{kind=link}

Courtesy of Charles Hugh-Smith of OfTwoMinds

"Prosperity" based on serial asset bubbles and near-zero interest rates is neither real nor sustainable.

Longtime readers know I have been covering residential housing since mid-2005. In those 8+ years, housing has proceeded through a cycle of bubble-bust-echo-bubble: now the echo bubble is crumbling, for all the same reasons the 2006-7 bubble burst: a prosperity based on asset bubbles and low interest rates is a phantom prosperity that cannot last.

Correspondent Mark G. has written a three-part series on the current state of the residential and commercial real estate (CRE) markets. Part 1 addresses residential real estate.

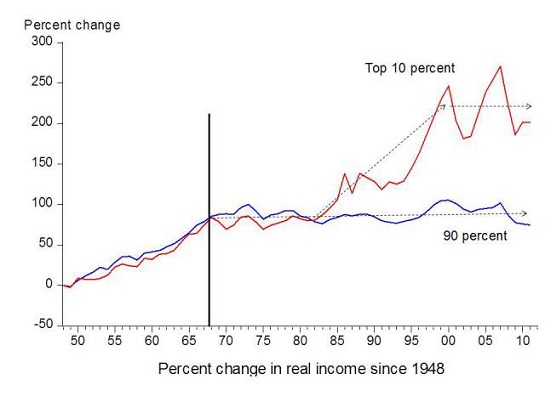

The broad context of this analysis is straightforward: an economy based on ever-rising consumption falters when real household incomes stagnate or decline. Real income for the bottom 90% has been stagnant for forty years, and has declined since 1999.

The only way to keep consumption rising when incomes are stagnant is to boost the borrowing power (i.e. collateral and creditworthiness) of households by inflating asset bubbles that create temporary (i.e. phantom) collateral and by lowering interest rates so the stagnant income can support more debt.

This is why the Federal Reserve and the other agencies of the Central State have been reduced to blowing serial assets bubbles: there is no other way to keep a consumption-based economy from imploding.

But "prosperity" based on serial asset bubbles and near-zero interest rates is neither real nor sustainable: real prosperity is based on rising real incomes, not debt leveraged on phantom collateral.

Here is Part 1 of Mark's series on U.S. real estate.

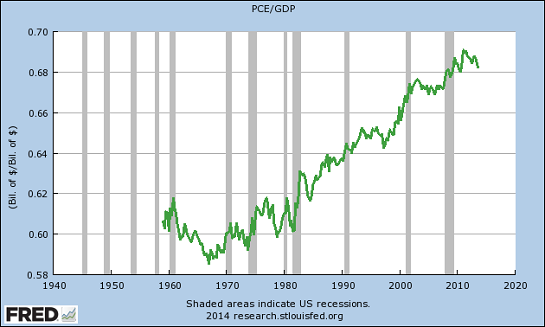

PCE = Personal Consumption Expenditures. GDP = Gross Domestic Product. The ratio of these numbers times 100 produces the percentage figure.

PCE includes food, entertainment, residential housing, automobiles, clothes and iPads. The consumer broadly has two ways to obtain the money needed to support this spending. The first method is to earn it and the second method is to borrow it.

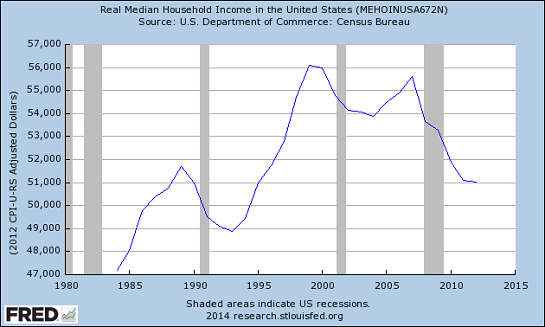

Since 1999 average real household income in the USA has declined by 10%. This real decline was only temporarily reversed during the peak bubble years. From 2000 to 2008 the full effects of this decline were masked by a vast expansion of household debts of all kinds, a collapse in mortgage and consumer lending standards and a concurrent decline in household net worth.

Exactly which 90% of the population is bearing the brunt of this collapse, and why it is occurring, is beyond the scope of this overview.

This trend culminated in the financial crisis of 2007 – 2009. This began in the subprime mortgage sector, spread to the entire residential real estate market and progressively engulfed commercial real estate, banking, the stock markets, commodity markets and finally all of international trade.

In response the Federal Reserve multiplied its balance sheet five times from $800 billion to $4 trillion dollars. And the US Government concurrently ran peak fiscal deficits up to $1.8 trillion. The US Government also extended many trillions more in direct guarantees of minimum prices of financial assets of all kinds.

US Residential Real Estate

The observed result of all this monetary and fiscal stimulus, combined with the lowest mortgage interest rates in the post World War II era, was to only slow the rate of decline of median US household income. In the combined residential US real estate market this set of policies had the following results:

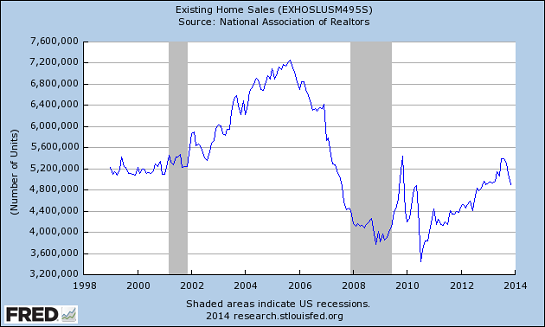

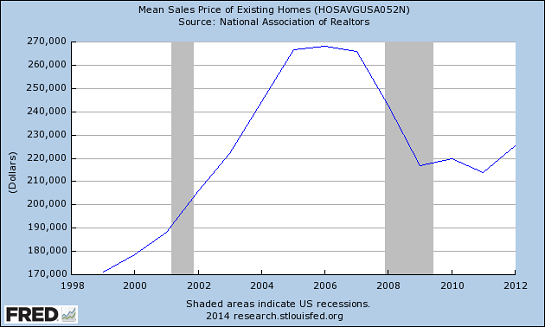

Existing Home Sales

The rate of existing home sales has yet to recover to the levels of the mid-1990s. Since the most recent decline in sales rate is paralleling the upward spike in mortgage rates it is reasonable to believe they probably will not recover.

The average sales price of existing homes has recovered to approximately 2003 levels.

(Note: Whether increasing average home prices for a population still experiencing declining real average household incomes is an intelligent public policy goal is a second question. This question deserves far more critical discussion than it currently receives.)

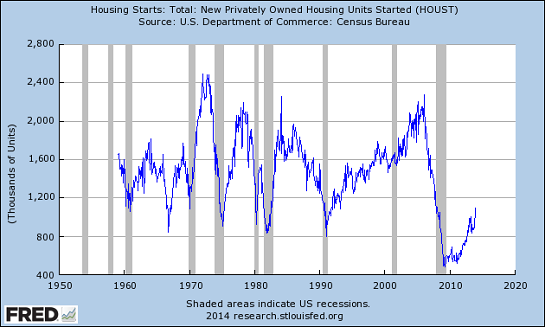

New Home Sales: (This time it really is different)

Those interested in detailed numbers for single and multifamily housing construction can find them here:

New Privately Owned Housing Units Authorized by Building Permits in Permit-Issuing Places(Census Bureau)

New-Home Production Tops 1 Million in November (NAHB)

The National Association of Homebuilders (NAHB) announced in mid-December 2013 that new starts in single and multi-family housing had finally exceeded an annualized rate of 1 million units. In other words, the actual 2013 new construction number will be approximately 935k.

Prior to 2008 these sub 1 million total new build numbers were only seen in the six years of 1991,1981, 1980, 1975, 1966 and 1960. They have subsequently occurred six straight years in a row from 2008-2013. It will not be known for another year whether new builds will finally exceed 1 million in 2014.

Note that US population has been continuously increasing over the entire time period. Therefore the present era represents the lowest per capita rate of new construction on record for six decades.

Near Term Prospects

There are two primary reasons that residential real estate has not recovered more that it has. These are very straightforward:

1. Real US household incomes continue to decline.

2. Residential mortgage lending standards have been significantly tightened since 2007.

These charts represent averages and sums across most of a continent. Within this expanse some areas are already experiencing new record bubbles while many others continue to fall deeper into local depressions.

There are several other factors that have affected and will continue to affect the residential real estate recovery.

Factor One: Habitable Vacant Dwellings

AMERICA’S 14.2 MILLION VACANT HOMES: A NATIONAL CRISIS (RealtyTrac)

“As of the first quarter of 2013, there are just over 133 million housing units in America and 10.7 percent of them — more than 14. 2 million — are vacant all year round for some reason or another, according to the Census Bureau."

To this 14.2 million empty dwellings we can add several million additional vacation homes that are only occupied for a few months a year.

Factor Two: Cultural Shift To Multigenerational Households

At least one person is required to create a household and occupy a dwelling. A related question is, what is the average number of empty bedrooms per occupied dwelling in the US? It is at least 1.0 and very probably much higher.

During recent years there has been an increase in average household size and a corresponding drop in the total number of households. This is the result of adult children and grandchildren moving back in with the “folks” to weather the economic storm. Whenever this occurs, two households become one household and residential housing demand is sensibly reduced.

A related trend is adult children who are economically unable to ever leave their parents household. To the extent these shifts are permanent trends rather than temporary expedients this will permanently reduce the per capita demand for residential housing.

Based on results the decline in real household incomes has proven insensitive to a variety of economic theories and policies. Neither the Republican-Bush era tax rate cuts nor the Democratic-Obama Keynesian pump priming at fire hydrant pressures has succeeded in reversing this long term trend. Nor has anything appeared recently to suggest an abrupt reversal is at hand in this key trend of average household income.

In these circumstances the only other possibility for further residential real estate “recovery” would be for government regulators to foster another bubble by effectively relaxing residential mortgage lending standards again.

Three Possible Future Outcomes For U.S. Residential Real Estate

In order, these are: go up further, stay the same or resume declining.

1. Up. The Federal Reserve has already begun withdrawing from its bond buying program, albeit at a slow rate of ‘taper’. This has accordingly led to mortgage rate increases which were accompanied by a prompt decline in existing home sales. It is mathematically impossible for a population with declining real household incomes to propel residential real estate markets higher in the face of higher interest costs.

2. Steady State. At a minimum, this outcome requires that average household income cease declining and that mortgage rates not rise significantly. Neither of these outcomes is likely. The following review of commercial real estate will examine clearly visible economic trends that make further household income declines a certainty.

If we cannot go up and even staying the same becomes doubtful this leaves:

3. Down Again.