{kind=link}

Big move for vol of vol

(October 17, 14)

Courtesy of SoberLook.com

Staying with the volatility theme, the latest jump in VIX was clearly dwarfed by what we saw in 2008 or even in 2011. However that's not true for the volatility of VIX – the so-called "vol of vol". The CBOE's VVIX Index, "an indicator of the expected volatility of the 30-day forward price of the VIX" (see description), has been comparable to or higher than what we saw during those high stress periods. The possibility of VIX doubling or even tripling ("tail" risk) does not seem outside of the realm of possibilities these days – even from the current elevated levels. And traders are willing to pay a relatively high premium to be able to take advantage of such moves.

Previously…

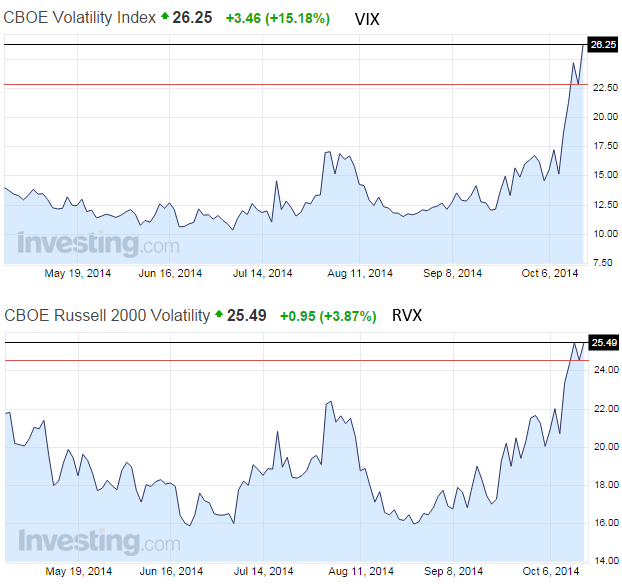

Implied vol dislocation

(October 16, 14)

The recent spike in volatility has created a "dislocation" in US equity options markets. VIX, which is a measure of implied volatility for large cap shares is now higher than RVX – the small-cap equivalent. This is highly unusual, since small caps tend to be more volatile. Part of the issue is the outsized spike in the volatility of large energy shares due to the recent sell-off in crude oil.

Sign up for Sober Look's daily newsletter called the Daily Shot.