Reminder: Sabrient is available to chat with Members, comments are found below each post.

Courtesy of Sabrient Systems and Gradient Analytics

Last week, the S&P 500 put up its best week of the year, closing above key psychological levels and breaking through bearish technical resistance, with bulls largely inspired by the dovish FOMC meeting minutes. But this year’s market has been news-driven and quite difficult for traders to read. Even our fundamentals-based and quality-oriented quant models have struggled to perform. With corporate earnings season now underway, equities might take a breather at this point of the oversold rally until some clarity from key corporate bellwethers begins to take shape, particularly with respect to forward guidance. But despite severe global headwinds, there remain strong reasons for optimism here at home.

In this weekly update, I give my view of the current market environment, offer a technical analysis of the S&P 500 chart, review our weekly fundamentals-based SectorCast rankings of the ten U.S. business sectors, and then offer up some actionable trading ideas, including a sector rotation strategy using ETFs and an enhanced version using top-ranked stocks from the top-ranked sectors.

Market overview:

Last week, the S&P 500 closed up +3.3% for the week, its best performance of the year so far. The S&P 500 large caps and Dow Jones Industrials blue chips closed above the psychological levels of 2,000 and 17,000, respectively — the first time since August — as well as above their 50-day simple moving averages. Although the Russell 2000 small cap index closed above its 50-day simple moving average, it remains more than 10% below its 52-week high set in June.

A big inspiration for bulls was the September FOMC meeting minutes that were released on Thursday afternoon showing that the Fed is concerned about persistently low inflation and the potential impact on the U.S. of the global economic slowdown. The Fed now doesn’t expect to reach its inflation goal of 2% before the end of 2018. Investors took this as a sign that the fed funds rate won’t be increased until 2016 — and likely it will be only a token one at that. The minutes also indicated that the Fed was further from approving a rate hike in September than had been broadly assumed, given the formidable global headwinds led by slowing growth in China and all of the broad implications of that, including falling demand for everything from commodities to Apple (AAPL) products.

Now we start to hear the Q3 corporate earnings reports, although investors are more interested in forward guidance than actual performance during the prior quarter. According to S&P Capital IQ, S&P 500 companies are expected to post negative revenue growth of -1.5% versus 3Q2014 (the third straight quarterly decline), primarily due to the strong dollar, and negative earnings growth of -5.3%, the first such decline since 3Q2009. However, excluding the Energy sector’s massive -66% earnings contraction, overall earnings growth for the others would be a respectable +2.7%.

No doubt, this market has been hard to read and even harder to trade. Certainly it has been news-driven to a large extent. Moreover, we have seen sort of an upside-down market lately in which the former leaders (like biotech) have been taken to the woodshed while the former laggards (like Energy and Materials) have been strong, all of which is the opposite of what our fundamentals-based and quality-oriented quant models have been suggesting (see sector rankings below). Such events are certainly not uncommon. It is largely driven by short-covering on the lower-quality stuff and profit-taking/protection on the higher-quality.

Such is the case with the dominant biotechs/biopharmas, many of which still sport low forward P/Es but have been the target of some posturing politicians in this election cycle who noticed that a populist message about drug pricing was resonating, thus creating uncertainty in the minds of investors — even though nothing concrete has changed in the company’s fundamentals. Sabrient-favorite Valeant Pharmaceuticals (VRX) is a case in point. This carnage among the money-making biotechs was the “last shoe to drop” so to speak in this broad market correction that essentially began in late-June. ConvergEx pointed out last week that among biotechs, stock performance this year has been inversely-correlated to profitability. But we believe investor rationality will soon return to this important market segment — this is definitely a case of, if you liked them at the higher valuation then you should love them at these lower valuations.

Furthermore, China’s coming clean with lowered growth estimates exacerbated worries of a global slowdown. Of course, this has not only hurt the industrial and commodity oriented firms, but also impacted Apple and its main suppliers in a major way — including favorites of ours like Skyworks Solutions (SWKS), Avago Technologies (AVGO), and NXP Semiconductor (NXPI), which are big winners that have suddenly fallen more than the overall market over the past few months, largely due to concerns about lowered growth projections in China.

Overall, Sabrient’s growth at a reasonable price (aka, GARP) approach seeks strong forward earnings projections selling at a reasonable price today, and the broadening concerns about global growth call into question whether corporate growth expectations will be met, or if they will be revised downward even further. Nevertheless, we still believe quite strongly that GARP is the way to invest profitably in most market conditions (except perhaps recessionary or irrationally exuberant ones). After all, buying future earnings flows at a reasonable price today is what investing is supposed to be about.

Yes, global headwinds are evident, and there are many commentators predicting either a recession or a bear market or both. Other than the wide-reaching impact of even a moderate slowdown in China, the strengthening dollar has been an issue given that so many things are priced in dollars, including oil, commodities, and global debt. All told, global 2015 GDP priced in dollars is forecast to contract about -3.5%, down to about $75 trillion, which certainly sounds recessionary. The last time this occurred was in 2009 when economic and stock market woes were reversed by massive stimulus programs. Many are wondering what it will take this time.

BlackRock came out with its global outlook, and the firm sees this as the most challenging global market environment in years that will likely lead to annual investment returns of just 4-5% over the next five years, as opposed to the robust 14% average of the past five years, pointing to a greater emphasis on defensive strategies and downside protection. Nevertheless, their outlook for the global economy is optimistic, and global recession is not their base case scenario.

And I believe there is reason for optimism. As I noted last week, household incomes and purchasing power are up, jobless claims are at the lowest level since 1973, auto sales are robust, global monetary policy remains accommodative (even here in the US, with the dovish implications of the FOMC minutes), banks are well-capitalized, corporate coffers are flush with cash, stock buybacks and M&A are active, and homebuilders are doing well. And perhaps most important of all, American innovation and entrepreneurism is more active and impressive than ever before.

Certainly last week’s market action was driven by the dovish FOMC minutes, and now fed funds futures (which tend to be quite prescient) are forecasting only a 37% chance of a quarter-point rate hike in December and a 47% chance January. The 10-year yield closed Friday at only 2.10%. The CBOE Market Volatility Index (VIX), a.k.a. fear gauge, closed Friday at 17.08, which is back below the 20 panic threshold.

SPY chart review:

The SPDR S&P 500 Trust (SPY) closed Friday at 201.33, which is back above its 50-day simple moving average but still below its 200-day, and the dreaded death cross remains intact (the 50-day SMA crossed down through 200-day in early September). But after some needed backing-and-filling and testing of support around 187, the prior Friday’s trading gave us a bullish engulfing candlestick, and then this past Friday provided a confirmation of the breakout back above resistance at the $200 price level and the 50-day SMA. As I said last week, the 200 price level (corresponding to 2,000 on the S&P 500) had been tested for resistance three times, and it was likely we would soon see another retest. Now that bulls have broken through to the upside, the 204 level (former support line for the long sideways consolidation from February through late-August) is the next level of tough resistance. However, oscillators RSI, MACD, and Slow Stochastic are getting a bit extended, although they could still go further to the upside. If SPY fails in this upward move and falls back below the $200 price level and its 50-day SMA, we might see another retest of support at 187, and perhaps even the August intraday low near 182 (which is also the low of last October). But in any case, as I said last week, the chart is shaping up a lot like 1998 and 2011, and I suspect the bulls will find a way to take stocks higher by year end — possibly to new highs.

Latest sector rankings:

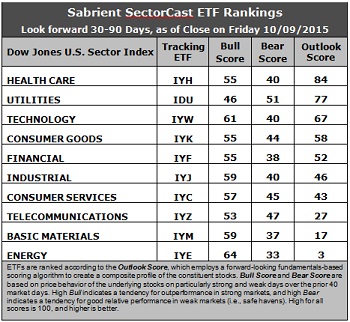

Relative sector rankings are based on our proprietary SectorCast model, which builds a composite profile of each equity ETF based on bottom-up aggregate scoring of the constituent stocks. The Outlook Score employs a forward-looking, fundamentals-based multifactor algorithm considering forward valuation, historical and projected earnings growth, the dynamics of Wall Street analysts’ consensus earnings estimates and recent revisions (up or down), quality and sustainability of reported earnings (forensic accounting), and various return ratios. It helps us predict relative performance over the next 1-3 months.

In addition, SectorCast computes a Bull Score and Bear Score for each ETF based on recent price behavior of the constituent stocks on particularly strong and weak market days. High Bull score indicates that stocks within the ETF recently have tended toward relative outperformance when the market is strong, while a high Bear score indicates that stocks within the ETF have tended to hold up relatively well (i.e., safe havens) when the market is weak.

Outlook score is forward-looking while Bull and Bear are backward-looking. As a group, these three scores can be helpful for positioning a portfolio for a given set of anticipated market conditions. Of course, each ETF holds a unique portfolio of stocks and position weights, so the sectors represented will score differently depending upon which set of ETFs is used. We use the iShares that represent the ten major U.S. business sectors: Financial (IYF), Technology (IYW), Industrial (IYJ), Healthcare (IYH), Consumer Goods (IYK), Consumer Services (IYC), Energy (IYE), Basic Materials (IYM), Telecommunications (IYZ), and Utilities (IDU). Whereas the Select Sector SPDRs only contain stocks from the S&P 500, I prefer the iShares for their larger universe and broader diversity. Fidelity also offers a group of sector ETFs with an even larger number of constituents in each.

Here are some of my observations on this week’s scores:

1. Healthcare remains in the top spot this week with an Outlook score of 84. It displays a relatively solid forward long-term growth rate and return ratios, and relatively good sentiment among Wall Street analysts (net revisions to earnings estimates). Even though the overall trend continues to be skewed toward reductions to forward estimates, a lack of cuts, even without a strong upside bias, earns a sector a good relative score. Utilities remains in second ahead of Technology with a score of 77 on the strength of the most positive sentiment (relatively speaking) among both Wall Street analysts and insiders (open market buying), as well as a reasonable forward P/E. Technology, Consumer Goods (Staples/Noncyclical), and Financial round out the top five, followed by Industrial and Consumer Services (Discretionary/Cyclical). Financial continues to display the lowest forward P/E (just over 14x).

2. Energy remains at the bottom with an Outlook score of 3 as the sector scores among the worst in all factors of the GARP model across the board. In particular, the sector still shows an increasingly negative forward long-term growth rate and low return ratios, as well as the highest forward P/E (now over 25x, after the recent rise in prices). (However, note that the refining & marketing segment remains an area of strength within the sector, with some having forward P/Es under 10x.) Basic Materials takes the other spot in the bottom two with an Outlook score of 17.

3. Looking at the Bull scores, Energy has the top score of 64, followed by Technology, while Utilities is the lowest at 46. The top-bottom spread 18 points, which reflects fairly low sector correlations on particularly strong market days, which is good. It is generally desirable in a healthy market to see low correlations reflected in a top-bottom spread of at least 20 points, which indicates that investors have clear preferences in the stocks they want to hold (rather than broad risk-on behavior).

4. Looking at the Bear scores, Utilities displays the top score of 51, which means that stocks within this sector have been the preferred safe havens (relatively speaking) on weak market days. However, this score is down substantially from 73 several weeks ago, and it continues to sink. Energy scores the lowest at 33, followed by Basic Materials and Financial, as investors flee these sectors during market weakness. The top-bottom spread is 18 points, which reflects fairly low sector correlations on particularly weak market days, which is good. Ideally, certain sectors will hold up relatively well while others are selling off (rather than broad risk-off behavior), so it is generally desirable in a healthy market to see low correlations reflected in a top-bottom spread of at least 20 points.

5. Healthcare displays the best all-around combination of Outlook/Bull/Bear scores, while Energy is the worst. Looking at just the Bull/Bear combination, Consumer Services (Discretionary/Cyclical) is the best, indicating superior relative performance (on average) in extreme market conditions (whether bullish or bearish), while Financial is the worst.

6. This week’s fundamentals-based Outlook rankings now appear to reflect a neutral look, although they continue to trend more defensive lately (after finally looking bullish a few weeks ago), with defensive sectors Utilities and Consumer Goods (Staples/Noncyclical) in the top four, along with all-weather Healthcare and economically-sensitive Technology. Notably, our Net Revisors score, which reflects the outlook among Wall Street analysts, continues to show very little in the way of positive earnings revisions, which is worrisome. In fact, only Utilities showed net positive earnings revisions this week. Keep in mind, the Outlook Rank does not include timing, momentum, or relative strength factors, but rather is a reflection of the fundamental expectations of individual stocks aggregated by sector.

Stock and ETF Ideas:

Our Sector Rotation model, which appropriately weights Outlook, Bull, and Bear scores in accordance with the overall market’s prevailing trend (bullish, neutral, or defensive), has moved back to a neutral bias and suggests holding Healthcare, Utilities, and Technology, in that order. (Note: In this model, we consider the bias to be neutral from a rules-based trend-following standpoint when SPY is between its 50-day and 200-day simple moving averages.)

Other highly-ranked ETFs in SectorCast from the Healthcare, Utilities, and Technology sectors include iShares Global Healthcare ETF (IXJ), PowerShares S&P SmallCap Utilities ETF (PSCU), and First Trust NASDAQ Technology Dividend Index (TDIV). Also scoring near the top of our ETF rankings are the US Global Jets ETF (JETS), made up mostly of airlines, with an Outlook score of 100; the PowerShares Dynamic Leisure & Entertainment Portfolio (PEJ), with a score of 99; and the First Trust LongShort Equity ETF (FTLS), with an Outlook score of 94, which employs a long/short absolute return strategy and licenses the Sabrient/Gradient Earnings Quality Rank for idea generation.

For an enhanced sector portfolio that enlists some top-ranked stocks (instead of ETFs) from within the top-ranked sectors, some long ideas from Healthcare, Utilities, and Technology sectors include United Health Group (UNH), McKesson (MCK), UIL Holdings (UIL), Atmos Energy (ATO), Adobe Systems (ADBE), and athenahealth (ATHN). All are highly ranked in the Sabrient Ratings Algorithm.

If you prefer to take a bullish bias, the Sector Rotation model suggests holding Technology, Healthcare, and Industrial, in that order. But if you prefer a defensive stance on the market, the model suggests holding Utilities, Consumer Goods (Staples/Noncyclical), and Healthcare, in that order.

IMPORTANT NOTE: I post this information each week as a free look inside some of our institutional research and as a source of some trading ideas for your own further investigation. It is not intended to be traded directly as a rules-based strategy in a real money portfolio. I am simply showing what a sector rotation model might suggest if a given portfolio was due for a rebalance, and I may or may not update the information each week. There are many ways for a client to trade such a strategy, including monthly or quarterly rebalancing, perhaps with interim adjustments to the bullish/neutral/defensive bias when warranted — but not necessarily on the days that I happen to post this weekly article. The enhanced strategy seeks higher returns by employing individual stocks (or stock options) that are also highly ranked, but this introduces greater risks and volatility. I do not track performance of the ETF and stock ideas mentioned here as a managed portfolio.

Disclosure: Author has no positions in stocks or ETFs mentioned.

Disclaimer: This newsletter is published solely for informational purposes and is not to be construed as advice or a recommendation to specific individuals. Individuals should take into account their personal financial circumstances in acting on any rankings or stock selections provided by Sabrient. Sabrient makes no representations that the techniques used in its rankings or selections will result in or guarantee profits in trading. Trading involves risk, including possible loss of principal and other losses, and past performance is no indication of future results.

{kind=link}