{kind=link}

When will I see you again?

When will our hearts beat together?

Are we in love or just friends?

Is this my beginning or is this the end? – The Three Degrees

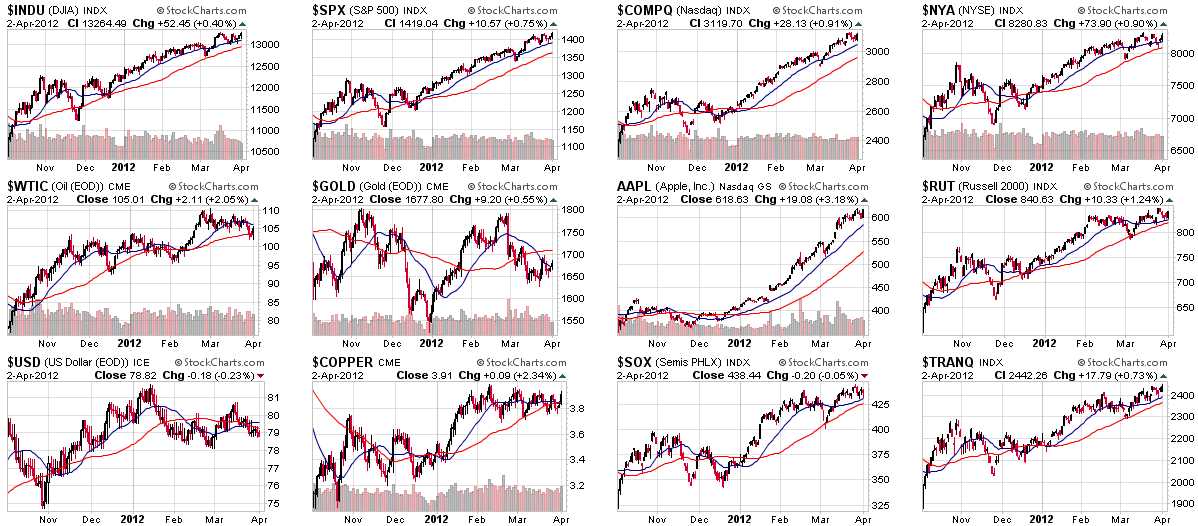

Will the S&P see 1,420, will the Russell see 860 again?

We need to see 13,600 on the Dow to flip our bull switch and we're happy to play that index bullish with something like the DDM (now $71.03 with the Dow at 13,264) $68/70 bull call spread at $1.15, which pays $2 (up 74%) if the Dow simply doesn't fail 13,200.

The potential loss of $1.15 on the trade can be offset with the sale of the May $127 puts at $1.10, which is a bet the Dow holds 12,700 (down 4.25%) or you can pick a stock you would REALLY like to own if it gets cheaper like AAPL, and sell the May $460 puts (down 25%) for $1 or a stock I would love to buy cheap(er) like BTU May $28 puts (down 5%) for $1.25 or CHK July $21 puts (down 14%) for .90. Assuming you offset $1 of the $1.15, then you are in for net .15 on the $2 spread with the potential for a 1,333% return on cash if the Dow simply doesn't go down from here. If you are not willing to make that bet, then you are simply not bullish.

We still favor cash in this very uncertain market but we've been more enthusiastic about adding bearish trade ideas, on the whole. Our very bearish, very aggressive, short-term $25,000 Portfolio gained a virtual $20,000 in the past two weeks DESPITE the fact that we're re-testing the tippy top of the market.

We still favor cash in this very uncertain market but we've been more enthusiastic about adding bearish trade ideas, on the whole. Our very bearish, very aggressive, short-term $25,000 Portfolio gained a virtual $20,000 in the past two weeks DESPITE the fact that we're re-testing the tippy top of the market.

That's because we are essentially doing the opposite of "buying the dips", which is "selling the rips" – taking advantage of the excitement of the bulls, who are whipped into an almost daily frenzy by these low-volume rallies.

I'm happy to be bullish, really I am, but SHOW ME THE EARINGS! We are now up 10% since January earnings and 25% since October's report so I am looking forward to some SPECTACULAR numbers to back up these new and vastly improved valuations for all these companies. Heck PCLN (on our Long Put List and now in our $25KP) is up $250 (55%) since January alone so I have to believe that the intense disappointment of last Quarters' $225M ($5.05 per share) will be left in the dust and we'll finally see how well they justify their $720 price point with the $36Bn market cap that we showed last week is GREATER than all of the Airlines COMBINED.

Would you rather own all 15 airlines in the Transport Index or PCLN? Apparently, Mr. Market would rather own one of the many web-sites that book the trips than the entire fleet of hard assets. Sure running an airline is a tough business, especially with sky-high oil costs but that doesn't bother the market either so why let it bother you? Richard Branson certainly seems to have made a few bucks running an airline (almost as much as Shatner has pitching one) – it can't be that awful, can it?

Would you rather own all 15 airlines in the Transport Index or PCLN? Apparently, Mr. Market would rather own one of the many web-sites that book the trips than the entire fleet of hard assets. Sure running an airline is a tough business, especially with sky-high oil costs but that doesn't bother the market either so why let it bother you? Richard Branson certainly seems to have made a few bucks running an airline (almost as much as Shatner has pitching one) – it can't be that awful, can it?

CMG raised the price of a burrito from $8 to $8.50, up 6.25% in the Fed's zero-inflation World (we get the minutes of the last Fed meeting at 2pm today). That popped their stock over $400 this month and they are now up 23.5% since last earnings and up 40% since October, when they earned $1.85 per share. Sure they only earned $1.83 a share in Q4, which is, I believe, LESS than $1.85 but if you string together even 4 $1.83s together you get $7.32 and you only have to multiply that by 57.37 to get to $420 – which makes perfect sense for a restaurant stock, doesn't it?

Well, maybe not. That's why CMG is also on our Long Put List with earnings coming up on the 19th. Nothing makes the pumper cockroaches scurry away faster than shining the light of earnings on them and we're looking forward to a VERY exciting earnings season this year as expectations are, literally, through the roof.

It's a good thing Branson is wearing his space suite because these charts are going to the moon baby! That 5% drop in the Dollar has been rocket fuel for the indexes, as well as commodities – even gold didn't fall as much as it should have on the persistent Dollar weakness despite the fact that it's massively over-priced for a "healthy" economy. Oil has also gotten a $5 lift from the falling Dollar as well as the constant pounding of the Iranian war drums by each of the GOP candidates and, of course, half the guests on CNBC.

Just this morning, PBOC's Governor Zhou Xiaochuan sad the Fed needs to recognize the dollar's reserve status and give some consideration to the global economy. "It's very difficult to control the flow of liquidity … inevitably, some emerging economies will suffer too much capital flow."

Just this morning, PBOC's Governor Zhou Xiaochuan sad the Fed needs to recognize the dollar's reserve status and give some consideration to the global economy. "It's very difficult to control the flow of liquidity … inevitably, some emerging economies will suffer too much capital flow."

The Governor warned that the global economy hasn't yet escaped the financial crisis, while cautioning the U.S. to take "more responsibility" for its monetary easing. There are "new elements that could bring the global economy back into recession," the central bank chief said in a panel discussion Tuesday at the Boao Forum in the southern island province of Hainan, without elaborating on what the elements are.

While the market bulls tend to worship China for its infinite potential to expand revenues, they completely ignore anything the Chinese say and do that is not a bullish statement. This China Blindness is going to be the undoing of many investor if it turns out that Chinese officials are not lying to us and their economy is slowing but, for now, the US Bulls believe they know better than the people who are actually in China.

Meanwhile, Gene Munster has put a pencil to my theory that AAPL's gains are everyone else's pains and calculates that 1/2 of AAPL's next $400Bn in potential market cap (on the way to AAPL $1,000) would have to come from the hides of their competitors. That's behind our (so far awful) theory on shorting the Qs – that AAPL has had a good run to $600 and should pause there over earnings while we get nothing but damage reports from their competition and that, finally, should be enough to give us a pullback in the Nasdaq.

Meanwhile, Gene Munster has put a pencil to my theory that AAPL's gains are everyone else's pains and calculates that 1/2 of AAPL's next $400Bn in potential market cap (on the way to AAPL $1,000) would have to come from the hides of their competitors. That's behind our (so far awful) theory on shorting the Qs – that AAPL has had a good run to $600 and should pause there over earnings while we get nothing but damage reports from their competition and that, finally, should be enough to give us a pullback in the Nasdaq.

It's very easy to cover a short Nasdaq position – just go long on AAPL. One trade idea we like is selling the AAPL 2014 $400 puts for $28.50 and using that cash to buy the Jan $600/665 bull call spread at $29 so you are in the $65 spread for .50 in cash and you are obligated to buy AAPL for $400 if it is below that price in Jan 2014. Obviously, if you don't REALLY want to buy AAPL for $400 (35% off) then this is a foolish play but, if you do – then this trade can make $64.50 in profits if AAPL just gets to $665 by the year's end – that's up 12,900% on cash! The best thing about this trade is it starts out $18 in the money so you're potentially up net $17.50 (3,500%) on day one – assuming AAPL just flatlines into Jan expirations.

So a trade like that goes a long way towards paying for some QQQ May $67 puts at $1.08 and, if those drop to .60, then we roll to the July $67 puts (now $2.15) for maybe another $1 or less – as you can see, it will be a long time before we even come close to eating into our AAPL money and it's VERY UNLIKELY that AAPL is heading down without our QQQ shorts paying off.

That's hedging. That's how we can be long-term long and short-term short while remaining "cashy and cautious" leaves us with plenty of cash on the side to buy stocks that do finally go on sale – like AAPL for $400!