{kind=link}

Courtesy of ZeroHedge

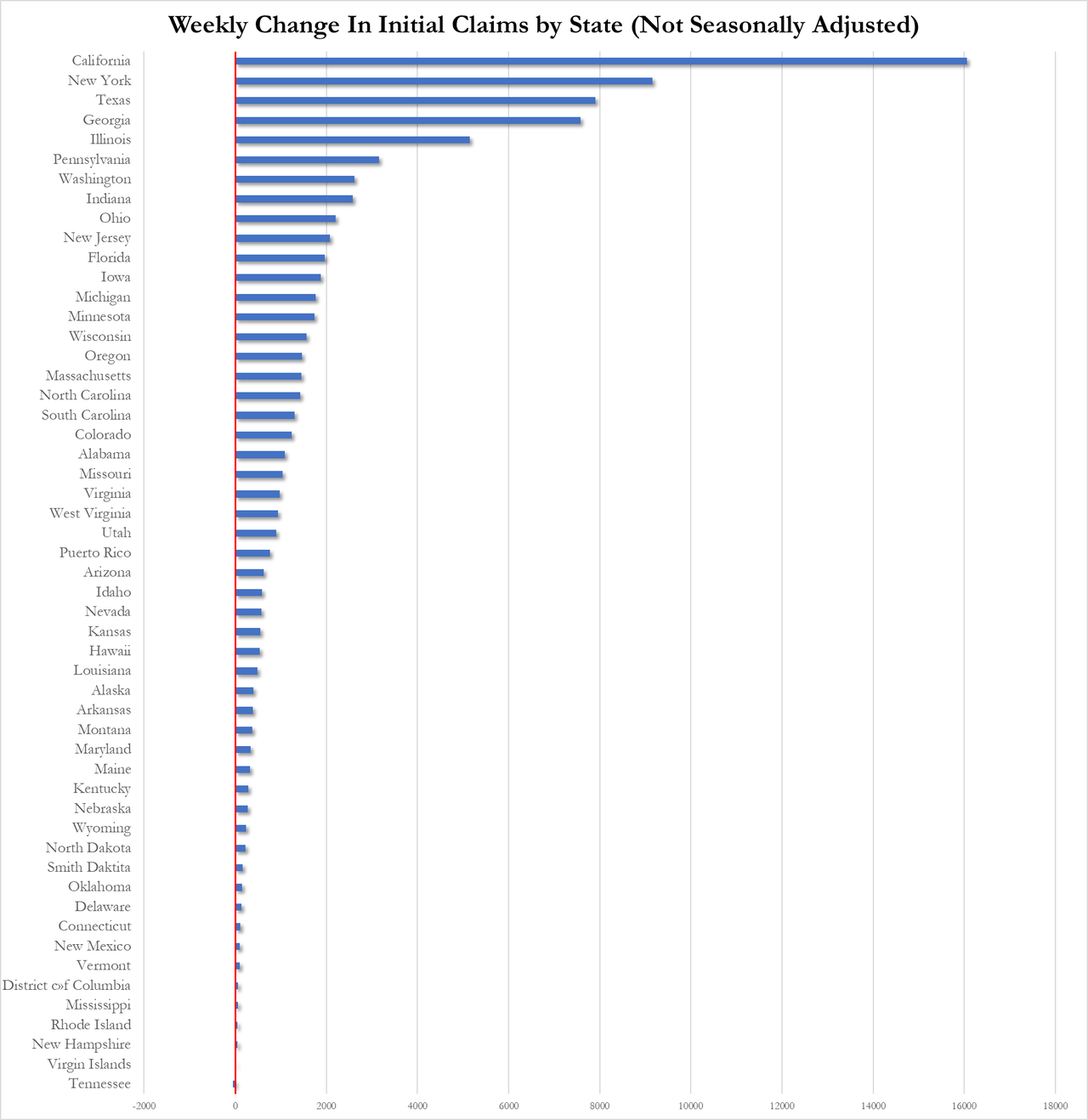

Another relatively quiet day for macro news but enough to spook some traders as continuing claims data jumped to 10-month highs, with every single state seeing a rise (something that hasn’t happened since the peak of the COVID lockdowns).

Additionally, as Bloomberg notes, claims data are pointing to a recession as continuing claims are above their one-year low by a margin that has always preceded a slump. But initial claims are also on the threshold of signaling a recession as the percentage of US states with their initial claims worsening significantly is rising fast, i.e. the slowdown is becoming pervasive.

Source: Bloomberg

As Simon White pointed out, this measure is like a Geiger counter for recessions. It also captures the precipitate nature of their onset. Economies do not go smoothly from a non-recessionary to a recessionary state, they do so abruptly. In the chart above, once the percentage of states with rising claims goes through 20%, it often goes to 50%, and then a recession is, historically speaking, all but guaranteed.

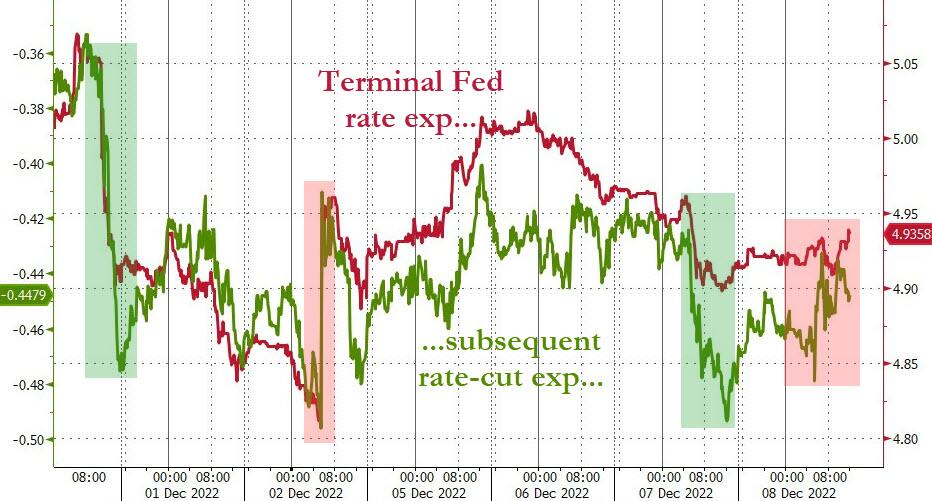

Something stocks are definitely not anticipating… stocks made some gains on the day (despite dropping on MSFT/ATVI headlines), and interestingly, bond yields were higher on the day (not exactly a sign of growth fears) even though the curve flattened (inverted deeper), and Fed rate-trajectory expectations shifted modestly more hawkish (not what you’d expect amid recession anxiety)…

Source: Bloomberg

Treasury yields rose across the curve today with the belly underperforming (5Y +9bps, 30Y +2bps). The entire curve remains lower in yield since Powell’s speech [sic],

Source: Bloomberg

Which flattened the yield curve deeper into inversion territory (recessionary signals growing)…

Source: Bloomberg

All of the US major equity markets closed higher on the day with Nasdaq outperforming. Stocks dumped at the cash open but were immediately ramped higher into the EU Close. They fell again into 1430ET (margin call time) before rallying in the last hour… and fading in the last 20 mins. The S&P 500 closed higher for the first time in six days…

The dollar drifted lower for the second day in a row (but is still up on the week)…

Source: Bloomberg

Bitcoin jumped back above $17,000…

Source: Bloomberg

There was one asset-class that ‘behaved’ in accordance with the recession-threatening jobs data – crude crashed despite ripping higher early on after the Keystone pipeline was shutdown due to a leak (halting flows up to 600,000 b/d)…

Gold ramped back above $1800 overnight and clung to that level for the rest of the day…

Finally, Bloomberg notes that concerns over a global recession may be rekindling haven demand, with gold starting to rise against crude oil, which has stalled on the possibility that demand will weaken as economies waver.

The gold-to-crude ratio could favor bullion in 2023, particularly if the global economy continues to deteriorate and central banks ditch campaigns to tighten monetary policy, Mike McGlone, a senior macro strategist at Bloomberg Intelligence, said in a note Wednesday.