{kind=link}

Western sanctions haven’t curbed Russian oil profits, but the green energy transition could

By Carole Nakhle, University of Surrey

Western sanctions that put a price cap on Russian oil exports from December 2022 aimed to cause the country significant economic pain after its invasion of Ukraine last year. The idea was to curtail the amount Russia makes from its oil while ensuring it continues to flow into the global market to reduce price pressures on consumers around the world.

Back then, oil prices were trading around US$80 (£66) per barrel (/bbl). More than 10 months later, the opposite has happened: Russian exports have declined but its revenues have increased, providing it with significant funds to continue the war.

This is because since July 2023, oil prices have been above US$80/bbl, exceeding US$95/bbl at times – levels last seen in November 2022. Even though it was subject to a price cap, Russian oil has been in even greater demand due to a squeeze on supply in global oil markets.

Russia’s global oil market position doesn’t seem to be threatened by sanctions and caps. But domestic problems and market changes that have been brewing long before the war in Ukraine could affect Russia’s oil industry for a long time to come.

Oil prices rising again:

How does the price cap work?

The price cap restricts the sale of Russian oil to third parties such as China and India. Countries can still buy that oil but they must use services such as shipping and insurance provided by G7, EU and Australian entities, and can also only do so if the oil is sold below a certain price. This price was set at US$60/bbl (after December 5 2022) for oil and around US$100/bbl (after February 5 2023) for refined products such as diesel.

Western providers of insurance and maritime services make up around 90% of the market, leaving those that want to buy Russian oil with few alternatives but to respect the cap constraints.

A US Treasury report published in May 2023 claimed that the price cap achieved its goals. It reported a decline in Russian oil revenues, even though the country exported around 5-10% more crude oil in April 2023 compared to March 2022.

Russian oil was also trading at a significant discount compared to global oil prices, as Western countries had hoped when they created the price cap. By June 2023, Russia’s oil export revenues plunged to US$11.8 billion, nearly half the levels of a year before.

But by the end of August 2023, a switch had occurred. Russian oil export revenues recovered to US$17 billion even as exports hit an 11-month low, averaging 5.27 million barrels a day (Mb/d) in September 2023 – the lowest since September 2022, and 0.65 Mb/d below pre-Ukraine war levels.

Similarly, the country’s oil production in August 2023 dropped to 10.43 Mb/d in August 2023 compared to 11 Mb/d in December 2022.

Several factors have helped the Kremlin replenish its oil coffers even though it’s selling less oil. First, oil prices increased significantly over the summer of 2023. This was largely a result of production cuts announced by OPEC members, primarily Saudi Arabia and its allies, led by Russia in what is known as OPEC+.

With less oil around, cheaper Russian oil appeals to many buyers around the world, particularly in Asia. Russia has been able to use this to replace eroding European demand.

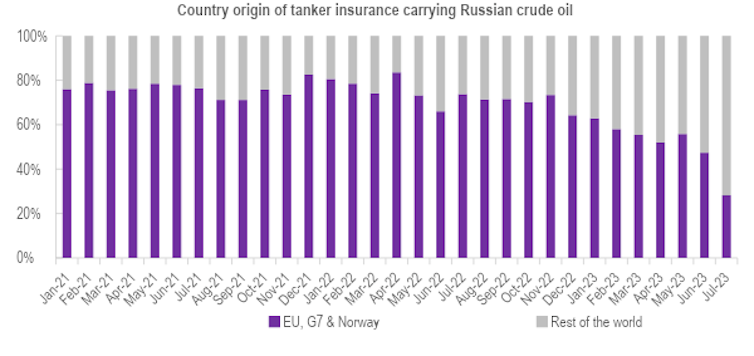

Breaches of the cap have also been reported, particularly since July 2023. Russia has significantly decreased its reliance on western maritime and insurance services, reducing the portion of its oil trade subject to the cap.

Almost three-quarters of all seaborne Russian crude flows travelled without western insurance in August, reported to be up from about 50% in spring.

Trouble brewing

Long before the war in Ukraine started, several studies – including research published by the Russian government – highlighted the challenges facing the country’s oil industry.

Russia’s Energy Strategy 2035 (published in 2019) presented two main scenarios for the country’s oil production. The optimistic scenario sees oil production for 2024-2035 at only 0.77% above 2018 production levels. In its pessimistic scenario, Russia’s oil output slips into a 12% decline by 2035 compared to 2018 levels.

An even more pessimistic scenario was suggested by a French research institute called Institut Francais du Petrole (IFP) in 2019, which said Russian oil would shrink by 41% in 2040 compared to 2018 levels.

The flight of western capital, investment and technologies from Russia following its invasion of Ukraine will only worsen all of these scenarios. But the main driver behind such outlooks is the reduction in output from brownfields (projects that have been operating for some time) in Western Siberia – the Soviet-era heartland of Russian oil production.

Alternative supplies are in remote areas (such as the Arctic circle), making them more complex and costly to develop.

Furthermore, as the transition to lower-carbon energy sources accelerates, oil demand is bound to hit a peak. The International Energy Agency expects this to happen before the end of this decade. Notable uncertainty surrounds such an outlook, but in a shrinking market the axe will fall on high-cost producers first.

New Russian oil fields developed in 2019 break even (including taxes) at an average of US$40-50/bbl. This is on the higher end, particularly compared to producers in the Middle East, where costs can even be less than US$10/bbl for some fields in Saudi Arabia, for example.

Of course, the carbon intensity of a country’s oil production will also have a significant impact on producers. As the world attempts to transition to lower carbon forms of energy, buyers will want to reduce the carbon footprint of their energy imports. Russia’s carbon intensity is double that of Saudi Arabia.

While the price cap has done little to erode Russia’s power in the global oil markets, it’s only a matter of time before its oil sector’s legacy problems and high carbon intensity start to squeeze its oil riches. This is likely to have a much more sustained negative impact on Russia’s oil wealth.![]()

Carole Nakhle, Energy Economist, University of Surrey

This article is republished from The Conversation under a Creative Commons license. Read the original article.