{kind=link}

Record highs!

Record highs!

That's what the Banksters want to print in their monthly reports to get their customers to pull their CASH!!! off the sidelines and put them into something that generates fees for the bank. They don't give a crap whether you win or lose – as long as they get their fees.

Morgan Stanley says "this time will be different" and that we shouldn't worry about Central Bank de-leveraging or China's Credit Collapse because (and these are their points, not me just making it sound absurd), although "global growth will moderate somewhat, and will remain above trend." That would be great but the "trend" has been around 2% and global stocks are not priced for "above 2% growth" they are priced for 4% growth or 6% growth and we are miles away from that!

Goldman's Chief Equity Strategist, David Kostin says the company's HNW clients are "confused" by the lack of inflation (as that's what we expect in a great economy) and he ponts back to the disparity of measurement that we touched on last week.

Goldman's Chief Equity Strategist, David Kostin says the company's HNW clients are "confused" by the lack of inflation (as that's what we expect in a great economy) and he ponts back to the disparity of measurement that we touched on last week.

Like me, Kostin is recommending inflation hedges, urging his clients to ignore what the Fed is saying and pay attention to the evidence that's right in front of their eyes. Zero Hedge does a very good job pointing out what's wrong with inflation measures as they note that: "A leading driver of disinflation has been the Video, Audio, and Computer category where prices dropped by 5% in 2015, by 10% in 2016, are declining at an average pace of 7% YTD." This is one of the stupidest things the Government does when measuring inflation. Basically, if you bought an IPhone last year for $1,000 and it had 64Gb or Ram and this year you spend $1,200 but it has 128Gb of ram, the Government says you are getting more for your money so that phone is counted as 40% CHEAPER than the one you bought last year.

Of course it's a bit more complicated than that but processor speed per Dollar goes up too so yes, electronics are almost always a drag on inflation, as are appliances. So take this chart with a Lot's wife-sized grain of salt:

In reality, rents are completely out of control – up 30% in the past five years and accelerating into 2017:

These are all-time highs yet real estate sales remain anemic, with most of the properties being snapped up by REITs, who now own 357,000 multi-family housing units that 111M Americans now live in – also a record. Essentially, about 10% (30M) Americans lost their homes in the crash, never recovered and are now renters, paying record-high rates, which makes it even harder for them to get back on their feet.

This matters a lot because it then affects Owner's Equivalent Rent (OER), which makes up 24.433% of the CPI and higher rents are calculated as a benefit to homeowners (2/3 of the population) while a detriment to renters but, since the owners outweight the renters, the higher POTENTIAL rental income for their homes is considered beneficial and artifically lowers the CPI. 24.433% – that is complete BS and that's why the CPI has no real connection with reality.

Why does the Government do this, because CPI is connected to Cost of Living Adjustments so a higher CPI means they have to admit that Seniors need more Social Security or that Union Workers deserve raises and nobody wants that, do they? So they lie to us and they've lied to us for so long we don't even remember that their used to be a truth.

Logic is another thing that's gone out the window these days and our friends at Morgan Stanley would like us to believe that we shouldn't worry about the fact that the Central Reserve Banks, over the course of the next 2 years, are projected to go from injecting over $100Bn a month into the markets to REMOVING $100Bn a month unitl they pull back their $10 TRILLION in purchases (8 years). What, us worry? Of course not!

Logic is another thing that's gone out the window these days and our friends at Morgan Stanley would like us to believe that we shouldn't worry about the fact that the Central Reserve Banks, over the course of the next 2 years, are projected to go from injecting over $100Bn a month into the markets to REMOVING $100Bn a month unitl they pull back their $10 TRILLION in purchases (8 years). What, us worry? Of course not!

As long as the cessation of stimulus doesn't bother us and then the reversal of stimulus doesn't bother us and then nothing bad happens for the next 8 years then sure, why not pay 25 times earnings for the average S&P stock? After all, what could possibly go wrong?

JP Morgan's Quant Strategist, Marko Kolanovic, feels the market is a a "tipping point" and he noted last week:

"In what is akin to the law of ‘communicating vessels,’ once inflows in bonds stop, funds are likely to start leaving other risky assets as well, including equities. The FOMC statement yesterday alleviated immediate fears – normalization of balance sheet will start ‘relatively soon,’ but only if ‘the economy evolves broadly as anticipated.’ This reasonably dovish stance pushes this market risk out for a few weeks (the next ECB meeting is Sep 7th, Fed Sep 20th, BoJ Sep 21st). This gives volatility sellers and other levered investors a limited window to position for a seasonal pickup in volatility and central bank catalysts in September."

Taking into account the solid equity fundamentals, but increased risks that are building for September – we suggest investors hedge their long equity exposure. One can take advantage of two current extremes in the derivatives market: a record low level of option volatility, and nearly record high level of option ‘skew’ (relative price of out-of-the-money options). An equity hedge that incorporates these extremes is “1 by 2 put spreads.” Investors can buy one S&P 500 2450 strike put and sell two 2300 strike put options that expire in January 2018 at nearly no cost (~20bps cost). This gives protection if the market drops below ~2450 (but also commits investor to double down below ~2150).

Howard Marks has a "Bubble Check-List" and we, at PSW, have our SQQQ and TZA hedges, as well as a few other plays that benefit us if the market ever does decide to turn down for more than a few hours. Over the weekend, in yet another note from JPM, this time from the bank's "flow" expert, Nikolaos Panigirtzoglou, he writes that none of the above should come as a surprise and that as a result, investors – both institutional and retail – have started putting hedges against an equity crash.

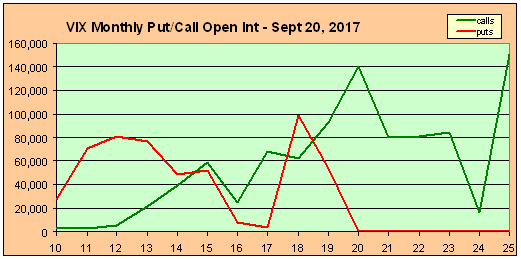

Among the market feature he highlights is that the current put to call open interest ratio for S&P500 index options has been rising for most of this year, and that while this ratio had peaked in June and its current level is not extremely high, it nevertheless stands above its post 2014 average. What is more extreme, is the call to put open interest ratio for VIX options, which at almost 4.0, is close to historical highs. (Chart courtesy of Sentiment Signals – http://sentimentsignals.blogspot.com/2017/07/heisenburgs-uncertainty.html)

Among the market feature he highlights is that the current put to call open interest ratio for S&P500 index options has been rising for most of this year, and that while this ratio had peaked in June and its current level is not extremely high, it nevertheless stands above its post 2014 average. What is more extreme, is the call to put open interest ratio for VIX options, which at almost 4.0, is close to historical highs. (Chart courtesy of Sentiment Signals – http://sentimentsignals.blogspot.com/2017/07/heisenburgs-uncertainty.html)

Notice on the chart that, into last week, all the Sept VIX puts disapeared and a massive amount of calls were written. At the same time, there have been several articles aimed at chasing retail investors out of VIX longs, presumably so the funds could free up shares and load up ahead of their expected correction (see our discussion in Member Chat).

It's going to be a meaningless Monday, we're just going to sit back and see how the month ends up but we'll certainly short the S&P again if we're back to 2,480 – along with the other shorting lines we were using last week.

I'm on TV this morning, live from the Nasdaq (#TradeTalks) and our weekly webinar will be tomorrow at noon, not 1pm and not Wednesday!

Be careful out there and have a good week,

– Phil