{kind=link}

Is there a Relationship Between the Economy and Stock Market?

Long story short… yes, there appears to be a relationship between economic growth and stock market performance within the U.S. (and developed world), but that relationship holds only over longer periods of time and does not hold for all countries (less developed countries often "divert" growth to the political elite).

Also, for those interested in the relationship between long-term economic growth and returns across countries, Dimson, Marsh, and Staunton provide a ton of interesting analysis going back 100+ years within the Credit Suisse Investment Returns Yearbook (Figure 13 on page 28). The high level takeaway: "Though difficult for investors to capture in portfolio returns, strong GDP growth is generally good for investors."

For now… below are two pieces of analysis that outline what I feel drive the relationship between underlying economic growth and the U.S. stock market;

- The economy's impact on valuation (economic growth provides a base for corporate earnings, which drives valuations, which drives returns)

- Economic contractions that severely impact stock market performance

U.S. Economy vs. U.S. Stock Market – The Valuation Story

The best part about taking an almost 3 year hiatus from blogging is that I can recycle about 90% of my previous ideas and they will seem new. Here is one I initially ran in May 2010, then revised to the format below in February 2012. The background of this is that over the long run, equity valuations and earnings have both grown at roughly the same pace as nominal GDP. This makes intuitive sense… while earnings can absolutely grow slower than the economy (especially in emerging markets with less developed investor protection), if they consistently grew faster than the economy, then earnings would eventually become larger than the entire economy (not possible).

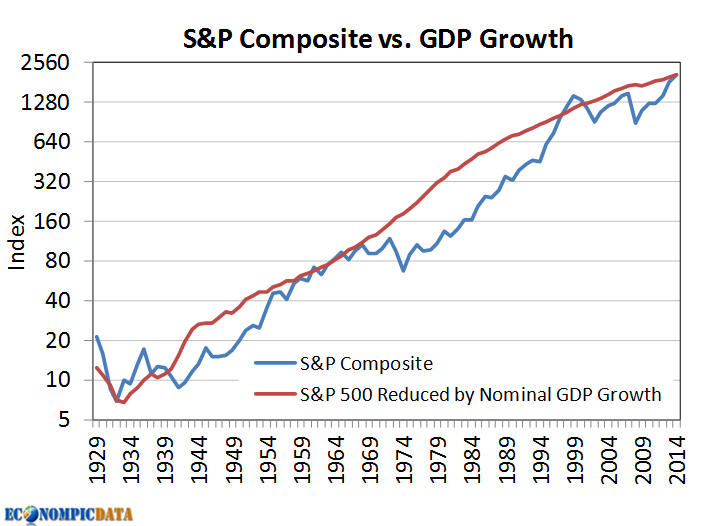

With that in mind, the below chart shows:

- Blue: the S&P index

- Red: the ending 2014 value is set to the 2014 year-end value of the S&P 500 index, then brought back in time by the nominal GDP growth rate (GDP data is available at the Bureau of Economic Analysis) – 1929 is the first year the BEA produces annual GDP growth rate

This is an attempt to compare the S&P's historical valuation relative to the size of the US economy, relative to the current level of that relationship. When the S&P 500 (blue) is below the nominal GDP line (red), then the S&P 500 was cheaper on this relative measure than it is now (when the lines cross valuation levels were equal to those in place today).

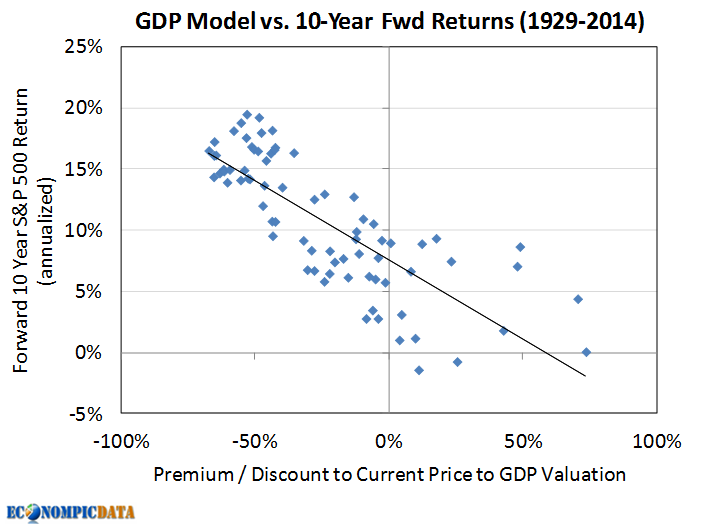

The chart below shows the relative valuation for each year from 1929 through 2004 (relative to its current value of 0; again if less than 0, the S&P was cheaper by this measure), along with the subsequent 10 year forward change in the S&P 500 total return (annualized). This chart outlines that historically there has been a significant relationship between the underlying economy and stock market. When the S&P composite has grown at a slower rate than the U.S. economy, making it cheap, this has led to historical outperformance.

Of note… there have been many more periods when the stock market was less expensive than the current level, yet the trend-line goes through 0% (the current valuation) on the x-axis at roughly 7.5% annualized (noisy data, but it makes current valuations less stretched than some would think).

U.S. Economy vs. Stock Market – Avoid Economic Contractions if Possible

While the above analysis outlines that the relationship between the economy and stock market generally holds over longer time frames, there has been a relationship worth mentioning over shorter time frames. Going back to the first quarter of 1947 (as far back as the BEA releases quarterly real GDP) and separating quarterly S&P 500 performance when real GDP was either positive or negative, we see a pretty material difference in performance. Not only were returns much better when GDP was expanding vs. contracting (real returns have actually been negative during economic contractions), but returns were much more volatile when the economy was contracting.