{kind=link}

Least Bad

-

Audio Recording by George Hahn

For decades, America has predicted — arrogantly and repeatedly — the imminent fall of a nation. The doomed nation, according to Americans? A: America.

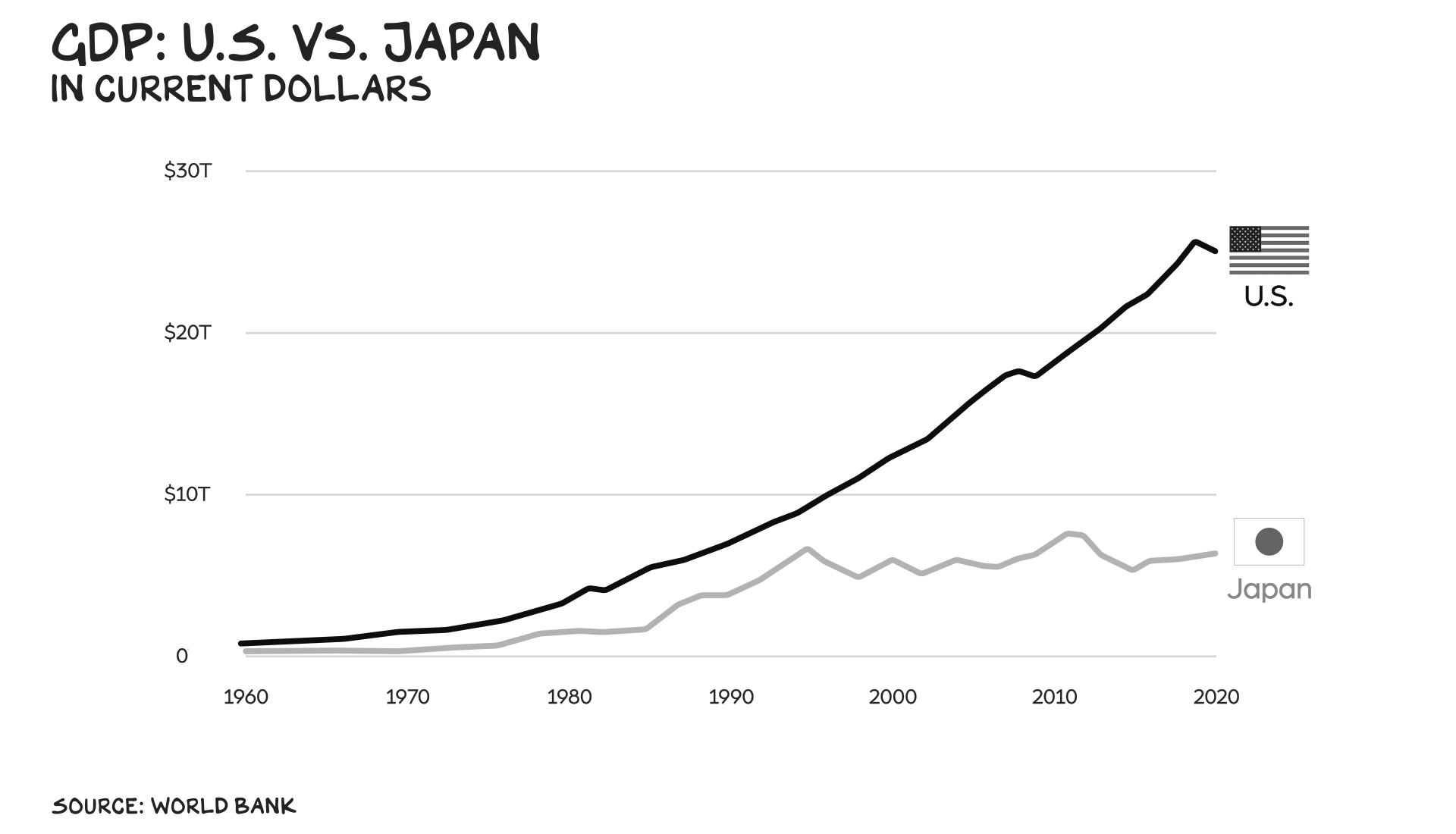

In the ’80s, we decided Japan was doing to us economically what they couldn’t do militarily four decades prior. My second year in business school (Berkeley ’92) was devoted to a forensic analysis of our loss to Japan. Computers and cars were the future, and Japan was building them faster, better, and cheaper. In 1984, Walter Mondale asked Reagan at the presidential debates, “What do we want our kids to do? Sweep up around the Japanese computers?” Three years later, Paul Kennedy wrote a book about it, The Rise and Fall of the Great Powers, comparing the U.S. empire to the British empire. Japan’s GDP soared to 40% of ours, and we feared what might happen when that number hit 100. It never did.

In the early aughts, our soft tissue was geopolitical. The tragedy of 9/11 was described as an “inevitable outcome.” Our subsequent invasion of Afghanistan inspired books including Dark Ages America: The Final Phase of Empire, and Are We Rome? The Fall of an Empire and the Fate of America. Each offered a similar theme: Our time was running out.

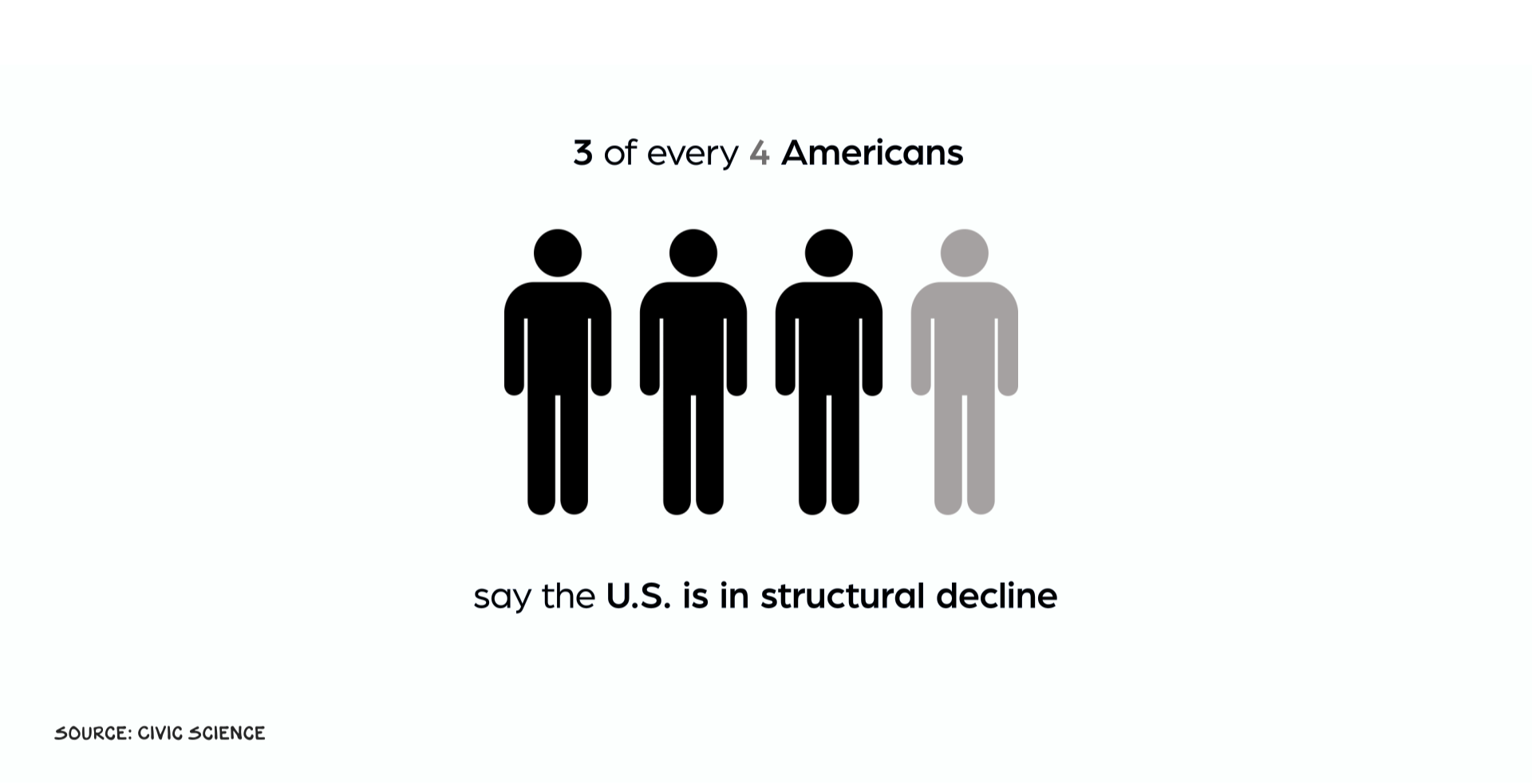

Today the decline is (supposedly) more imminent. January 6 was the “beginning of the end.” Russia’s invasion revealed a “great unwinding.” Nations view us “with pity,” and we are “on the brink of collapse.” Just last week, the New York Times opinion page compared us to Rome (again). These headlines are click bait, and we still take the bait: Three-quarters of Americans believe our country is in structural decline, and the song of the summer is an ode to our demise.

It’s not just the public. Among economists there’s a growing school of thought that our situation is dire. Two months ago, ratings agency Fitch downgraded America’s credit rating due to “fiscal deterioration” and “erosion of governance.” The debt ceiling debacle didn’t help: Investors “should worry.” Our debt-to-GDP ratio is hovering around 120%; back when it was 70%, Brookings called it “the real national security threat.”

Many believe we are in the midst of “dedollarization,” ceding our status as the world’s reserve currency because of our unsustainable spending habits and an overall loss of faith globally. JPMorgan recently flagged it, an ex-CIA adviser plainly predicted it, and one prominent tech investor bet $1 million on it. Ray Dalio, the founder of the world’s largest hedge fund, hinges his recent bestseller, Principles for Dealing with the Changing World Order, on America’s inability to adapt to our loss of status and power. Empires win and lose their hegemony depending on their reserve currency status, and in Ray’s view, we’re near freefall.

We’re Not

Culturally you could build a compelling case. National pride is at an all-time low, and the “vibe” in America is that things are not good. (See above: the song.) But these are functions of perception, and as I’ve written before, human perception is flawed.

This is an economic discussion. And when you look at the data, you’ll find every diagnosis of our supposedly terminal illness is proof the doctor is jonesing for us to die. We’ll examine them, but first, a brief summary of the doomer’s economic vision for America. It goes roughly as follows:

1) America keeps borrowing more money, leading to an increased burden of interest payments.

2) Foreign nations increasingly question our ability to make good on our debts, leading to low demand for U.S. Treasuries and thus low demand for dollars.

3) Once dedollarization takes effect and the dollar is supplanted as the world’s reserve currency, the U.S. will be forced to ratchet up Treasury yields to increase demand for our debt, leading to even greater interest payments.

4) This will crowd out private investment, as well as public investment in our own infrastructure. GDP growth will grind to a halt, and eventually we’ll default on our debt.

5) At that point we’ll be unable to borrow or finance our growth, and

6) America will collapse.

Dedollarized

Doomsday is due next century or next year, depending on who you ask. (That ex-CIA adviser said it’d be last month.) But the catalysts are consistent, and one of them is this notion of dedollarization.

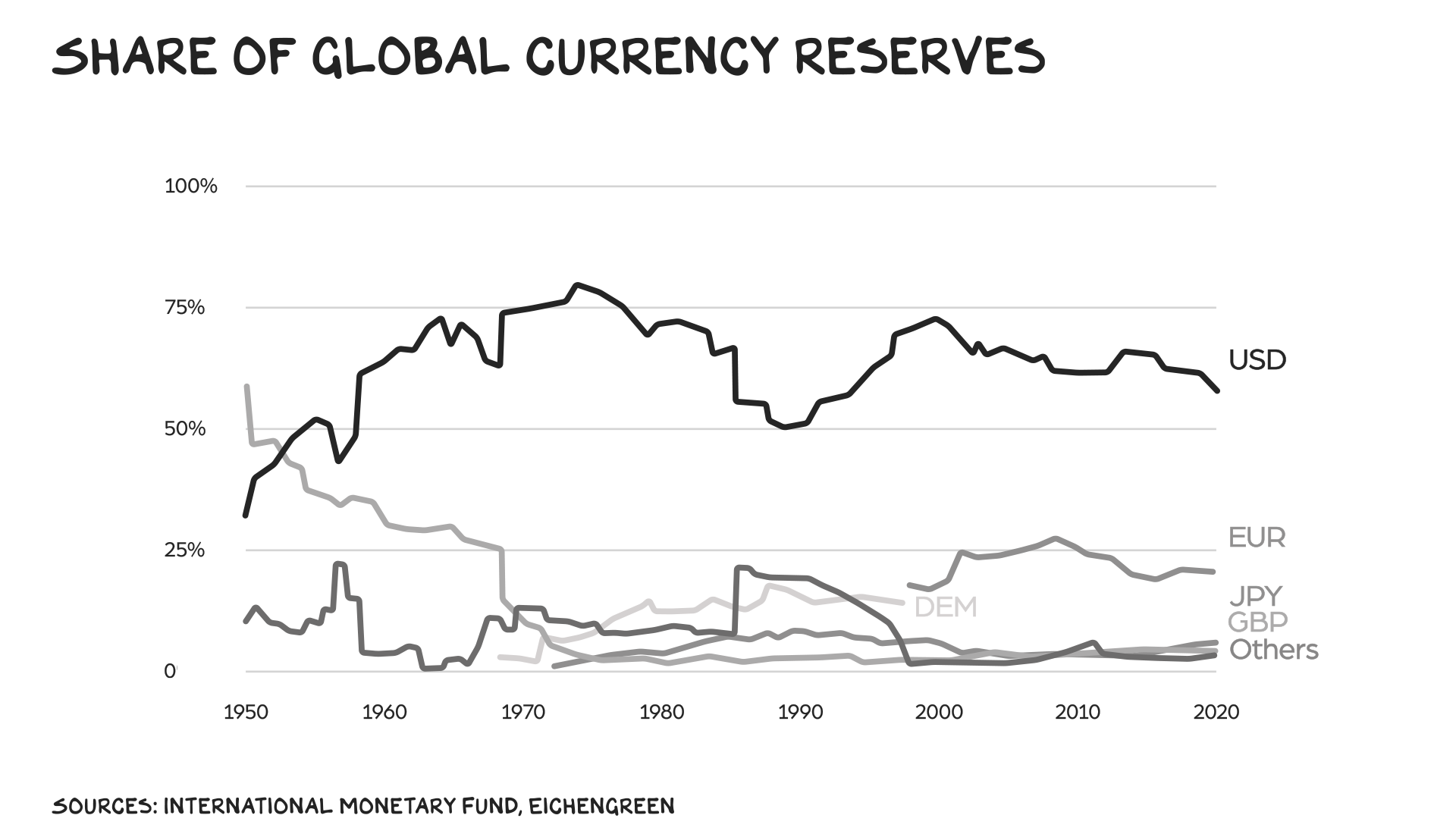

The argument is that foreign central banks are losing interest in the dollar. The stat dedollarists point to is that the dollar has fallen from 70% share of the world’s currency reserves to 60% in the past 20 years. That may sound significant, but the scope is comically small. When you zoom out you find that in the ’80s our share was 50%, and 30 years before it was 40%. The only accurate description of the dollar’s reserve status over the past 75 years is … unwaveringly dominant. At 20%, the next-best option (the euro) is not within striking distance.

However, it’s not the euro dedollarists are talking about, but the currencies of ascendant nations, including China. A common headline is “Yuan’s share of global reserves hits record high.” Less common is any mention of that “high”: 2.6%. The president of Brazil made headlines recently calling on the BRICS nations (Brazil, Russia, India, China, South Africa) to join forces to create a new global reserve currency. The world’s reaction was lackluster — and even South Africa’s own central bank governor played it down: “If you want it, you’ll have to get a banking union, you’ll have to get a fiscal union, you’ve got to get macroeconomic convergence.” Translation: pipe dream.

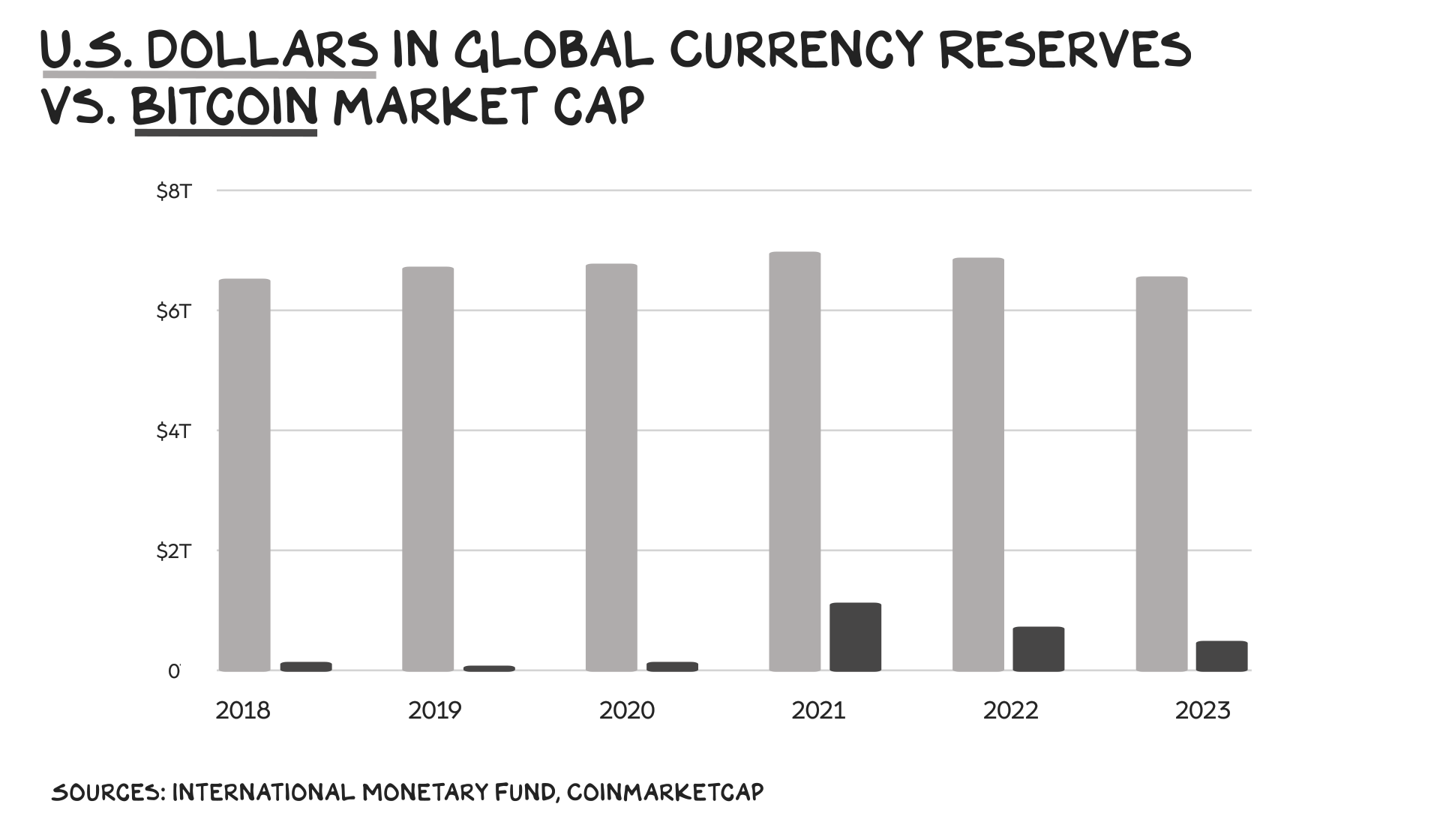

Another pipe the hallucinations flow through is bitcoin. Among its many use cases is its potential to supplant the dollar. The argument: The value of the dollar is predicated on faith in the U.S. government; the value of bitcoin is predicated on faith in, well, bitcoin. Many bitcoin bulls argued the latter will ultimately win — and for a second there in 2021, it looked feasible. As with every other dollar competitor, though, the cryptocurrency ran out of steam. Today the total value of bitcoin is 12 times smaller than the amount of dollars held in global central bank reserves. So next time someone tells you the dollar will be replaced, ask: With what? By any metric, the most innovative payment platform or store of value has been, and remains, USD. More good news: Minting dollars doesn’t require the energy consumption of Argentina. But I digress.

Theory of Relativity

Arguments for America’s decline are rarely accompanied by a credible alternative. This is true of the dollar, and it’s also true of U.S. debt.

Take Fitch’s downgrade of our national credit rating, for example. What should have been a seismic shock to the global bond market by the premier ratings agency turned out to be a catastrophist headline. The bond market barely registered the news, with the 10-year Treasury yield inching up 4 basis points. Goldman put it deftly: “We do not believe there are any meaningful holders of Treasury securities who will be forced to sell due to a downgrade.” Jamie Dimon put it better: The downgrade was “ridiculous.”

As with currencies, creditworthiness is relative. The question creditors should ask isn’t “how likely am I to get my money back,” it’s “who’s more likely to give me my money back?” And when it comes to sovereign debt, there is no better option than the United States. Sure, Xi Jinping may make Biden look like a web browser with 19 tabs open, not knowing where the music is coming from — but the Chinese Communist Party also systematically withholds, suspends, and lies about the nation’s economic data. The Party has even ordered its own economists to stop talking about negative trends. Who would you rather lend to?

False Prophets

This extends beyond national debt. There are several linchpin data points declinists point to that are supposed to forecast our imminent undoing, but the people who cite them also forget to compare those metrics to those of other nations.

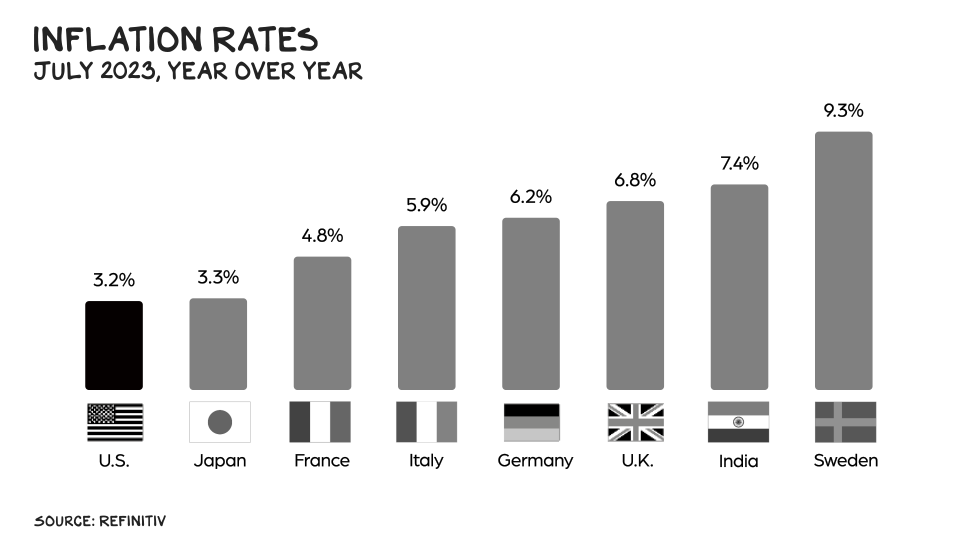

For example: inflation. Last year, inflation hit a 40-year high. Some predicted America would enter a period of hyperinflation. However, when you compare our situation to those of other nations, it’s less bad. Significantly less bad. In the U.S., prices have risen 3.2% year over year. In the U.K., it’s 6.8% — more than double. In the eurozone, it’s 5.3%. And yet — despite U.S. inflation continuing to come down and wage growth recently surpassing it — 74% of Americans still believe inflation is headed in the wrong direction.

Another catastrophist go-to: the debt-to-GDP ratio. Currently, our national debt amounts to 120% of our GDP. In other words, we’re borrowing more money than we’re making. Sounds bad. Until you look at other nations and realize it’s, wait for it, less bad. Singapore is at 130%, Italy, at 150%, and Japan, at 260%.

For years, economists have been drawing red lines around “no-go” debt-to-GDP numbers, but time has shown these red lines are also meaningless. The Maastricht Treaty said don’t go higher than 60%. The World Bank, 77%. One landmark Harvard study, “Growth in a Time of Debt,” claimed 90% was the tipping point. That study caused panic until three years later researchers found the data was faulty and the conclusion wrong. The reality is there is no magic number. Japan is at 260% and Botswana, 20%. Would you rather hold Japanese yen or Botswanan pula?

Vitals

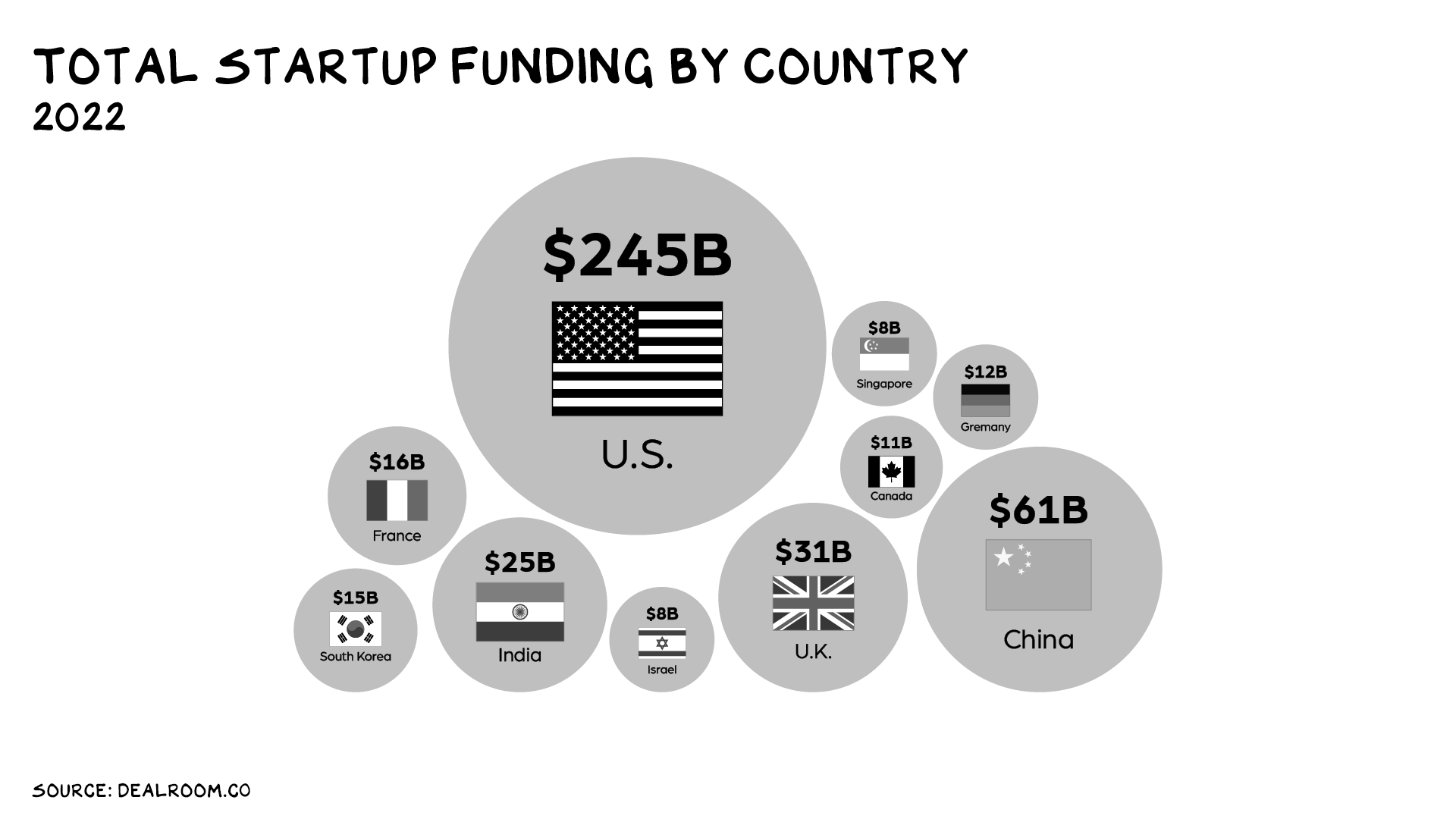

By nearly every measure, America is doing just fine. Better than fine. Our annual GDP is $26 trillion — 40% greater than China’s, whose population is four times larger. And, despite our enormous output, our economy is still growing, with 2.4% GDP growth last quarter. China’s is higher, but slowing faster than expected. Meanwhile the yuan continues to slide and this week hit a 16-year low. We have many unique advantages, including unrivaled innovation, the best universities, the best military, strong rule of law, a willingness to embrace risk, and a culture of doing the right thing (I believe this). Last year, U.S. startups received $245 billion in venture funding — roughly equal to the rest of the world combined.

Upstream in the public markets, we remain dominant. Nine of the ten largest companies in the world are domained in America. Nvidia, the undisputed leader in AI, the next world-changing technology, is headquartered in Santa Clara. Investors have reaped the benefits, and continue to wager their money on America. In the past decade the U.S. stock market has returned 10% per year. Compare that to Europe (2%) or China (0.09%) or Australia (-0.2%).

Meanwhile, our near-term economic prospects look good. Unemployment is hovering at record lows. Inflation has fallen precipitously and is low relative to our peers (see above). Poverty rates are in decline. Disposable income is higher than any other country. We have a lot to be proud of.

Exceptionalism

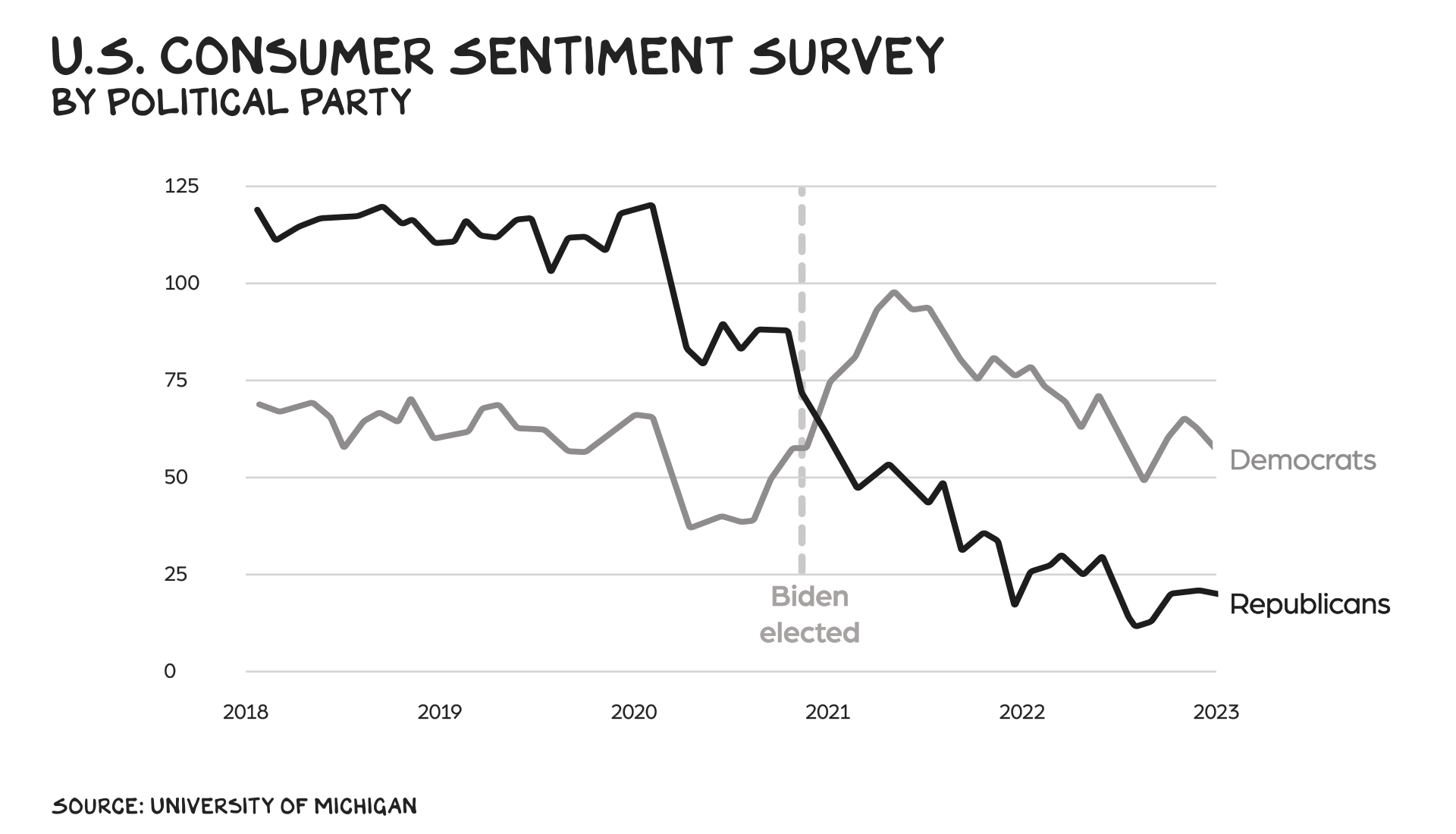

The schadenfreude we feel for our own country when it stumbles is nothing new. In fact, I would argue that in a democracy this is a feature not a bug. Things appear brighter when our favored political party is at the helm, and vice versa when it isn’t. A case in point is the consumer sentiment index, which is supposed to be an economic barometer, but is really a political one. In 2019 Republicans felt great about the economy, Democrats less so. Then Biden got elected and the relationship flipped.

People will argue I’m optimistic because a Democrat’s in charge. I recognize my political bias and intentionally adjust for it. And still, when I look at the U.S. economy and America’s position as a global power, I repeatedly land on a singular conclusion: The glass is half-full.

This conclusion won’t sell books nor grow this newsletter — history has proven that “Things Marginally Better Today” does not get clicks. But it’s the truth. And the truth, as with most things in life, is usually not as good or bad as we’d hoped. We are the least bad of our kind. When I look at the data, much less my personal situation, I can’t help but hate my life less and less every day.

If you are healthy, have someone who loves you, and enjoy a household income greater than $34,000, then you are in the top 1% globally. Think about this — you are 1 in 100. Why? Yes, you’re talented and hardworking. But more than that, you’re talented and hardworking in what is the most innovative platform in history: America.

Life is so rich,

![]()

P.S. I’m an AI optimist. Join my free event on Sep. 20, where I’ll share how AI will transform healthcare, education, and finance, and create more jobs than it takes away. Sign up here.