{kind=link}

Weekly Market Summary

Courtesy of Urban Carmel (originally published on Aug. 1)

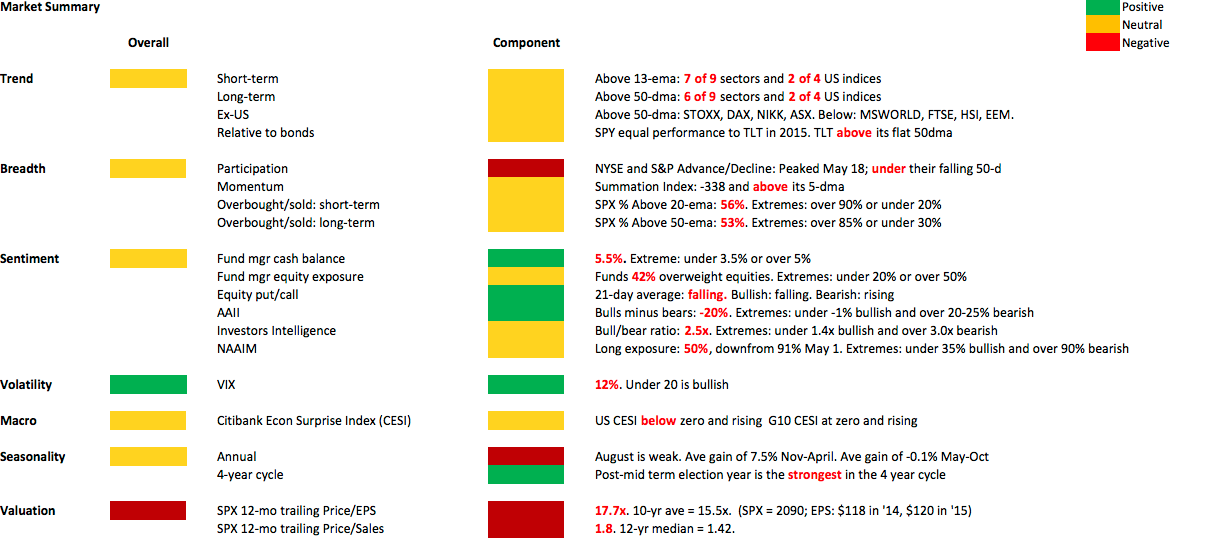

Summary: There are several breadth and sentiment indicators that suggest the indices have reached, or are near, a one month low. But more importantly, for the first time in awhile it is possible to see an endgame to the sideways trading range that has persisted in 2015. A break lower soon, should it occur, would likely lead to a washout low. This is the set up for US equities as seasonally weak August begins.

Our view at the end of 2014 was that 2015 was likely to be unremarkably flat. This was to be a year where stock appreciation would take a break while sentiment and valuations cooled off and the economy improved (post).

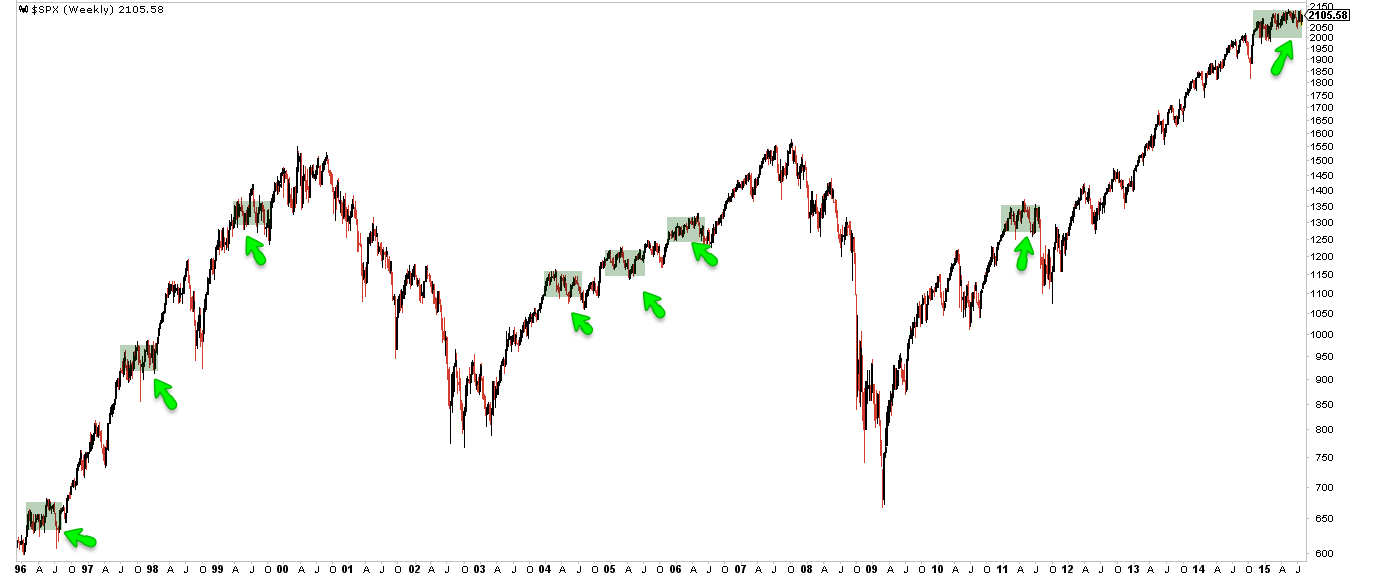

Sideways markets are not unusual. Periods like the one we are in now can last as long as two years. There is no decisively bearish implication of a sideways market either. It is, in fact, a pattern that is common within every bull market, a period of rest between periods of rapid price appreciation. We reviewed this topic in detail here. Similar instances to today are shown below (this and all charts expand when clicked).

But flat markets can feel bearish in real-time. Moving averages bunch closer together. This makes it easy to have a lot of companies trading below their 50-day or their 200-day average even while the index is close to a high. This makes breadth measurements look weak.

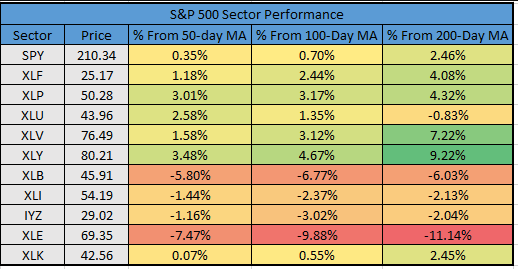

Right now, about 50% of the companies in the S&P are trading below their 50-dma and 44% are below their 200-dma. This is, on the surface, very weak breadth. But these numbers are skewed primarily by two sectors, energy and materials, both of which have been impacted by the strong dollar and weak commodity prices. All the other sectors are either above their averages or only slightly below (data from Ryan Detrick).

In the table above, also note that for the weakest sectors, the difference between the 50-dma and the 200-dma is only slight. Again, in a prolonged flat market, the averages bunch together. Energy and materials aside, it would take only a modest gain for the others to all move back above the averages. This would restore breadth to something that is more healthy.

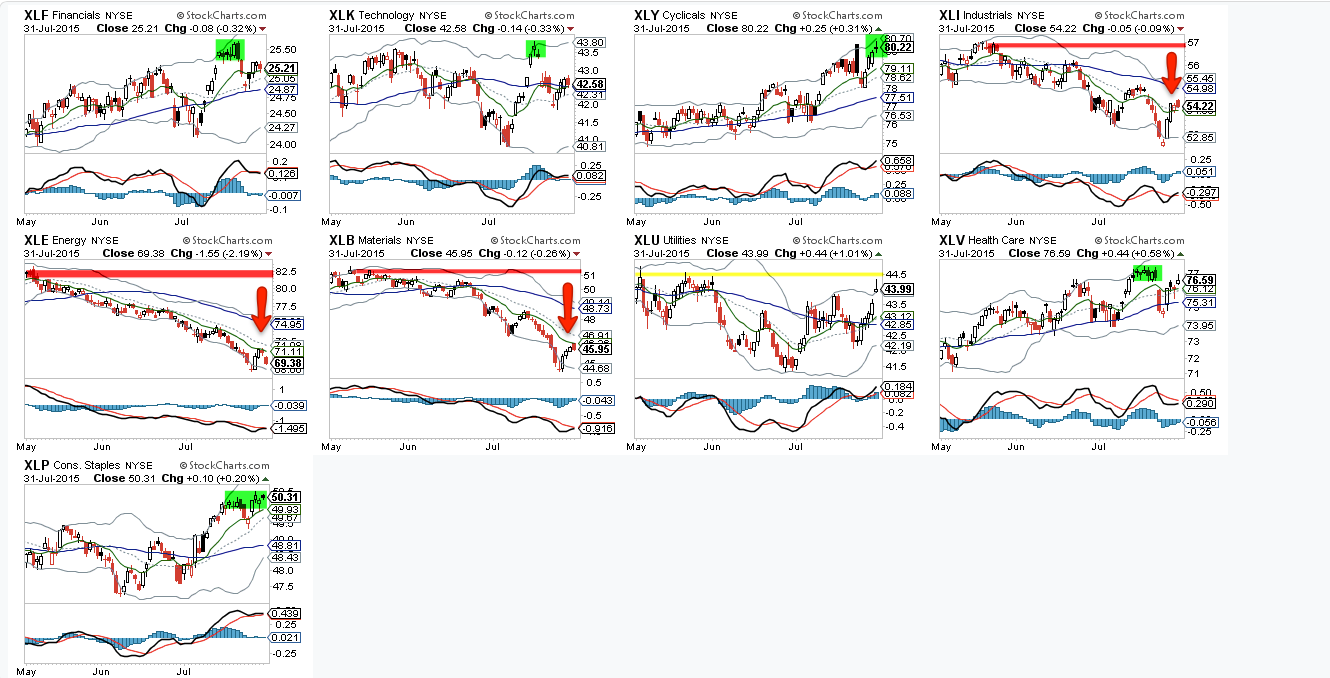

It's also worth noting that 5 sectors made bull market highs this month: financials, technology, discretionary, staples and healthcare. Utilities ended July at close to a 3 month high. The weakness is, again, primarily concentrated in energy and materials with industrials (which includes transports) weak to a lesser extent.

Does poor breadth lead inevitably to a major market correction? The answer is no.

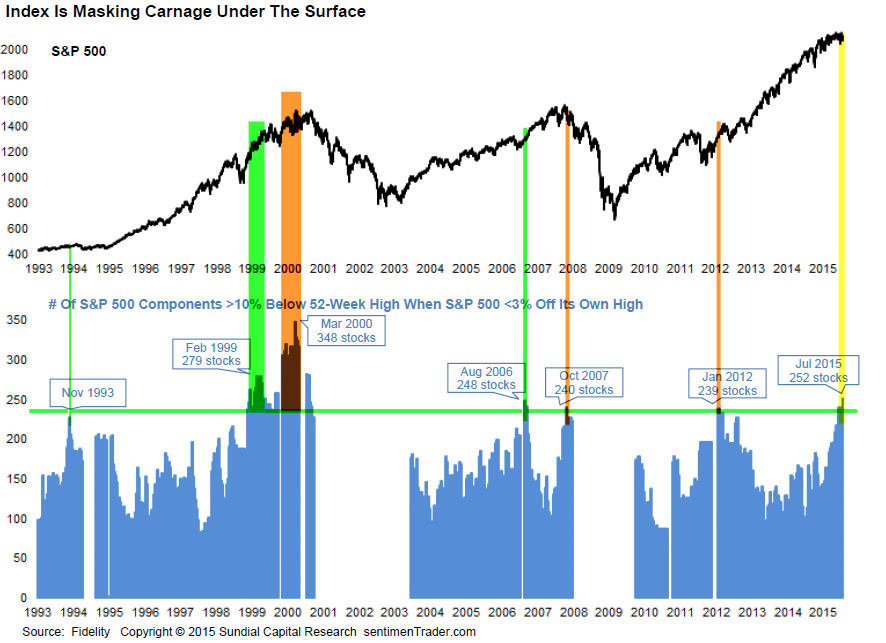

The chart below looks at other instances where half the S&P traded 10% from their 52-week high while the index was near a high. This occurred near two tops (2000 and 2007) and near a 10% correction (2012) but also in the middle of several uptrends (1993, 1999 and 2006). There could be a correction now, in 6 months or years later. The signal to noise ratio is weak, probably because gross measures of breadth do not distinguish which or how many sectors are weak (data from Sentimentrader).

We think it is more actionable to think of breadth in terms of extremes that mark turning points. Poor breadth reaches a washout level where indices tend to bottom and rebound.

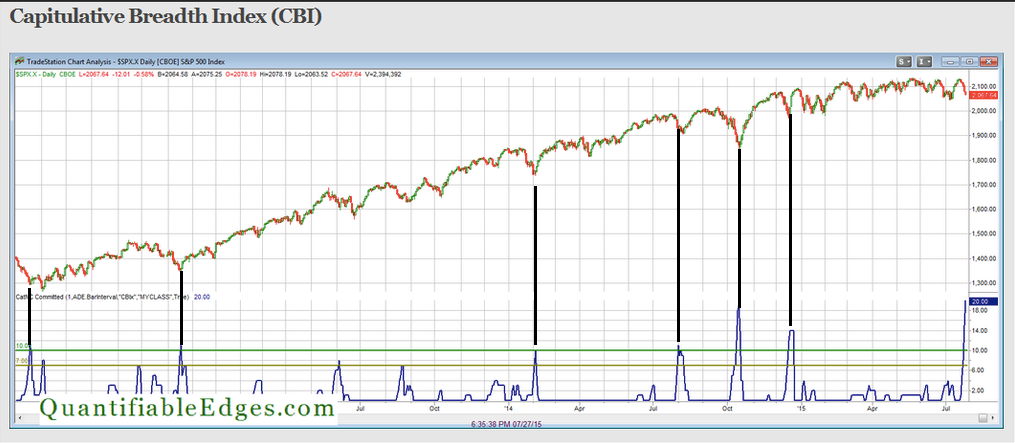

An example of this is the Quantifiable Edges Capitulative Breadth Indicator (CBI), which hit 20 on Monday. Extremes like this have occurred just 23 times in the past 20 years; a month later, SPY has been higher every time. This suggests SPY will be still be above 208 three weeks from now. Read further here.

One of the other features of sideways markets is that investors eventually become worn out. Bearish sentiment can rise from falling prices or through time with price making little headway. We are beginning to see this now.

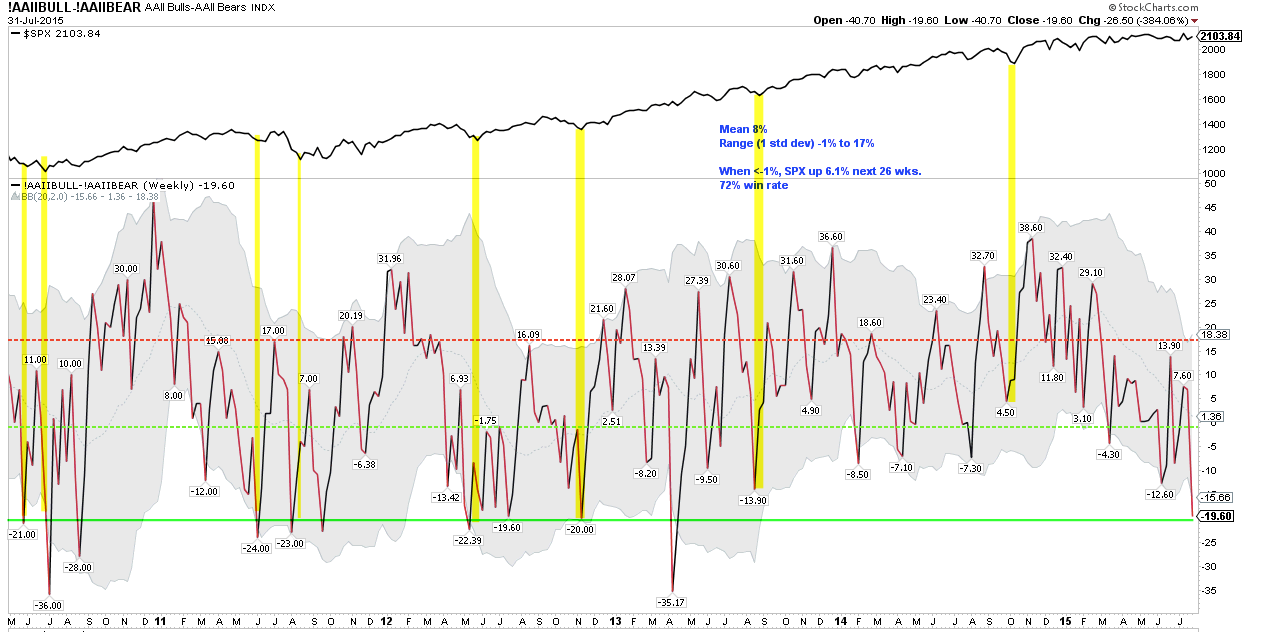

The spread between bullish and bearish individual investors (AAII) is now the most negative since 2012 (the low print in 2013 was due to a sampling error). It is about 2 standard deviations below the mean. In the past, the S&P has bounced higher from these levels. In 2011 and 2012, those bounces failed and a lower low formed 1-2 months later. In this sample at least, none of the instances led directly into a major correction.

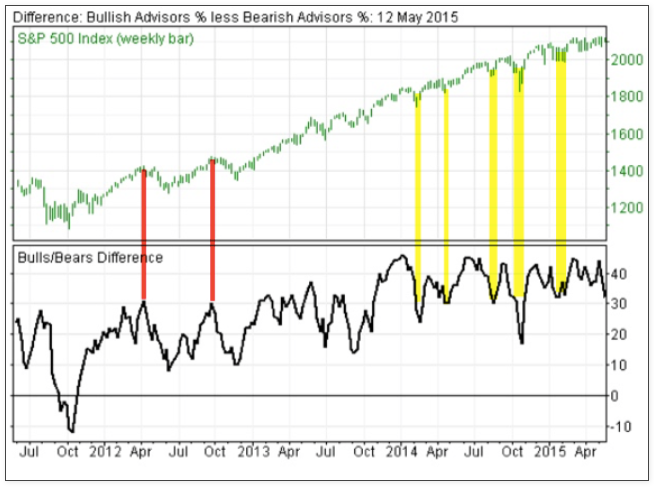

Investment advisors are still bullish; the most recent Investors Intelligence bull/bear spread was 26%. But this is the lowest spread since the S&P lows in October and February 2014. In 2012, this level would have marked a bullish extreme (red lines). Since then, it has marked several lows (yellow).

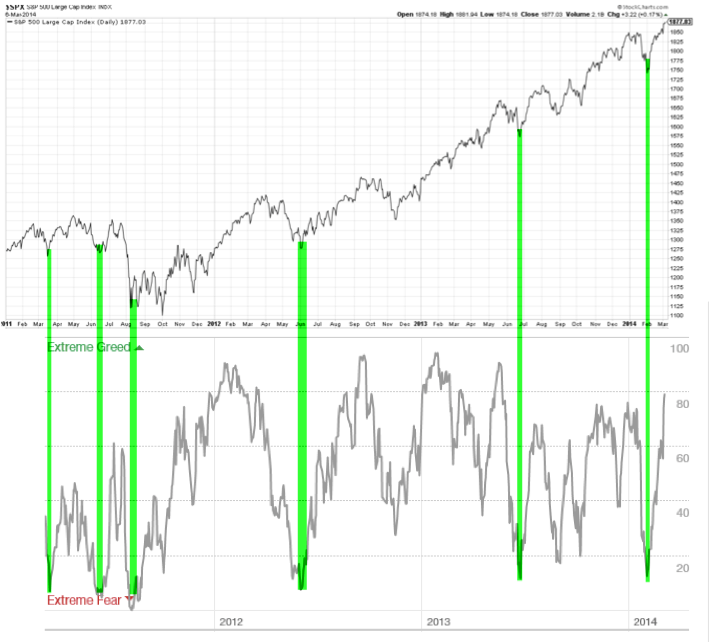

The Fear & Greed index closed at 7 on Monday. This was the lowest since October 2014. Extreme lows have marked at least one month lows in the S&P the past 5 years (the chart below covers 2011-2014).

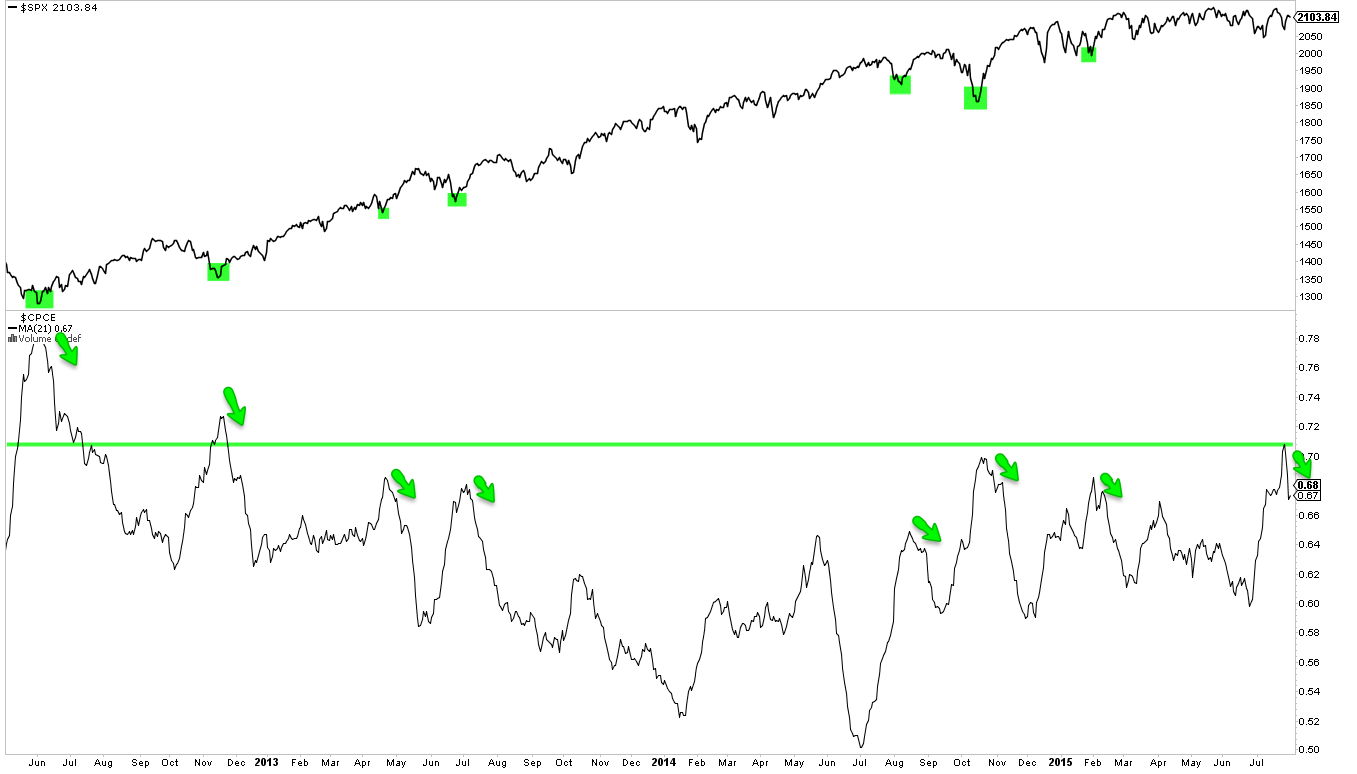

The 21-day equity-only put/call ratio is now clearly declining from a 2 1/2 year high. Spikes higher that then recede like this one have marked at least one month lows.

If the recent pattern continues, sentiment suggest the markets should move higher, at least short term.

Should the markets instead rollover, a washout low, with a more durable bottom, could finally be formed. That might mark the end of the sideways trading environment that has persisted in 2015. Sentiment is already weakening. Some measures are already at an extreme. A rollover lower would likely pull Investors Intelligence, NAAIM and the BAML survey of fund managers into an extreme as well.

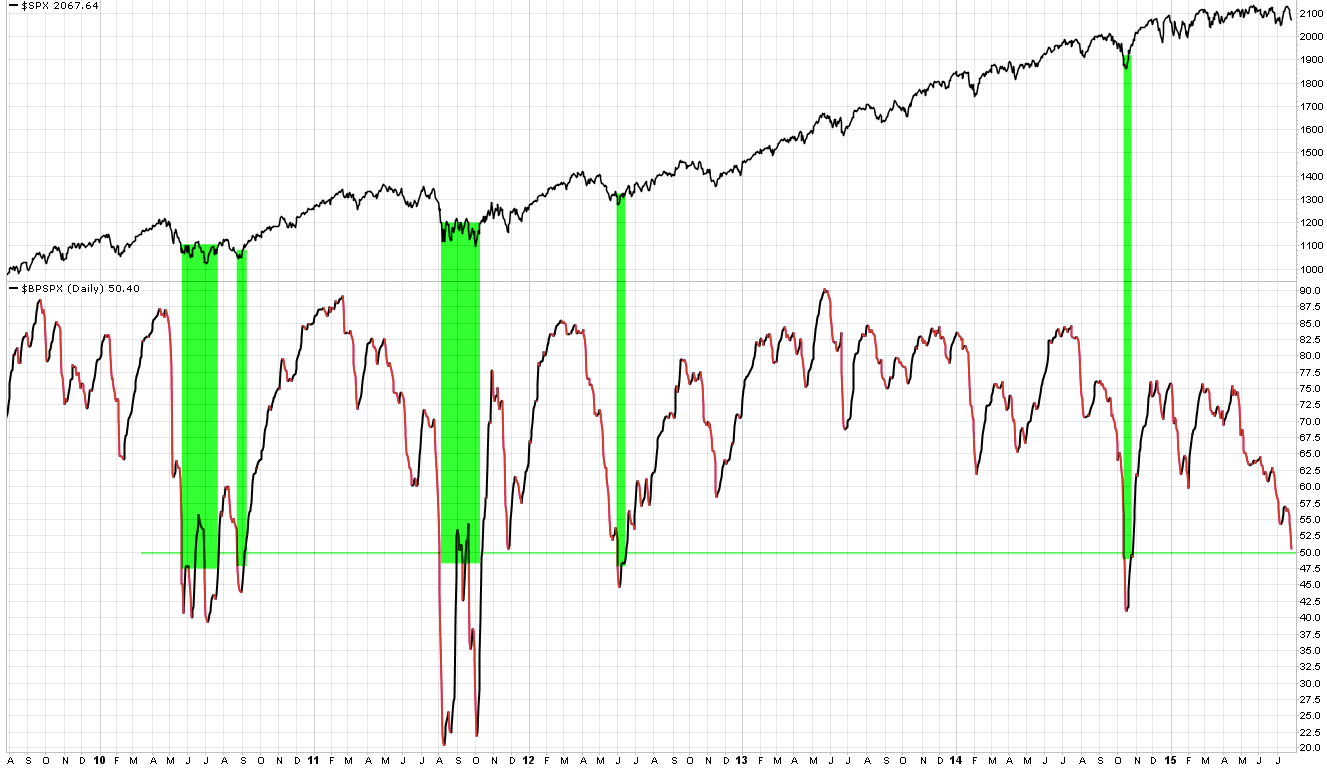

As an example of how this might occur, the bullish percent index (BPI) is already at the edge of what has been a low. BPI is a breadth measure that counts the number of stocks on point and figure buy signals. It reach 50% on Monday; in the chart below, you can see that even the 2010 and 2011 corrections ended when BPI fell under 50%. A drop lower in price soon, with BPI already weak, would likely set up a durable low.

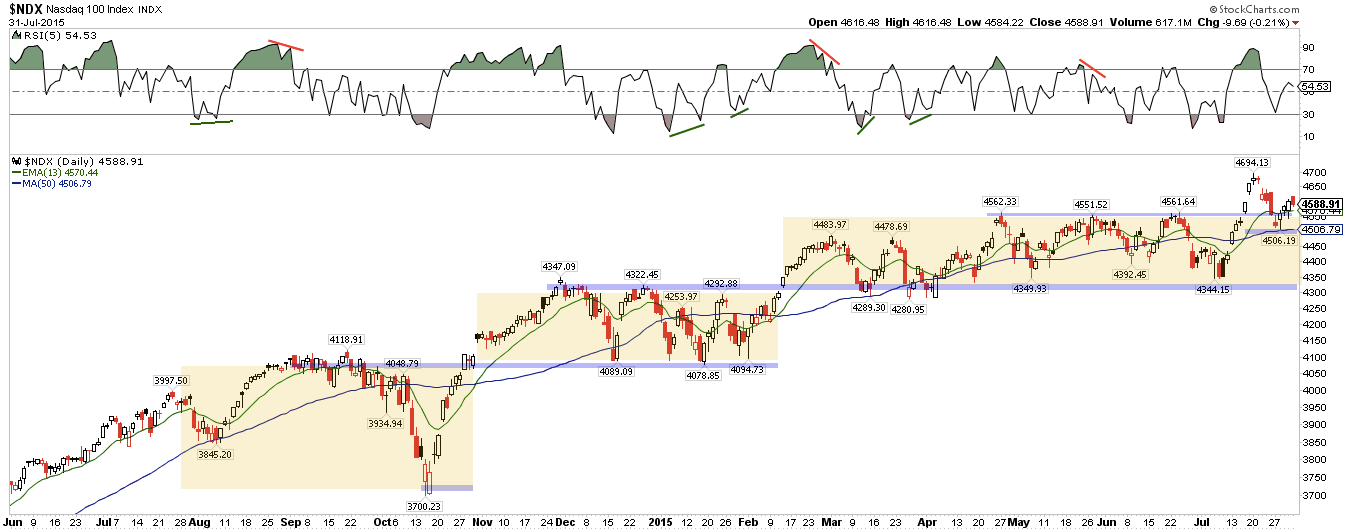

Price action was mediocre this week. Recall that price was poised to rebound at the end of last week (post). In the event, all the indices moved higher. SPX and RUT gained 1% but NDX and DJIA gained just 0.7%. But after a 5 day drop, this was a tepid rebound. Let's review.

The Dow fell to a 6 month low on Monday before rebounding. But the rebound did not even recover the fall from a week ago on Friday, and price barely closed within the bottom of the last 6 months' range. This is not strong and looks more likely to eventually continue lower.

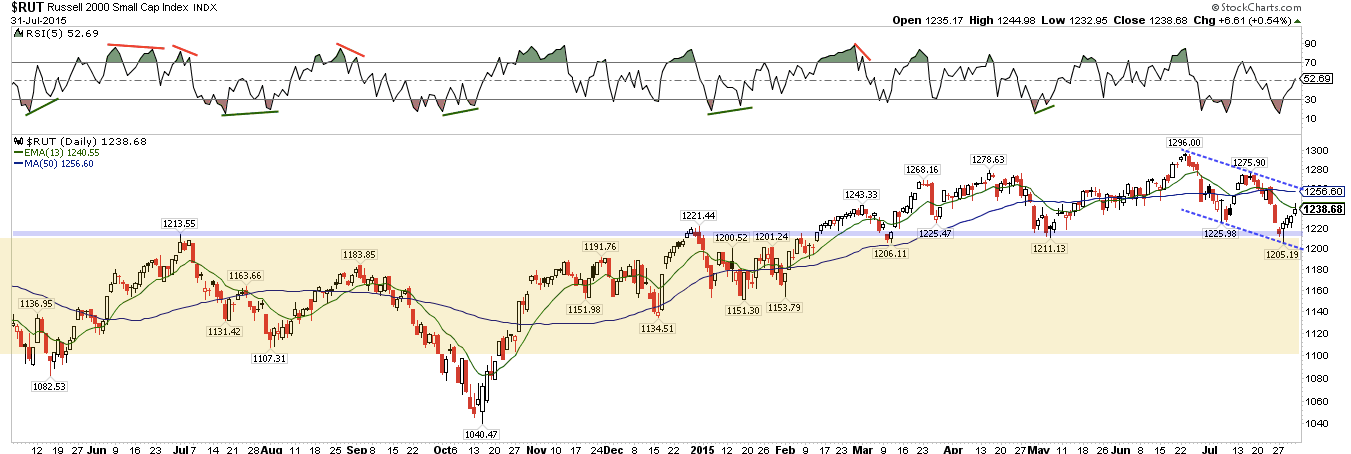

Small caps were only slightly better. RUT bounced right on its prior trading range top (shaded area) but the subsequent 4 days of gains amounted to less than the one day drop last Friday. There are lower highs and lows and thus a falling channel. At the low, price touched its 200-dma; the first touch is usually good for a bounce (as it was this week), but a quick return likely fails.

The leader, NDX, has been stair stepping higher in the past year. But Monday's sell off overlapped with the prior "stair" and the rebound didn't even retrace the Friday drop. Since March, NDX has been bouncing along its 50-dma every other week. That pattern looks like it will continue.

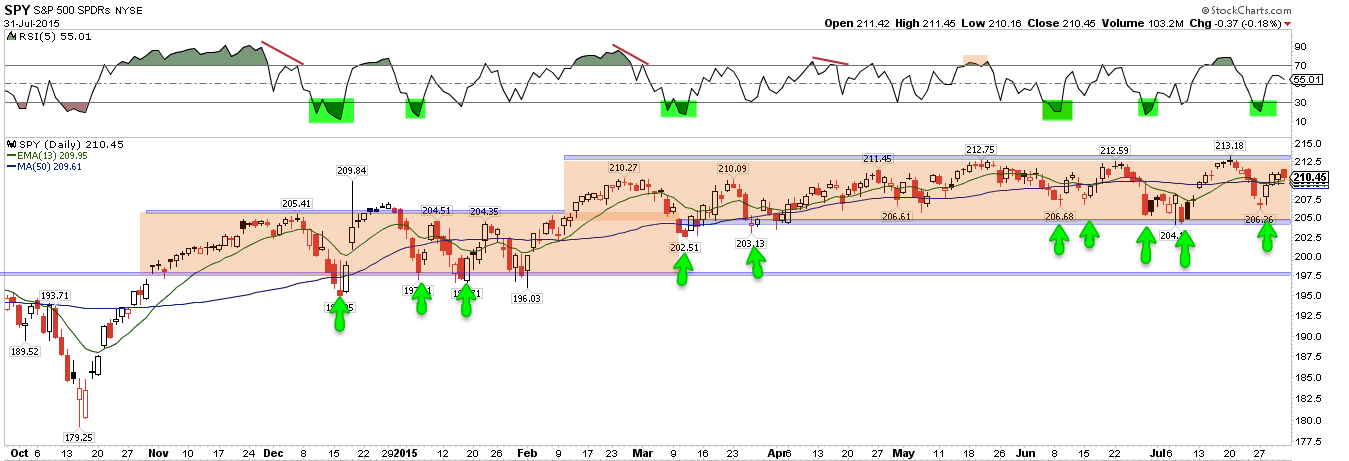

SPY ended last week in the middle of its 6-month trading range. Note that Monday's sell off pushed RSI into oversold (top panel). Every time this has happened since December, the low has soon been retested (arrows). There is little here to suggest that pattern won't continue.

Moreover, SPY did something unusual this week. There was a large gap up on July 10 that was only partially filled on Monday. When SPY leaves a gap open for a week and that gap is subsequently breached, it normally fills. That it did not suggests that price will return to 204.8, probably within a month.

In the chart above: the weekly pivot (209. 4) will be important this coming week. That is the 50-dma as well as Thursday's low from which price rebounded strongly. Holding above that level opens up a test of 211.6 and then the weekly R1 (212.5). Odds of the July 10 gap filling increase should 208 break (blue line).

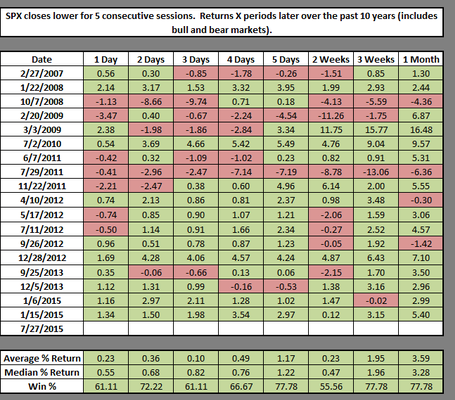

SPY closed lower 5 days in a row. Since the 2009 low, price has at least retested the low within a month 11 of 13 times (85%). In the table below, note that the last instance retested the low intraday (data from Chad Gassaway).

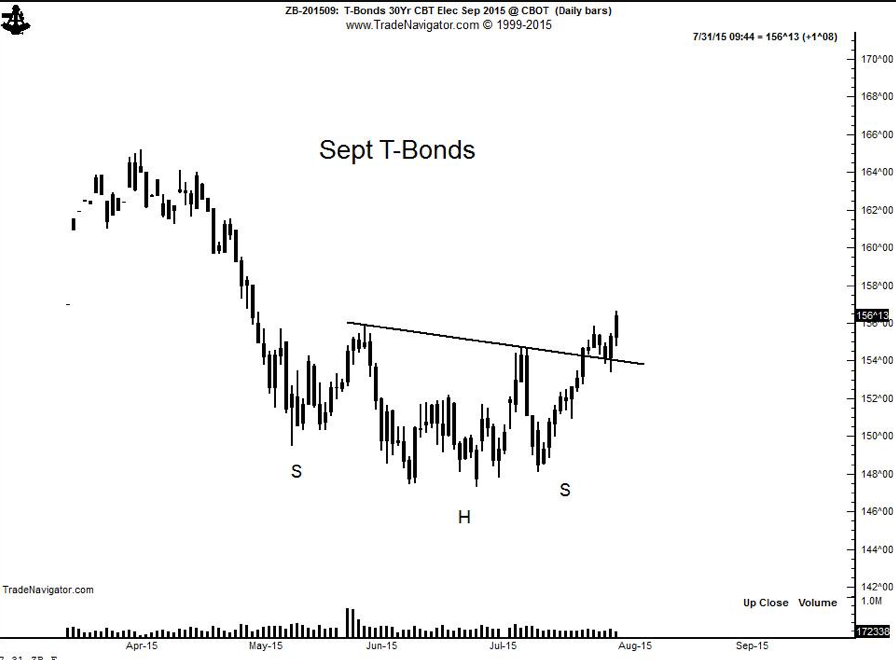

TLT strengthened further this week. It is still at the top of a rising 1-month channel but the larger down channel that has been in place in 2015 appears to have been broken this week. The high in May was $123; a rise above this level would constitute a change in trend. Further downside in equities could coincide with a breakout higher in treasuries.

Peter Brandt notes that bonds have completed a head and shoulders bottom.

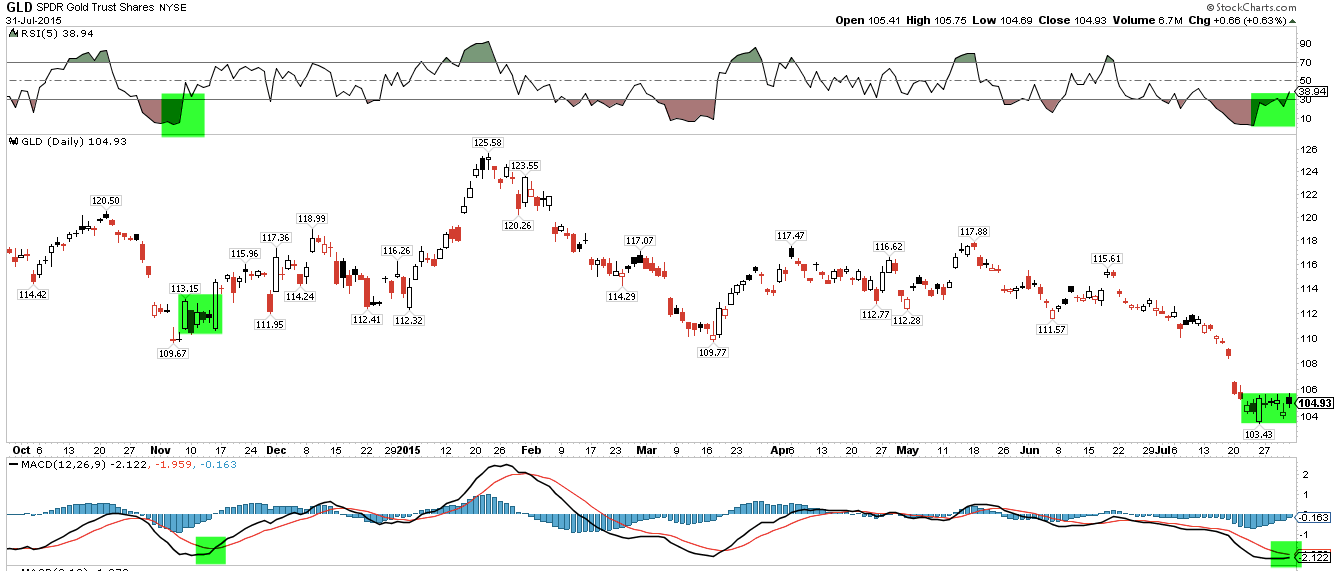

We reviewed gold more fully this week (here). Price has done little since then. Optimistically, the pattern resembles last November. A break below the recent low likely targets $100.

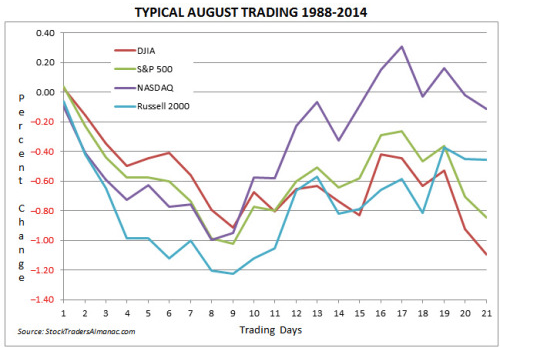

Most months start strongly. August is an exception; it is typically weak through mid-month. The entire month, recall, is typically weak, coming on the back of seasonally strong July. This year, July did not disappoint, rising 2.3% (NDX rose 4.4%; chart below from Stock Almanac).

On the calendar, July's non-farm payroll data will be released on Friday.

In summary, there are several breadth and sentiment indicators that suggest the indices have reached, or are near, a one month low. Further weakness would create a washout and a more durable low. There is, in short, a visible endgame to the sideways trading environment that has persisted in 2015.

Our weekly summary table follows.