{kind=link}

Courtesy of John Rubino.

Let’s say you’ve got some traditional mutual funds full of stocks and bonds and they’re way up. You’re worried by all the taper talk and the charts that show share prices and margin debt back up to pre-crash levels, and you’re wondering whether it’s time to redirect some of that capital to someplace that no one is calling a bubble.

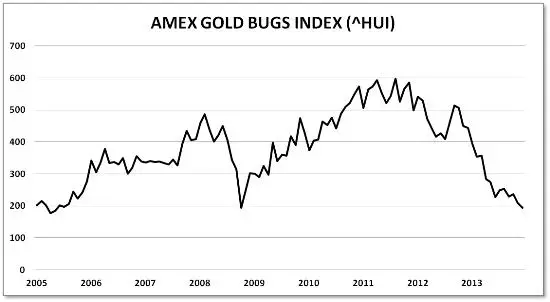

Meanwhile, you’ve noticed that precious metals mining stocks are in another of their periodic corrections, with this one looking a lot like 2008’s bloodbath — which was followed by an epic bull market:

But with gold and silver below the production cost of a lot of miners, there’s a ton of risk to go with the seemingly huge upside. So committing to individual miners is terrifying. Still, that’s how it always looks at the bottom.

So if you’re going to buy one, which would it be?

Let’s start with the premise that at a bear market bottom investors, having been faked out so many times on the way down, don’t trust the turn. So to the extent that they buy anything, they buy the safest names. If the miners keep to this pattern, next year will be good for the best and mediocre for the rest. And in mining the safest bets are the royalty and streaming companies that don’t actually mine metal themselves but contract with other mines to take part of their future output. They do this in a variety of ways ranging from buying up existing royalty agreements that call for a given number of ounces delivered over a specified period of time, to in effect making equity investments in mines in return for some portion of future production. The first is passive investing, the second more like venture capital.

The biggest companies in this space have been able to gain interests in lots of mines on generally favorable terms. Here are the three to consider:

Not Risk-Free

A lot of these companies’ investments depend on mines expanding or continuing to produce as expected. Should the price of gold and silver fall much from here there will be wholesale project cancellations and mine shutdowns, which would mean less cash flow from their positions. This is a very real risk, but even so, the impact on the royalty/streaming companies would be less than on the typical miner because the former have spread their bets among so many different mines.

The other issue is the availability of good investments going forward. The royalty companies have to invest their cash at rates that exceed their cost of capital. Such deals are scarce in this environment and will get scarcer if metals prices don’t recover. Here again, though, we’re talking about diminishing cash flow, not an existential threat.

Meanwhile, in a really bad market these companies become the king makers in the industry, deciding which juniors live or die and using that power to cut deals that become hugely favorable when prices revive and those new mines are developed.

To sum up, these companies are not as safe as owning bullion intelligently stored, but they’re safer than the typical miner, with considerable upside margin over metals prices if things turn around from here.

Visit John’s Dollar Collapse blog here >