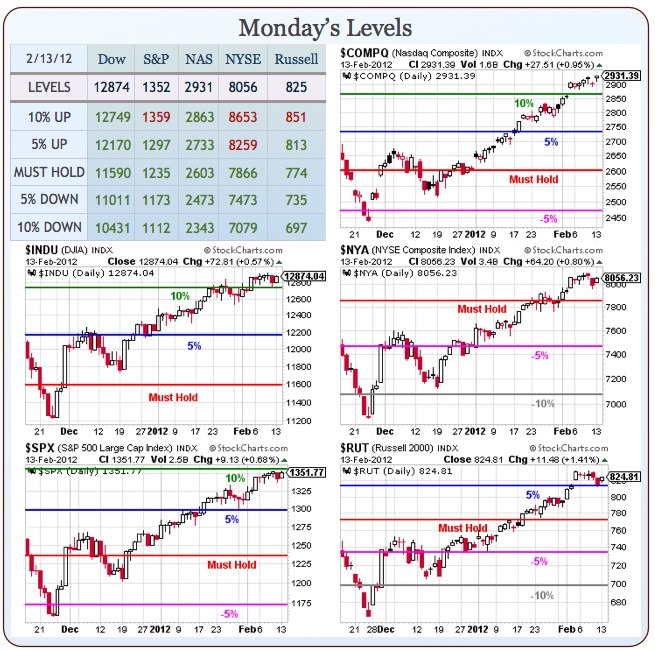

We are right on our 10% lines for the Dow, S&P and Nasdaq.

We are right on our 10% lines for the Dow, S&P and Nasdaq.

The S&P rests just 6 points under our final line of resistance on the Big Chart and the Dow and Nasdaq have been over the line since the beginning of the month. Now it's up to the S&P to put up or shut up as we test 1,359, which is exactly were we expected to top out on this rally – only we expected it months from now.

We went over the Dow components previously and determined they were a bit stretched at 12,749 and the Nasdaq would be under the mark if not for AAPL – and a sell-off there along with an overall pullback in the Nasdaq can lead to an extremely rapid decline in the index. Obviously it seems like my timing is off with AAPL just hitting $505 yesterday but, on a run from $420 pre-earnings, that's 20% and certainly due for a $16 pullback to test $485-490 in the very least.

That's 3% and AAPL is 10% of the Nasdaq so 0.3% of a drag coming there is very likely and I have long been pointing out to Members that the Tech sector – minus AAPL and AAPL partners – is not having a very good year. That's why the rally does not make sense – AAPL is strong but many, many other techs are weak yet they have all been moving in lock-step higher and higher and higher – up 450 Nasdaq points (18%) since Thanksgiving – despite 70 out of 100 of the components having lower revenues and lower earnings than they did a year ago.

That's 3% and AAPL is 10% of the Nasdaq so 0.3% of a drag coming there is very likely and I have long been pointing out to Members that the Tech sector – minus AAPL and AAPL partners – is not having a very good year. That's why the rally does not make sense – AAPL is strong but many, many other techs are weak yet they have all been moving in lock-step higher and higher and higher – up 450 Nasdaq points (18%) since Thanksgiving – despite 70 out of 100 of the components having lower revenues and lower earnings than they did a year ago.

GOOG and AMZN both missed, with AMZN earning less than half of what it earned in Q4 of 2010. Financials are down 21% from last year's Q4 reports – what is everyone so excited about? That sector is the largest in the S&P! Overall, earnings in the S&P are up 2.7% from Q4 2010 – a drastic slowing of growth from the 33% gains we had over Q4 2009. Taking out the drag of the Financials but leaving in AAPL, S&P earnings growth is 8% over last year.

As you can see from David Fry's SPY chart above – we're already 10% higher than we were last February and last February we certainly thought (forward-pricing mechanism) that the S&P would grow earnings more than 4% in 2011. In fact, realization that growth was slowing in July along with the Japan disaster of March and the ongoing Greek crisis led to a 20% pullback over the summer – from 1,350 to 1,100 on the S&P.

As you can see from David Fry's SPY chart above – we're already 10% higher than we were last February and last February we certainly thought (forward-pricing mechanism) that the S&P would grow earnings more than 4% in 2011. In fact, realization that growth was slowing in July along with the Japan disaster of March and the ongoing Greek crisis led to a 20% pullback over the summer – from 1,350 to 1,100 on the S&P.

This nifty chart of our "One Trade for 2012," BAC, shows that there are certainly bargains to be had. BAC, in fact, is responsible for 20% of the S&P's earnings gains this year – yet it still gets relatively no respect as it's still 40% LOWER than it was last February. What kind of rally is this if BAC can't get any traction on $1.6Bn in Net Income from a loss of $1.5Bn last year?

If course the stock has already gone nuts since our Jan 5th pick – hopefully we'll get a little pullback here, back to $7 and then we can reload as there's nothing wrong with BAC – or hundreds of other individual stocks in the S&P or the Nasdaq but ramming thousands of stocks in those indexes all up in synch like this is just ridiculous. Just this morning, we were playing with the oil pumpers and getting a few nice runs to short oil at $101.50 (after our first failed attempt to short them below $101.20, which almost cost us our Egg McMuffin money!).

There is simply too much effort being put towards convincing us that there is a rally with gaps up before the market opens and stick saves into the close to get back to the gap up open after the rest of the day is spent transferring shares from the institutions – who pump up the prices when the lights are out – to retail traders – who buy on the morning dips thinking they are catching a trend that will last.

There is simply too much effort being put towards convincing us that there is a rally with gaps up before the market opens and stick saves into the close to get back to the gap up open after the rest of the day is spent transferring shares from the institutions – who pump up the prices when the lights are out – to retail traders – who buy on the morning dips thinking they are catching a trend that will last.

The epic weakness of the Dollar is a huge concern but not so much that we're willing to take our precious Dollars off the sidelines and throw them into the markets at these valuations. Sure we like to trade – we trade every day – but it's been almost a month since we've found many long-term positions we're willing to get attached to. That's been a month in which the McClellan Summation Index (which tracks longer-term trends than the Oscillator) has run back up to overbought levels we have not seen since the Summer of 2009, when the market had already moved up 50% from it's lows.

That did not, of course, prevent us from moving higher. We went from 666 in March to 1,000 in August of 2009 on the S&P (50%) as the summation index finally hit that overbought line – THEN we went from 1,000 in August of 2009 to 1,150 in January of 2010 before falling back to 1,050 and then back to our story of last Summer we discussed above. What is key though is that, once we hit the seriously overbought levels we're at now – that was pretty much it for the market gain for quite a while.

So shorting has a much higher probability of success than going long at the moment. It's much easier for the markets – even assuming the move up was not a prop job put up by the Fund Managers to herd the retail sheep in for the slaughter – to go down than up at the best of times but trying to move a $40Tn US market up ANOTHER $10Tn after we just moved it up $10Tn on almost no volume without MASSIVE inflows of capital begins to strain the bounds of Financial Physics (see "Stock Market Physics," which I used to warn people the markets were overbought (too early) at the end of 2006).

So shorting has a much higher probability of success than going long at the moment. It's much easier for the markets – even assuming the move up was not a prop job put up by the Fund Managers to herd the retail sheep in for the slaughter – to go down than up at the best of times but trying to move a $40Tn US market up ANOTHER $10Tn after we just moved it up $10Tn on almost no volume without MASSIVE inflows of capital begins to strain the bounds of Financial Physics (see "Stock Market Physics," which I used to warn people the markets were overbought (too early) at the end of 2006).

The science doesn't change. The Nasdaq is 20% higher now than it was then and, on our 5% rule, it's due for a 4% pullback to 2,725. That just so happens to be about what we're expecting from AAPL on a test of $500 but I learned my lesson in 2006 and, IF the S&P can pop 1,359 – I will happily bite my lip and BUYBUYBUY until this thing (whatever it is) finally exhausts itself. For the moment, however, I remain skeptical.