{kind=link}

Courtesy of Mish

Courtesy of Mish

ZeroHedge posted an interesting article called Europe Is Now China's Sweatshop As Great Wall Starts Building Cars In Bulgaria. Unfortunately the article contains many often repeated trade fallacies as well as numerous other errors.

Mish: China's wages are rising fast. Sometimes in leaps of 20%. From where? How sustainable is it? Please consider this snip from the Reuters article HP, Dell watch rising China labor costs for Applewritten February 27, 2012:

"Taiwan-based Foxconn said the pay of a junior level worker in Shenzhen, southern China, had risen to 1,800 yuan ($290) per month and could be further raised above 2,200 yuan if the worker passed a technical examination. It said that pay three years ago was 900 yuan a month."

Let's do the math. $290 a month is $3,480 a year. Assume 20% annual wage hikes, once a year for 5 years. Should that happen, at the end of that time, the salary would be 8,659.35. US minimum wage is $7.25 an hour (not sure what it will be five years from now), but that is about $14,500 assuming a 40 hour work-week and 2 weeks unpaid vacation.

It would take 33% raises every year for five years just to match US wages. Is that likely?

Bear in mind that shipping costs and productivity issues are also in play. This is not simply a wage issue.

ZH: As Spiegel reports, carmaker "Great Wall this week became the first Chinese automobile manufacturer to open an automobile assembly plant inside the European Union in the latest move suggesting the country's carmakers are seeking to establish a beachhead into the European market." Yes, that's right: it is now cheaper for China to make cars in the European Union: "It used to be that European carmakers opened plants to assemble their cars in China. Now the Chinese have turned the tables with the opening of their first factory in Bulgaria, an EU country with low labor costs and taxes.

Mish: Is it really cheaper to build cars in Bulgaria, or is something fundamentally different happening? I suggest the latter, possibly both, but the latter point is critical. China is sitting on huge piles of forex resereves. Those reserves must return at some point. China can either buy goods from Europe, or it can invest in Europe. What better place to invest than in a country with low taxes and low labor costs? The Bulgarian Lev currency is pegged to the euro at €1 = BGN 1.95583. Bulgaria is expected to join the Eurozone by 2015. Whether joining makes sense is debatable, but China sees an opportunity. China also has a need to put euro reserves to work. That need is a mathematical identity. By the way, this is likely a good deal for Bulgaria. It gets badly needed jobs.

ZH: Chinese carmakers are setting their sights on the European and American automobile markets." The ramifications of this landmark development are massive for virtually every aspect of the economy: for domestic labor migration, for inflation, for the trade balance, and certainly for US workers.

Mish: Agreed but for different reasons. This is a necessary part of global rebalancing.

ZH: Bulgaria, the EU's poorest country, is attractive as a labor market because it is an oasis of cheap wages and low taxes. Workers are considered well educated and the country is ideal as the site for a company like Great Wall to launch. Given that wages for factory workers have risen considerably in China in recent years, assembly sites abroad have become increasingly attractive for some manufacturers.

Mish: Exactly. So just how likely are those 33% annual raises for Chinese workers if the trend catches on? How likely are those 33% annual raises regardless?

ZH: So the real question is if Chinese wages can no longer compete with those in a poor EU member, just how high are they?

Mish: $290 a month for junior level workers and I will take a stab at not much higher for senior level workers.

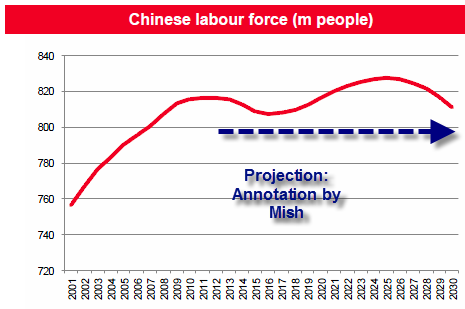

ZH: And how long before China, for so many years a happy mercantilist importer of Bernanke's monetary inflation courtesy of its currency peg, is no longer competitive with ever growing parts of the EU, and then America? Does this mean that China's cheap labor force has pleateaued and the labor migration of peasants moving from the periphery to the cities no longer provides cheap labor? This was the topic of an extended analysis by SocGen from early January (posted here), of which the salient chart is presented below.

Mish: Is that alleged shortage of labor due to inflation and monetary stimulus in China or the US? How much Chinese labor goes into totally unaffordable projects driving up the price of labor? How much of the worker stagnation is simply do to falling export demand? I do not have the answers to those questions but there are multiple explanations for the alleged "shortage of labor". The single most likely explanation however, is unsustainable stimulus and growth, in China.

ZH: Aside from demographics, the macroeconomic implications on foreign trade and capital flows are monumental: most immediately for the US, it puts today's Wal Mart miss in a very different perspective, as it means that China is no longer the source of cheap commoditized produce, which in turn means that the entire discount retail vertical may have entered the secular sunsetting phase.

Mish: For a completely different viewpoint, and a deflationary one at that, please consider Hugh Hendry of Eclectica Discusses Hyperdeflation, Europe, China, and Japan.

ZH: Most importantly, it means that going forward China will have zero tolerance for Fed monetary expansion as any hot money will immediately set off an inflationary forest fire as China suddenly finds itself with absolutely no output gap slack (unlike America which allegedly has more than enough, even though it is really just a secular regression to the mean shift).

Mish: Most importantly, such events are a necessary part of global rebalancing. As a mathematical identity, China's hoard of euros must eventually return to Europe just as China's hoard of dollars must eventually return to the US. The sooner this happens the better. The US and Europe should both embrace Chinese investment. Unfortunately, that is highly unlikely.

Mike "Mish" Shedlock

http://globaleconomicanalysis.blogspot.com