{kind=link}

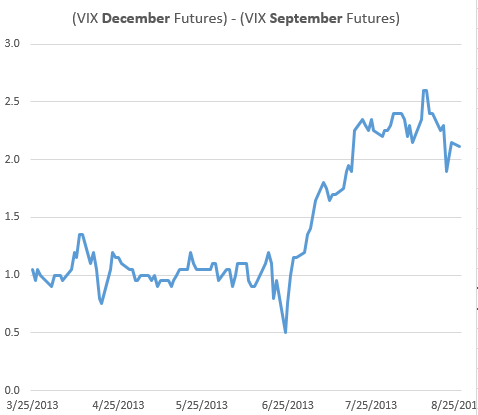

A steeper VIX futures curve

Courtesy of SoberLook

One helpful risk indicator worth tracking is the steepness of the VIX futures curve (see description). In particular the spread between the December and the September futures provides a measure of risk premium that should in theory encompass both the Fed action and the budget/debt ceiling fight in Washington. Based on the recent spread movements, the market seems to be mostly just concerned with the Fed right now. Will the curve steepen further once the risk of this potential government shutdown becomes more real?