{kind=link}

Courtesy of Sabrient Systems and Gradient Analytics

U.S. stocks found support once again last week and rallied on strong volume. Of course, the main catalyst was the FOMC policy statement on Wednesday that maintained its dovish language with a pledge of considerable time before raising the fed funds rate and adding that it would be patient as it begins the process of normalizing monetary policy. The result was yet another classic V-bottom. Ho, ho, ho. Say hello to Santa Claus.

In this weekly update, I give my view of the current market environment, offer a technical analysis of the S&P 500 chart, review our weekly fundamentals-based SectorCast rankings of the ten U.S. business sectors, and then offer up some actionable trading ideas, including a sector rotation strategy using ETFs and an enhanced version using top-ranked stocks from the top-ranked sectors.

Market overview:

For the week, the S&P 500 had a total return of +3.4%, led by a huge +9.7% bounce in beleaguered Energy sector. Basic Materials also looked strong with a +5.0% rally. For the year, the S&P 500 is up nearly +12% through Friday. And then on Monday of this week, the S&P 500 logged a new closing high, although the intraday high from December 5 still stands. Last Thursday’s big move resulted in a 421-point gain for the Dow Jones Industrials, which was its best one-day performance in three years, and the 709 points totaled on Wednesday and Thursday was its best two-day performance since 2008.

With Santa lurking on the horizon, bears have run for cover from the charging bulls. Moreover, Fundstrat reported that 71% of active fund managers are trailing their respective benchmarks, which would be the worst such percentage since 1998. So, they needed to do some catch up in accumulating U.S. equities. Notably, 1998 closed with a similar end-of-year rally. Also, this is the time of year in which many companies announce increases to their dividend payments. And don’t forget, this year’s IPO market has been the busiest since the crazy days of 2000, with 273 new IPOs (compared with 406 in 2000) and $85 billion raised (vs. $97 billion in 2000).

Crude oil has fallen -48% below the June highs, so it’s not surprising that the Energy sector led last week’s big rally. At current levels, there is more upside potential than further downside and a solid long-term risk/reward profile. And given the surge in insider buying, company executives seem to agree. Nevertheless, some prominent London hedge funds have been adding to their short positions in European companies with the highest sensitivity to falling oil prices, so not everyone thinks the bottom is in.

In desperate response to plunging oil revenues and the resultant plunging ruble from capital flight, Russian president Putin jacked rates by +6.5% up to 17%, thus providing the intense pressure that economic sanctions could not. (And the timing of President Obama’s move to normalize relations with Cuba probably was related.)

Nominal GDP is up +4.0% over the past year. The Conference Board Leading Economic Index has shown steady improvement and gaining momentum all year. And as we complete Q3 earnings season and look ahead to Q4 reports, sell-side analysts are anticipating EPS of $29.92 for the S&P 500 companies, which is an increase of +5.5% from Q4 2013, and total 2014 EPS growth is expected to come in at +7.5%, compared with +4.5% for 2013. This would be the best earnings growth since 2011’s +14.3%.

With a patient and friendly Fed providing ongoing tailwinds, strong GDP growth should continue into 2015 and beyond, which should propel equities to further heights, although the future for long-term bond prices is not so clear. Although the near-term will likely provide a flattening yield curve, eventually economic health will demand higher long-term rates and a steeper yield curve.

While 2015 appears to be shaping up similarly to 2014, i.e., lower equity correlations, higher volatility, and modest increase in U.S. equities, some observers are suggesting investors gain greater exposure to less directional equity strategies, such as long/short, long-hedged strategies, and market neutral. Also, many believe that given the dominance in large caps this year, we will need to see outperformance from small caps, and perhaps emerging markets.

Sabrient’s annual Baker’s Dozen portfolio of 13 top picks for the year is up about +22% since its January 13 launch through Friday’s close, while the S&P 500 is up +16% over the same timeframe. Top performers include Southwest Airlines (LUV) and NXP Semiconductors NV (NXPI). Baker’s Dozen represents a sector-diversified group of stocks based on our Growth At a Reasonable Price (GARP) quant model and confirmed by a rigorous forensic accounting review by our subsidiary Gradient Analytics to help us avoid the landmines. It is packaged as a unit investment trust (UIT) by First Trust Portfolios (note: the new 2015 Baker’s Dozen portfolio will launch on January 14).

Sabrient also publishes a handful of thematic indexes that are tracked by various ETFs. Year-to-date, while the S&P 500 is up about +11.8%, the Direxion All Cap Insider Sentiment ETF (KNOW) is up +17.6%, the Guggenheim Defensive Equity ETF (DEF) is up +13.3%, and the Guggenheim Insider Sentiment ETF (NFO) is up +5.7% (flat performance for second half of year caused it to lag).

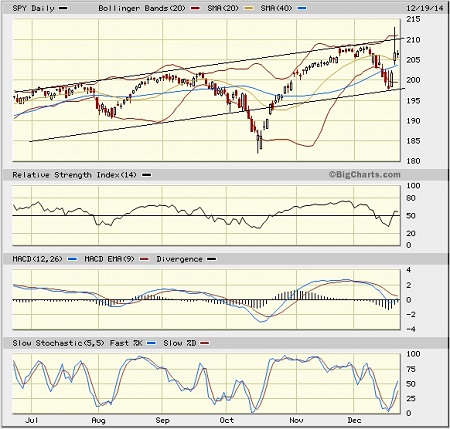

SPY chart review:

The SPDR S&P 500 Trust (SPY) closed Friday at 206.52 (and then on Monday this week it hit a new closing high of 207.47). As I suggested it might, the SPY found solid support last week and stabilized while working off its severely overbought technical condition and reconfirming bullish conviction. Oscillators RSI, MACD, and Slow Stochastic all have reversed and look strong for further upside. Support levels include the 20-day simple moving average near 205, the 50-day SMA at 201, the 100-day SMA at 199, the bottom of the bullish rising channel around 198, and the 200-day SMA at 195. Overhead resistance resides at current levels (new highs), followed by the top of the bullish rising channel around 210.

I am still hopeful that last week’s technical pullback was what the market needed in order to avoid a more dramatic downside event in early January.

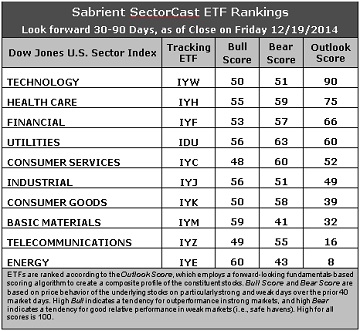

Latest sector rankings:

Relative sector rankings are based on our proprietary SectorCast model, which builds a composite profile of each equity ETF based on bottom-up aggregate scoring of the constituent stocks. The Outlook Score employs a forward-looking, fundamentals-based multifactor algorithm considering forward valuation, historical and projected earnings growth, the dynamics of Wall Street analysts’ consensus earnings estimates and recent revisions (up or down), quality and sustainability of reported earnings (forensic accounting), and various return ratios. It helps us predict relative performance over the next 1-3 months.

In addition, SectorCast computes a Bull Score and Bear Score for each ETF based on recent price behavior of the constituent stocks on particularly strong and weak market days. High Bull score indicates that stocks within the ETF recently have tended toward relative outperformance when the market is strong, while a high Bear score indicates that stocks within the ETF have tended to hold up relatively well (i.e., safe havens) when the market is weak.

Outlook score is forward-looking while Bull and Bear are backward-looking. As a group, these three scores can be helpful for positioning a portfolio for a given set of anticipated market conditions. Of course, each ETF holds a unique portfolio of stocks and position weights, so the sectors represented will score differently depending upon which set of ETFs is used. We use the iShares that represent the ten major U.S. business sectors: Financial (IYF), Technology (IYW), Industrial (IYJ), Healthcare (IYH), Consumer Goods (IYK), Consumer Services (IYC), Energy (IYE), Basic Materials (IYM), Telecommunications (IYZ), and Utilities (IDU). Whereas the Select Sector SPDRs only contain stocks from the S&P 500, I prefer the iShares for their larger universe and broader diversity. Fidelity also offers a group of sector ETFs with an even larger number of constituents in each.

Here are some of my observations on this week’s scores:

1. The rankings continue to remain stable, as Technology and Healthcare stay at the top. Technology ranks first with a robust Outlook score of 90. Tech stocks display the best return ratios, a good forward long-term growth rate, a reasonably good forward P/E, and decent support among insiders (buying activity). Healthcare scores a 75 and displays good sell-side analyst support (recent upward revisions to earnings estimates), a strong forward long-term growth rate, solid insider sentiment (buying activity), and good return ratios, although its forward P/E is on the high side. Financial remains in third with a score of 66, and it displays the best (lowest) forward P/E. Rounding out the top six are Utilities, Consumer Services/Discretionary, and Industrial. Notably, stocks within the Consumer Services/Discretionary (a.k.a., Cyclicals) sector held up well during the recent market weakness and the sector continues to get the greatest support from both analysts and insiders while boasting the highest forward long-term growth rate.

2. Energy continues to hold the bottom spot, primarily due to Wall Street analysts continuing to revise downward their earnings expectations and reduce the forward long-term growth rate. Also, insiders have slowed their open market buying activity, and with last week’s price recovery, the forward P/E is higher (worse). Joining Energy in the bottom two again is Telecom, which generally scores poorly across the board in most factors in the Outlook model.

3. Looking at the Bull scores, Energy suddenly surged to the top with a score of 60, based on last week’s strong performance during the market’s huge rally. Basic Materials is close behind at 59. Consumer Services/Discretionary scores the lowest at 48. The top-bottom spread is only 12 points, which still reflects high sector correlations during particularly strong market days, i.e., highly-correlated risk-on action. But it is generally desirable in a healthy market to see low correlations and a top-bottom spread of at least 20 points, which indicates that investors have clear preferences in the stocks they want to hold, rather than the all-boats-lifted-in-a-rising-tide (risk-on) mentality.

4. Looking at the Bear scores, Utilities again displays the highest score of 63 this week, as one would expect for this traditionally defensive sector. Utilities stocks have been the preferred safe havens on weak market days, and it is followed closely by Consumer Services/Discretionary (somewhat surprisingly), and then Healthcare and Consumer Goods/Staples. Basic Materials displays the lowest score of 41, followed by Energy. The top-bottom spread is a wide 22 points (although it is tighter than last week’s 29), reflecting low sector correlations on particularly weak market days. In other words, certain sectors are holding up relatively well while others are selling off. Again, it is generally desirable in a healthy market to see low correlations and a top-bottom spread of at least 20 points.

5. Technology displays the best all-around combination of Outlook/Bull/Bear scores, followed closely by Healthcare, while Energy is the worst. Looking at just the Bull/Bear combination, Utilities and Healthcare are the clear leaders, indicating superior relative performance (on average) in extreme market conditions (whether bullish or bearish). Basic Materials is the worst, indicating general investor avoidance.

6. Overall, this week’s fundamentals-based Outlook rankings still look bullish to me, particularly given the continued strength in Consumer Services/Discretionary. Five of the top six sectors are economically-sensitive (or in the case of Healthcare, all-weather), and they also display generally strong Bull scores. Keep in mind, the Outlook Rank does not include timing or momentum factors, but rather is a reflection of the fundamental expectations of individual stocks aggregated by sector.

Stock and ETF Ideas:

Our Sector Rotation model, which appropriately weights Outlook, Bull, and Bear scores in accordance with the overall market’s prevailing trend (bullish, neutral, or defensive), continues to indicate a bullish bias this week, and it suggests holding Healthcare, Basic Materials, and (new surprise!) Utilities, in that order. (Note: In this model, we consider the bias to be bullish from a rules-based trend-following standpoint because SPY is above both its 50-day and 200-day simple moving averages.)

Other highly-ranked ETFs from the Healthcare, Basic Materials, and Utilities sectors include iShares Nasdaq Biotechnology ETF (IBB), PowerShares DWA Basic Materials Momentum Portfolio (PYZ), and Fidelity MSCI Utilities Index ETF (FUTY).

For an enhanced sector portfolio that enlists some top-ranked stocks (instead of ETFs) from within the top-ranked sectors, some long ideas from Healthcare, Basic Materials, and Utilities sectors include United Therapeutics (UTHR) C.R. Bard (BCR), LyondellBasell Industries (LYB), The Sherwin-Williams Company (SHW), Pinnacle West Capital (PNW), and Consolidated Edison (ED). All are highly ranked in the Sabrient Ratings Algorithm and also score within the top two quintiles (lowest accounting-related risk) of our Earnings Quality Rank (a.k.a., EQR), a pure accounting-based risk assessment signal based on the forensic accounting expertise of our subsidiary Gradient Analytics (except for the Utilities stocks, which are not covered by EQR). We have found EQR quite valuable for helping to avoid performance-offsetting meltdowns in our model portfolios.

However, if you prefer to maintain a neutral bias, the Sector Rotation model suggests holding Technology, Healthcare, and Financial, in that order. And if you prefer a defensive stance on the market, the model suggests holding Utilities, Healthcare, and (surprise!) Consumer Services/Discretionary, in that order.

IMPORTANT NOTE: Some readers have been asking for more specifics on how to trade our sector rotation strategy based solely on what I discuss in my weekly newsletter. Thus, I feel compelled to remind you that I post this information each week as a free look inside some of our institutional research and as a source of some trading ideas for your own further investigation. It is not intended to be traded directly as a rules-based strategy in a real money portfolio. I am simply showing what a sector rotation model might suggest if a given portfolio was due for a rebalance, and I may or may not update the information each week. There are many ways for a client to trade such a strategy, including monthly or quarterly rebalancing, perhaps with interim adjustments to the bullish/neutral/defensive bias when warranted — but not necessarily on the days that I happen to post this weekly article. The enhanced strategy seeks higher returns by employing individual stocks (or stock options) that are also highly ranked, but this introduces greater risks and volatility. I do not track performance of the ETF and stock ideas mentioned here as a managed portfolio.