{kind=link}

Courtesy of Dana Lyons

The relative strength of the consumer discretionary sector versus consumer staples had been a positive for stocks – not anymore.

The relative strength of the consumer discretionary sector versus consumer staples had been a positive for stocks – not anymore.

Some folks like to accuse us of being perma-bears, or at least one-sided when presenting market insights. Nothing could be further from the truth. Our only mission is to make and protect our clients’ assets. Therefore, our focus will go wherever the data leads us. It just so happens that the preponderance of data over the past 8 months, in our view, has been tilted to the bearish, or “risk” side of the equation.

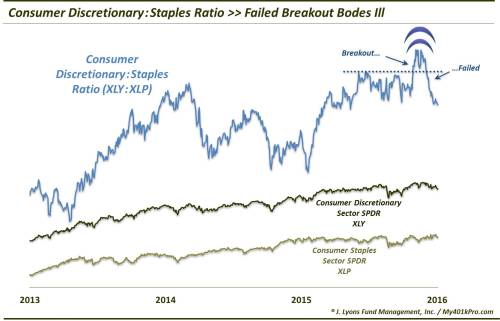

That said, we have been willing suppliers of bullish indicators when we’ve come across them. Since May, these have primarily been found in shorter time-frame data points. One longer-term positive that has persisted, however, is the relative ratio between the consumer discretionary sector versus the consumer staples sector.

The story goes that, when discretionary stocks are leading, it is perhaps an indication of a healthy consumer in the economy, and/or that the investor community is comfortable taking on risk. Conversely, when the defensive staples sector is leading the way, it connotes the impression that investors, and possibly consumers, are assuming a “risk-off” posture.

Whether that is sound reasoning or not, prices do historically support the theory. When stocks are in the midst of a bull market, the discretionary:staples ratio tends to slope up. On the other hand, during risk-off periods (e.g., 2000, 2007-2008), the ratio has clearly pointed lower.

Over the past year, the ratio, as measured by the Consumer Discretionary SPDR ETF (XLY) versus the Consumer Staples SPDR (XLP) has exhibited mostly positive behavior. This has, in our view, been a positive consideration for stocks over that period. We pointed out such bullish developments in posts in May and December.

Although, in the December post, we did point out a very relevant asterisk regarding the ratio. The XLY was climbing on the backs of only a few mega-cap names (e.g., Amazon). Indeed, using the equal-weighted versions of the two sectors, we found discretionary stocks at a relative 4-year low. That said, as recently as November, the XLY:XLP ratio was breaking out to all-time highs. On the margin, we considered that a bullish factor for stocks. Not anymore.

As the chart below shows, the November breakout in the XLY:XLP ratio was short-lived. It has since dropped to an 8-month low in forming an apparent false breakout.

So is this a death knell for the bull market? Not necessarily. There are obviously numerous other factors that will weigh on the market’s direction at least as heavy as this one. However, for a bull market with a dwindling list of positives on which to hang its horns, this additional negative development is most unwelcomed indeed.

There are precious few support rungs left to lose before this market finally goes Kerplunk!

* * *

More from Dana Lyons, JLFMI and My401kPro.