{kind=link}

How Asset Classes Have Responded To The First Rate Hike

Courtesy of Urban Carmel, The Fat Pitch

Summary: How have different asset classes in the past responded when the FOMC has raised rates for the first time? Commodities were the best performing asset; they boomed. The dollar sold off. Equities usually rallied into the decision, then sold off, and then rallied again. Treasury yields rose. The total return for high yield bonds was usually positive.

On September 17, the FOMC will meet. And expectations are that the Fed will enact a 25bp rise in rates. This would be the first change in rates since December 2008, and the first rise in rates since June 2006 (here).

The question for investors is: how might various assets classes react? To answer, we can look at how they have reacted in the past.

Before looking at the data, consider this: a rate increase means that the economy is improving enough that employment and inflation are considered to be well on the path to being healthy. You would expect, therefore, that stocks would do well if the Fed felt comfortable raising rates. An improving economy also implies demand for commodities and lower default rates, meaning that commodity prices are rising and high yield bonds are at least stable.

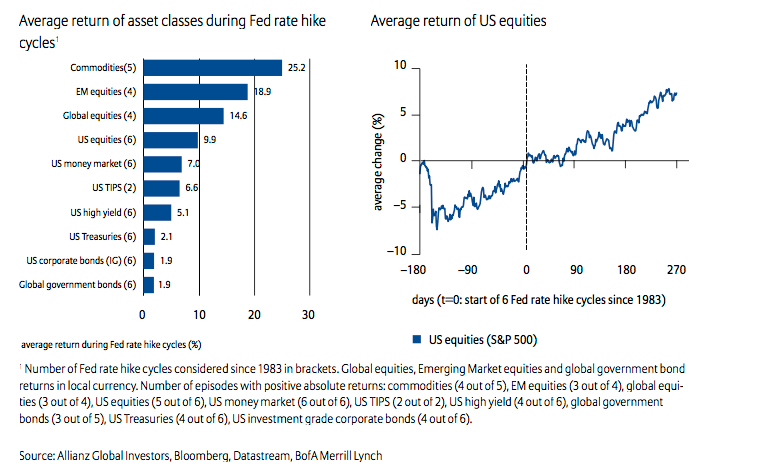

And in fact, this is what usually happens when the Fed raises rates for the first time: stocks and commodities rise and high yield bonds have a positive return over the next year (the average length of time rates rose). The chart below covers the period after the first rate hikes in 1983, 1986, 1988, 1994, 1999 and 2004 (data from Allianz).

None of these assets was a winner each time: stocks rose in 5 out of 6 cases; commodities rose in 4 of 5; ex-US equities in 3 of 4; treasuries and high yield bonds in 4 of 6.

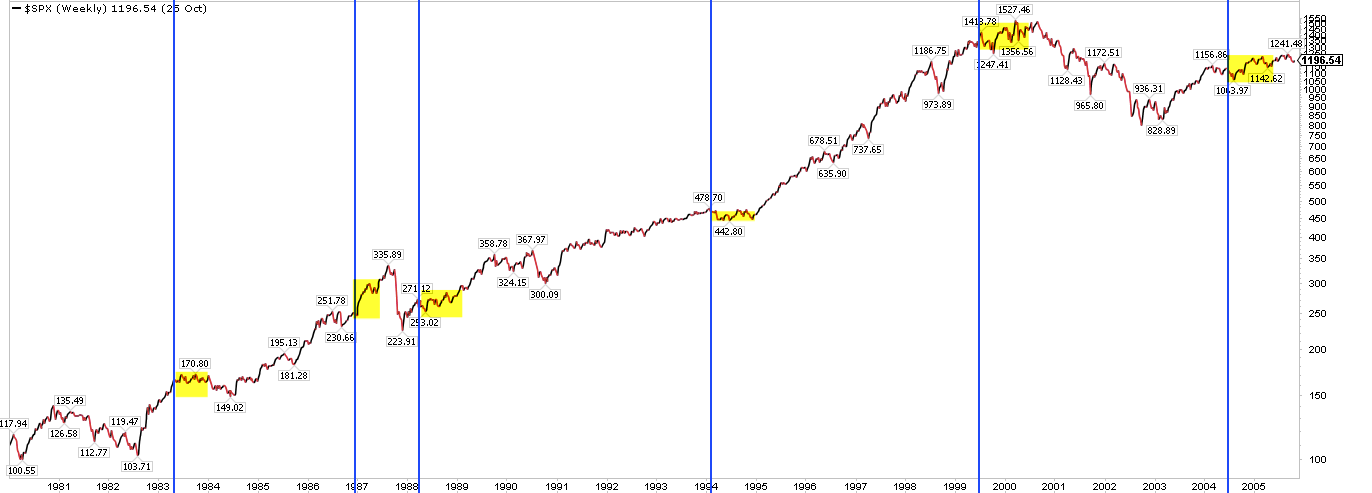

In all 6 cases, US equities rose in the 3 months ahead of the first rate hike (on the right side of the chart above). Note that $SPX sold off by at least 5% in the months after the last 4 rate hike cycles began. So, to generalize, stocks rally into the expected first rate hike, then sell off and then rally again.

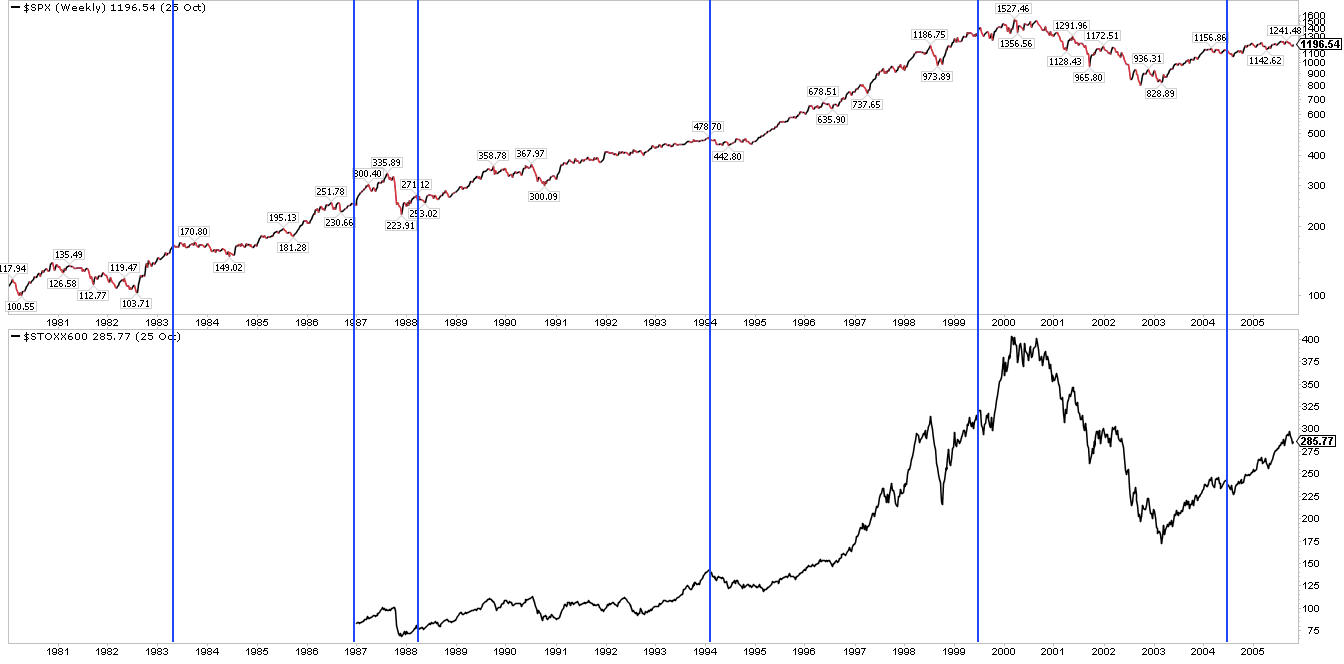

European stocks followed the same pattern as US stocks (the Stoxx index is shown in the lower panel).

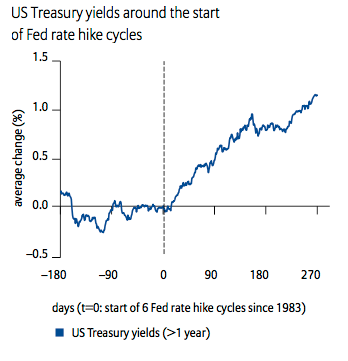

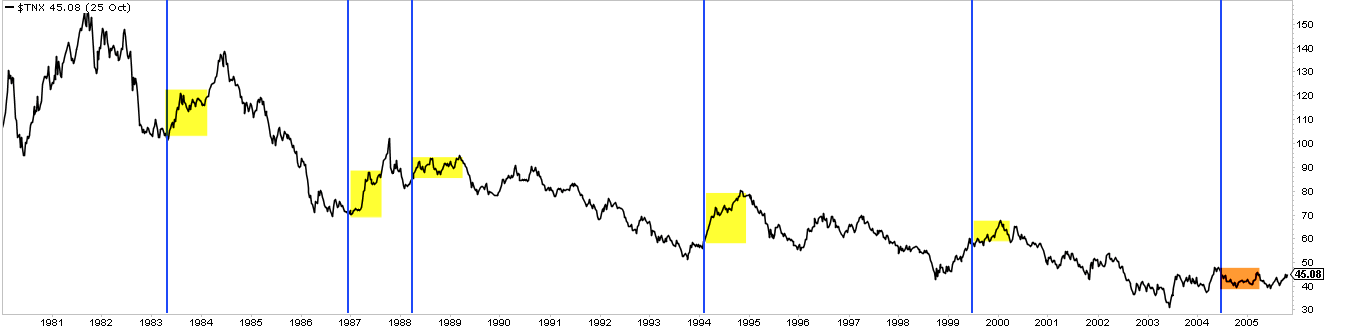

Treasury yields rose after each rate hike (meaning: prices fell). The positive returns (first chart in this post) come from their offsetting coupon payments.

Interestingly, yields were flat or rising in the 3 months ahead of the first rate increase. In contrast, 5, 10 and 30 year yields have now declined over the past 3 months, and 2 year yields are flat. The set up is different now then it has normally been.

10 year treasury yields after each rate hike shown below; not surprisingly, they mostly rise.

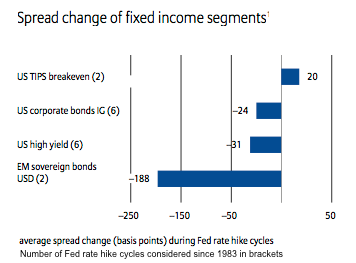

Corporate and high yield bond spreads contracted, on average, after the first rate hike.

In the case of high yield, most of the total return gains came from their yield. Again, the pattern is inconsistent, with 4 of 6 appreciating.

While both treasuries and high yield appreciated in value, it's worth noting that their returns were less than for money markets.

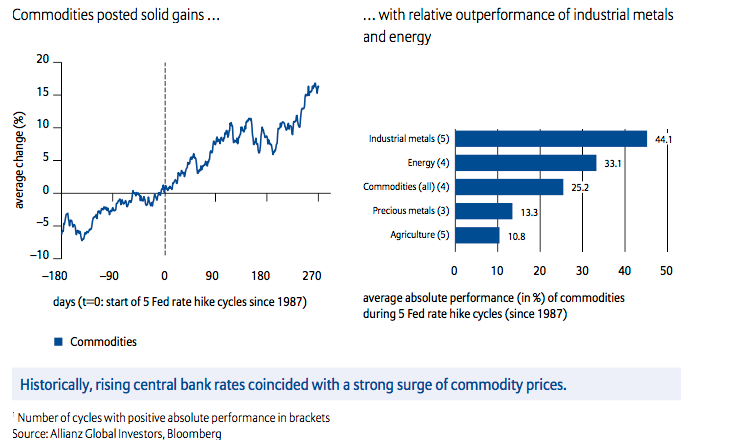

On average, commodities were the best performing asset class after the first rate hike. Again, this should make sense since an improving economy implies demand for industrial metals and energy. In fact, commodity prices had already been rising ahead of the first rate increase. Which makes today's situation, where energy and industrial metals are falling, very different.

Gains in the CRB index after the first rate hikes are shown below. Commodity optimists should note the pattern in 1999, in which commodities fell ahead of the first rate increase and then boomed.

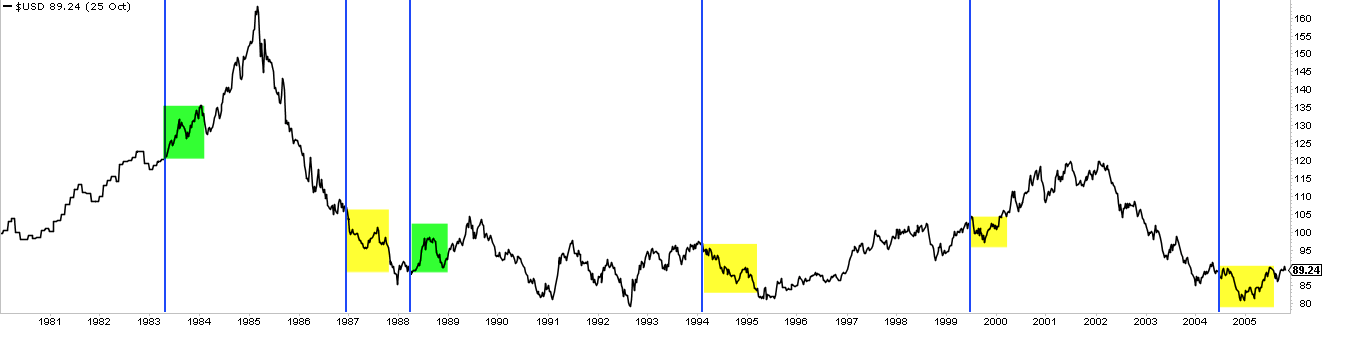

The dollar generally weakened after the first rate hike. In the last 5 cases, the one exception was 1988: the dollar was already at a low, rallied and then gave all those gains back.

The obvious caveat to this discussion is that circumstances today are quite different from previous instances during the past 30 years. We are in a post-financial crises recovery for the first time in 80 years. The European currency union and many emerging markets were still fresh the last time rates were raised more than a decade ago. Perhaps the biggest difference is this: rates normally rise within 18 months after a stock market drop or economic weakness caused them to be lowered. Now, the last time rates changed is almost 7 years ago. The US stock market is already deep into a long bull market. Things could well be very different this time.