{kind=link}

It's one long Sunday for me as I just flew in from California.

It's one long Sunday for me as I just flew in from California.

I left at 10pm, didn't sleep on the plane and now it's 8am and I find myself essentially continuing what I was saying last Monday (14th), when we flatlined at 2,965 after a very bad Friday sell-off. This Friday was not as bad, with the S&P finishing at 2,986 and we're still flirting with 3,000 – again. So it's the same old, same old with not much having changed over the weekend so earnings will be our primary focus for the week.

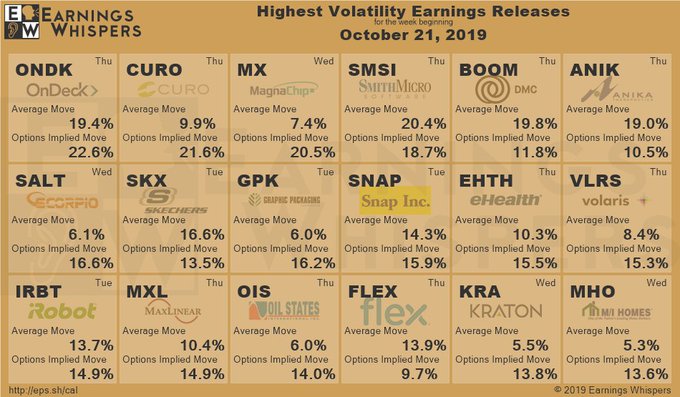

Lots of fun reports already and, so far, earnings have beaten low expectations, for the most part and we're into the meat of the S&P 500, with about 1/4 of the index reporting this week:

We'll keep an eye on the Tech Sector as the earnings there have been pretty erratic. Semiconductors rose 6.74% in Q3, topping all six industries in Tech. Semis are followed by Technology Hardware (+5.26%) in second place and IT Services (-3.19%) at a distant third. The worst Tech Sector Performer has been Software, whose quarterly return stands at a negative 16.3% but still many companies to report.

In June, Goldman Sachs issued a warning to “write off high-growth tech stocks,” according to a CNBC report – this was not heeded by the market as the Nasdaq is up about 800 points (10%) since June. The reasons for Goldman’s warning are double: they said that Technology stocks may be overvalued at their current levels, and that talks about potential regulatory changes from Washington may make stocks within the sector something of a “hazard.”

Keep in mind it's not about justifying the 10% move up from 7,200 (thowing out the spike) in the June dip but justifying the ENTIRE 60% move from 5,000 in the beginning of 2017 to 8,000 today. We ran an analysis of the top Nasdaq stocks back on April 17th, looking at whether or not the Nasdaq could justify 8,000 and we thought it could – and that was our bullish premise at the time but we cashed out at the 8,000 line and now, the question for Q3 is – can they justify 9,000 and, if not – why would we still be in them?

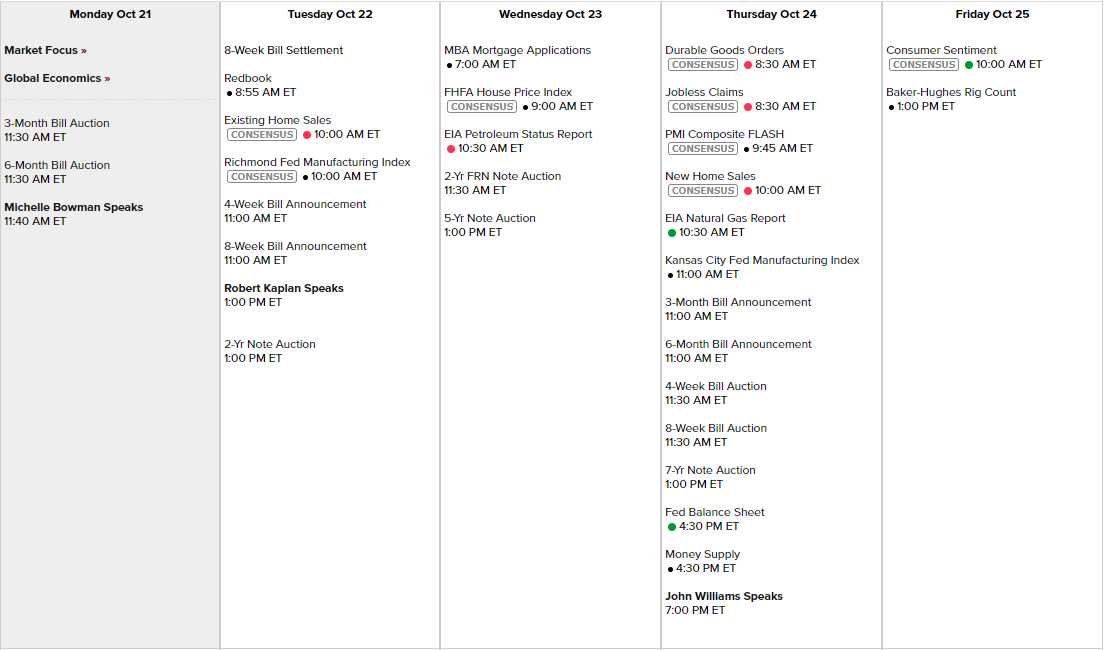

Outside of earnings reports, we have only 3 Fed speakers this week and not very much exiting data to distract us from earnings reports. Richmond Fed is tomorrow, Durable Goods, PMI and the KC Fed on Thursday and Consumer Sentiment Friday but, other than that – it's all about who made what last Q and, of course – guidance!

Apple got an upgrade this morning and is being used to prop up the markets – so take any gains with a grain of salt. An AAPL rally is often used to cover up a broader sell-off as we top out and, of course, it's Monday – you can't take anything that happens on low-volume Mondays seriously.