{kind=link}

By Ye Xie, Bloomberg Markets Live reporter and strategist, as posted at ZeroHedge

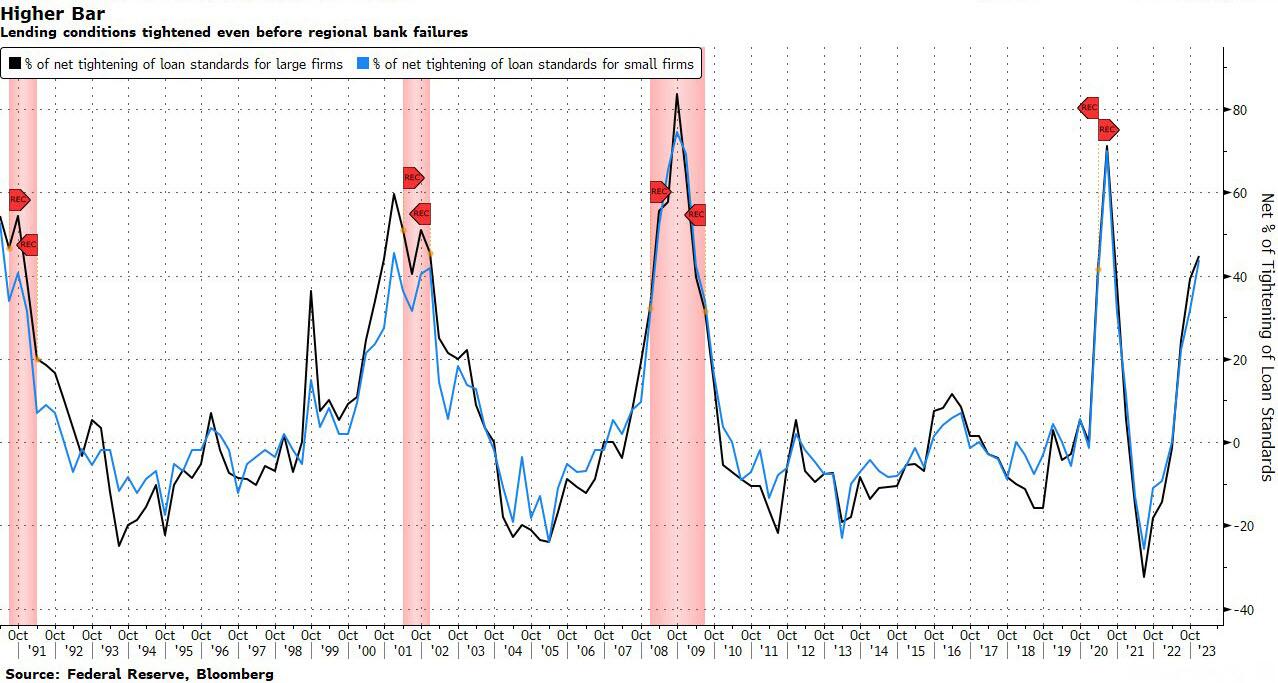

While the US banking turmoil has eased lately, the economic damage from an inevitable tightening in lending may only be starting.

In China, the opposite seems to be happening. The latest central bank survey shows that credit demand surged to the highest in more than a decade. That lending boom, though, may overstate the recovery in business and consumer confidence.

On Monday, the US ISM manufacturing index slumped to the lowest level since May 2020. It may be one of the earliest signs of the knock-on effect from bank failures last month. While the deposit outflows at small banks seem to be stabilizing, the underlying issue is far from being resolved. The yield advantage of money-market funds is likely to force banks to raise rates to compete for deposits. The resulting higher funding costs could cap banks’ willingness and capacity to lend.

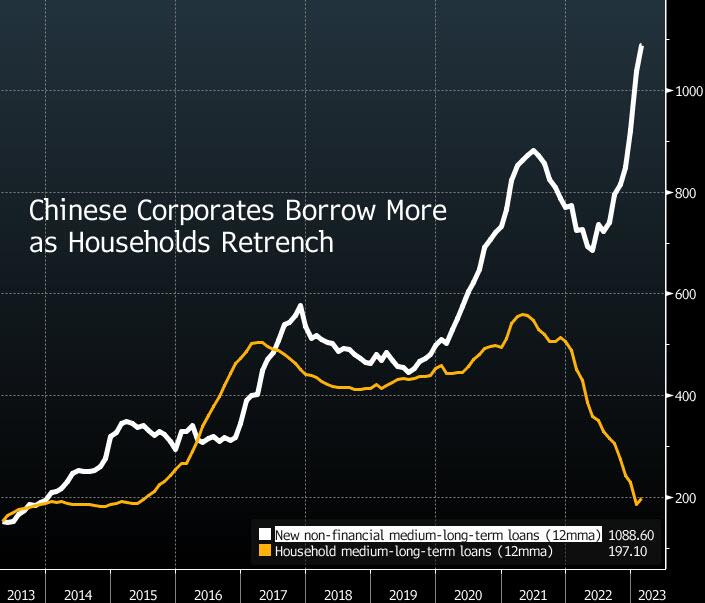

In China, a different dynamic is on display. The PBOC’s quarterly survey of bankers released Monday showed loan demand surged to the highest in 11 years.

The survey result is in-line with the actual bank lending data, which show long-term corporate loans are shooting through the roof, thanks to lower borrowing costs. It is in sharp contrast with the deleveraging in the household sector amid housing turmoil.

At first glance, strong long-term borrowing seems to suggest a resurgence of business confidence as entrepreneurs expand factories or invest in new businesses.

But the central bank’s surveys of businesses and households cast doubt on this interpretation. The macroeconomic heat index of entrepreneurs only recovered in the first quarter to a level seen a year ago, with domestic and export orders showing only marginal improvement. The profitability index actually fell to the lowest level since March 2020. On the household side, the survey also shows a modest recovery in consumer confidence.

All in all, business and consumer confidence seems to be on the mend, but it’s far from a full recovery. That suggests at least part of the demand for corporate debt may be companies borrowing new money to refinance existing debt, as opposed to expanding their business.