{kind=link}

Courtesy of ZeroHedge

Just a few short hours ago, Bloomberg reported that UBS and Credit Suisse were both against any merger scenario.

Citing sources close to the matter, Bloomberg said UBS would prefer to focus on its own wealth-centric standalone strategy and is reluctant to take on risks related to Credit Suisse.

Well since then things haven’t gone so well.

First, at least four major banks including Societe Generale and Deutsche Bank have placed restrictions on their trades involving Credit Suisse or its securities, Reuters reports, citing five unidentified people with direct knowledge of the matter.

Another source at a major global bank, who deals directly with Credit Suisse in Asia, said their bank had started asking the Swiss lender to gross settle, a trading scenario where the counterparty demands upfront payment from Credit Suisse instead of collecting later any money the Swiss lender might owe them as a result of the trade.

Another global bank has reduced its unsecured exposure to Credit Suisse, which includes all lending with no collateral, according to a person with knowledge of the matter. The bank is still providing repurchase agreements, which is secured lending.

This likely explains why the classic counterparty-risk hedge (1Y CDS) has barely budged despite the $50 billion liquidity injection from the SNB…

And second, given the continued collapse in Credit Suisse shares today (despite the billions from the SNB… and maybe even more from the ECB)…

…it appears a deal between the two Swiss banks could be on.

The Financial Times reports that, according to multiple people briefed on the talks, UBS is in discussions to take over all or part of Credit Suisse, with the boards of Switzerland’s two biggest lenders set to meet separately over the weekend to consider Europe’s most consequential banking combination since the financial crisis

The Swiss National Bank and regulator Finma are orchestrating the talks in an attempt to shore up confidence in the country’s banking sector.

Swiss regulators told their US and UK counterparts on Friday evening that merging the two banks was their “plan A” to arrest a collapse in confidence in Credit Suisse, a person familiar with those discussions told the FT.

UBS has a market value of $65bn (CHF60bn), while shares in Credit Suisse closed on Friday with a value of $8bn (CHF7.4bn).

Will this be bank mega-merger weekend?

* * *

As we detailed earlier, we knew this was the endgame more than two weeks ago when we reported that “Credit Suisse Crashes To All Time Low After Boosting Deposit Rates To Reverse Bank Run” in which we reported that after a quarter of “staggering” bank runs, the second largest Swiss bank – clearly panicking – was offering a 6.5% annual rate on new three-month deposits of $5 million or above – and a rate as high as 7% for one-year deposits – far above matched maturity Bills, and suggesting that to attract a client, the bank is forced to eat a loss.

The hope, we explained, “was that after it attracts enough new clients, the bank will then be able to quietly lower the rates and make the new accounts profitable, however as the various DeFi blow ups of 2022 showed, it never quite works out that way.”

This time was no different, and as the bank run accelerated, the Swiss bank ended up getting an (interim) $50 billion rescue financing from the SNB to cover the most recent deposit run, and it will get much more before it’s all said and done. To underscore this point, two days ago – in our post summarizing the SNB bailout – we said that “this is a last-ditch liquidity infusion, and all it does is prevent forced asset liquidations (a la SVB). Meanwhile it does nothing to halt the depositor flight because once confidence is gone, it rarely returns.“

Again we were right, and one day after the failed bailout attempt, Bloomberg writes that while the $54 billion lifeline won by Credit Suisse on Thursday gives it a fighting chance to rebuild its business, “some clients aren’t waiting around to find out how that goes.” To wit:

- In Asia, several ultra-wealthy clients continued to cut back their exposure amid the tumult this week.

- In the Middle East, some customers asked the bank to convert cash deposits into treasury bills and bonds.

- An executive at a rival European bank said they’re seeing some deposits shifting from Credit Suisse, although the amount isn’t yet sizable.

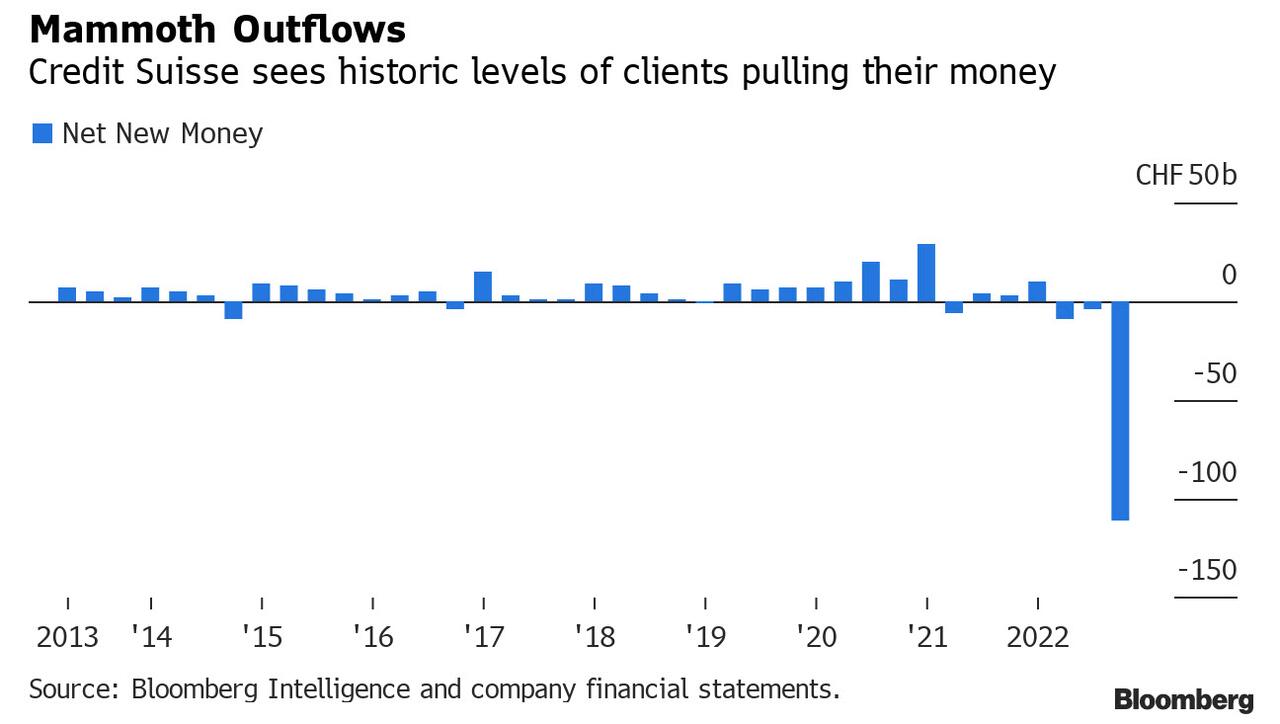

Such attrition, Bloomberg notes redundantly, “will make the overhaul that Chief Executive Officer Ulrich Koerner and his team are overseeing that much harder.” Because, at its heart, a successful bailout of Credit Suisse means halting the record historic run. Recall, the bank saw net outflows hit 110.5 billion francs ($119 billion) in the fourth quarter…

… and despite this week’s rescue, the bank run is once again picking up, setting up the bank for another bailout because unless the SNB and the Swiss government want a historic bank implosion on their hands, they now have no choice but to keep throwing good money after bad.

For the CEO, hope still lives: “We want to get back all what we lost,” Koerner said at an investor conference on Tuesday. “And once we are there, we go beyond and grow the business again.”

The problem is getting “there.” And while the bank has consistently said it has sufficient liquidity, “it isn’t yet clear what the overall flows are or whether the backstop is helping attract clients back.” Actually, it’s clear it is not, which begs the question: if an SNB rescue isn’t enough, what else can the bank do to restore confidence?

Not much: bankers are calling round clients to reassure them, primed with talking points sent out by executives or communicated at town halls. The lender is offering deposit rates that are significantly higher than rivals to win back funds, and even that is not working.

And as Bloomberg reports today, “some ultra-wealthy families booking out of Asia accelerated their retreat from the Swiss bank this week, according to three large single family offices that collectively manage billions and multiple private bankers based across Hong Kong and Singapore.”

One family office in the region is planning to cut back as much as 30% of its money parked with the embattled bank after the wealth manager was unable to assure it that non-Swiss clients would be protected in the event of a collapse, Bloomberg reports citing an unnamed person.

Some clients in the Middle East asked the bank to convert their cash deposits into fixed income securities, giving them more comfort to keep money with the firm, according to another person familiar with the matter. In Germany, a wealth manager received inquiries from Credit Suisse clients looking to shift deposits to his firm

To be sure, some clients are still optimistic:

Others are less concerned, with one adviser to several trusts saying he’s recommended they keep their deposits at Credit Suisse even though they far exceed the amounts covered by the country’s deposit insurance. He said he’s convinced there’s no risk because the Swiss government will never let the firm fail.

Then again, SVB’s corporate clients were also optimistic the bank would never fail…. until it did.

The bottom line for CS: “outflows haven’t reversed as of this month, though they have stabilized at much lower levels, according to the bank’s annual report released Tuesday, the same day Koerner said on Bloomberg Television that the bank had seen inflows on Monday.”

A day later, his bank’s shares plunged after its biggest shareholder ruled out adding to its stake, unnerving investors already on edge after three regional US banks failed in a span of days. It’s not like the bank won’t lie to restore confidence. Last month Reuters reported that Switzerland’s financial regulator is reviewing comments by Credit Suisse Chairman Axel Lehmann made in December on outflows from the company having “stabilized”, on the basis that they may have been misleading. In other words, the bank’s highest official was lying on the record, just to slow down the bank run.

The support of Credit Suisse’s counterparties will also be critical, and here too cracks are emerging: the biggest banks in the US have been paring down their direct exposure to Credit Suisse for months as it stumbled from one crisis to the next. Firms including JPMorgan, Bank of America and Citigroup have told regulators their exposures are now minimal. And then, earlier this week, Paris-based BNP Paribas also moved to trim its exposure telling clients that it will no longer accept so-called novations where BNP is asked to step in on derivatives contracts where Credit Suisse is a counterparty, Bloomberg reported.

And with every passing day, doubts grow. JPMorgan. analyst Kian Abouhossein wrote in a note (available to pro subscribers) that the “status quo is no longer an option,” laying out three possible scenarios for Credit Suisse and saying that a takeover is the most likely. However, shortly after Bloomberg reported that “both lenders are opposed to a forced combination.”

Any such move could be followed by a listing or spinoff of the Swiss unit. Other possibilities mooted in the note included the Swiss National Bank stepping in with a full deposit guarantee or Credit Suisse’s entire investment bank being shuttered.

While executives insist such drastic solutions aren’t needed now the backstop is in place, they are dead wrong since the deposit run is once again picking up. Meanwhile, the bank is claiming that its strategic revamp announced in October remains the core plan to turn around the bank, they say, with the bank’s offer to buy back debt underlining its core strength.

“We see it as preventive liquidity so that we can carry out the transformation of Credit Suisse and continue to work well in this turbulent situation,” Swiss bank head Andre Helfenstein said in an interview with national broadcaster SRF on Thursday.

It adds up to a finely balanced situation. With camera crews gathering Thursday outside of Credit Suisse’s stone-clad headquarters on Zurich’s moneyed Paradeplatz, CEO Koerner urged staff to stay focused.

“Effective communication is key to ensure that our clients and external stakeholders understand the strengths of the bank, our strategy and the accelerated progress we are making to create the new Credit Suisse,” he said in a memo.

So far the only thing the bank has communicated clearly is that it has no clear vision of how it will emerge from the current crisis while preserving depositor confidence.