Courtesy of Mish.

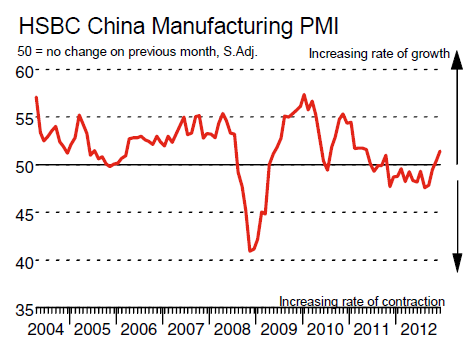

The HSBC China Manufacturing PMI™ shows modest growth this month. The index is at 51.5 with growth above 50.

After adjusting for seasonal factors, the HSBC Purchasing Managers’ Index™ (PMI™) – a composite indicator designed to give a single-figure snapshot of operating conditions in the manufacturing economy – posted 51.5 in December, up from 50.5 in November, signalling a modest improvement of operating conditions in the Chinese manufacturing sector. Moreover, it was the highest index reading since May 2011.

Input prices at manufacturing plants continued to increase in December, and for the third successive month. The rate of inflation eased slightly from November but remained marked overall. Average tariffs also increased during December, after remaining broadly similar in November. Output charges rose at an accelerated pace that, although modest, was the quickest in 14 months. Anecdotal evidence suggested that tariffs were raised in line with rising market demand and higher input costs.

Purchasing activity rose at a marked rate in December, the fastest since March 2011. Exactly 17% of panellists reported increased input buying. Consequently, stocks of purchases also rose. Even though the pace of stock accumulation was only slight, it was the quickest in two years. Rises in input buying and stocks of purchases were generally associated with higher new order volumes.

Comment

Commenting on the China Manufacturing PMI™ survey, Hongbin Qu, Chief Economist, China & Co-Head of Asian Economic Research at HSBC said:

“December’s final manufacturing PMI picked up for the fourth consecutive month to a 19-month high, thanks to the faster new business flows and the end of destocking. Such a momentum is likely to be sustained in the coming months when infrastructure construction runs into full speed and property market conditions stabilise. This, plus Beijing’s reiteration of keeping pro-growth policy in place into the coming year, should support a modest growth recovery of around 8.6% y-o-y in 2013, despite the ongoing external headwinds.”

{kind=link}

Pollyanna Outlook

I beg to differ with Hongbin Qu.

There is no reason to believe property market conditions will stabilize. Nor is there any reason to believe infrastructure construction will run at “full speed” for any significant length of time.

Indeed, should either of those happen, China’s already massive rebalancing problem will just get worse.

Realistic Outlook…