{kind=link}

Courtesy of Charles Hugh-Smith of Of Two Minds

The end of rising wages = the end of mass affluence: we just enjoyed the Last Christmas in America (TLCIA).

As unemployment topped 10%, the January 1975 cover of Ramparts magazine blared: The End of Affluence: The Last Christmas in America. (TLCIA)

The government responded to the high unemployment, rampant inflation and rising budget deficits by manipulating data to mask the politically inconvenient realities of inflation, unemployment and deficits by playing with Social Security Trust Funds, inflation data, etc.–games it continues to play to cloak reality from the media-numbed public.

The economic stagnation, despite various stock market rallies and false starts, essentially lasted 10 years, from 1973 to 1982.

The malaise had a happy ending: huge new oil fields were discovered in Alaska, the North Sea, West Africa and elsewhere, ushering in a renewed era of cheap, abundant petroleum. President Reagan re-set Social Security for a generation and introduced a lower taxes, higher permanent deficits ideology that is now accepted as the only possible way to sustain the Status Quo: deficits don't matter, even when they reach the trillions, because our good friends the Gulf Oil Exporters and Asian exporters will buy all our debt forever and ever, keeping interest low forever and ever.

(And if they drop the ball, then the Federal Reserve prints money and buys trillions of dollars of Treasury bonds. Sweet! We don't need any external buyers, just the Federal Reserve creating money out of thin air.)

Then the U.S. created and launched two revolutionary technologies which both created new wealth around the globe: the personal computer (microprocessor and cheap RAM) and the Internet (TCP/IP, Ethernet, and the commercialization of Tim Berners-Lee's World Wide Web with free browsers) spawning the generation-long boom of the 1980s and 90s.

Those "saves from stagnation" were one-offs; there will be no more supergiant energy finds, nor any equivalents of the Internet expansion cycle.

When the wheels inevitably fell off the Internet/tech boom in 2000, the U.S. did not create a new engine of wealth: it opted instead for a devilishly insidious simulacrum of wealth: debt which rose at an exponential rate throughout the economy.

Borrowed money and phony financial legerdemain (mortgage-backed securities, derivatives based on the MBS, etc. etc.) from 2000-2007 created what I have termed a "bogus prosperity": no actual new productive wealth was created, only a brief and self-liquidating bubble of debt-based housing and stock valuations.

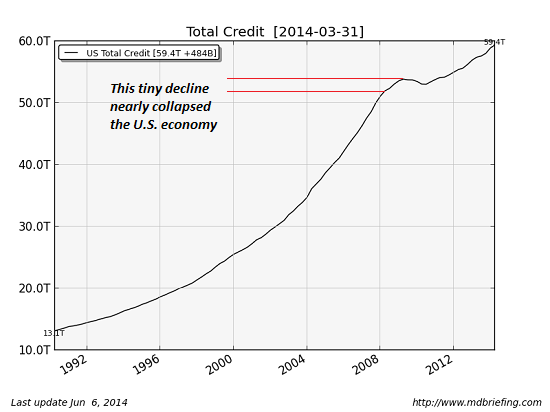

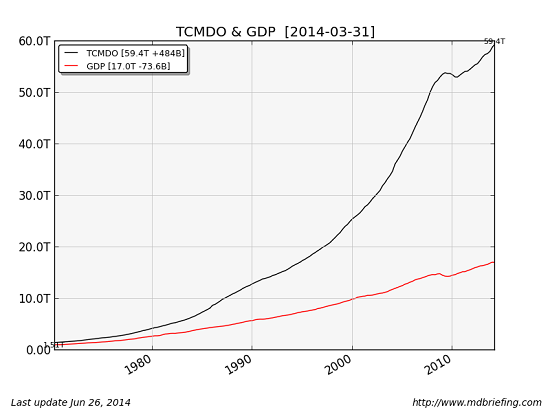

Compare the rate of GDP growth (another unreliable indicator, but all we have) with the astonishing rise in debt:

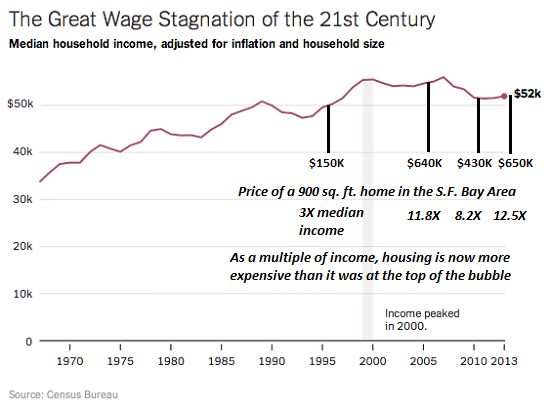

Meanwhile, wages adjusted for inflation have stagnated for 15 years while asset prices for stores of value such as housing in desirable areas have skyrocketed in terms of median household income:

Real household income has declined in the Bubble Era across the entire income spectrum:

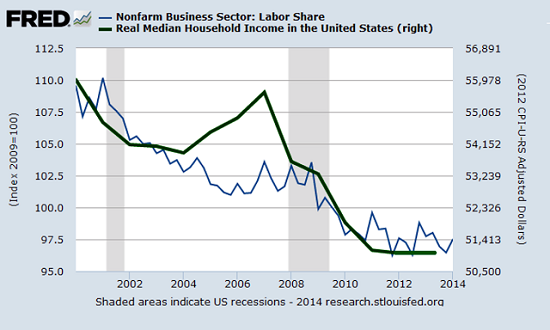

Here is real median household income and labor's share of the economy: both are in structural decline, and inflating asset bubbles has done nothing to reverse either trend.

Why will Christmas 2014 be the last Christmas in America? It's simple: declining wages cannot support an ever-expanding mountain of debt.

The Federal Reserve has played a game for six long years of lowering the cost of debt (i.e. the rate of interest borrowers must pay), which has enabled stagnating wages to support ever heavier debt loads.

There is an endgame in sight to this financial trickery, a point of diminishing returns to lower interest rates: the Fed can't drop rates lower than 0%. Borrowers simply can't qualify for more debt, regardless of interest rates.

The extreme fragility of an economy based on ever-expanding mountains of debt piled on declining incomes is apparent: if the Fed can't raise interest rates even a tiny quarter point without threatening to collapse the unstable pyramid of debt-based affluence/ consumption, what does that say about the fragility of the "growth" (supposedly running at a hot 5% annually) and "prosperity"?

Claiming that a few hundred dollars in lower gasoline costs per household will enable a desert of declining income to bloom is the equivalent of claiming that an inch of rain in Death Valley will transform the desert into a lush tropical rain forest.

Remember the lackluster Christmas of 2014; the endgame of expanding debt will play out as every endgame does: furious moves by central bankers will prolong checkmate but not transform the inevitable loss into a win. Media sound and fury are no substitute for rising real household wages and incomes.