Friday is a National Holiday!

Friday is a National Holiday!

That’s right, it’s my Birthday and everybody gets a day off, except perhaps Chairman Powell, who seems to be giving a speech at 11:30 for some reason. Also, the Econoday Calendar seems to list reports to be released Friday that other calendars do not so I’ll check in in the morning but my family is in town so I won’t be working.

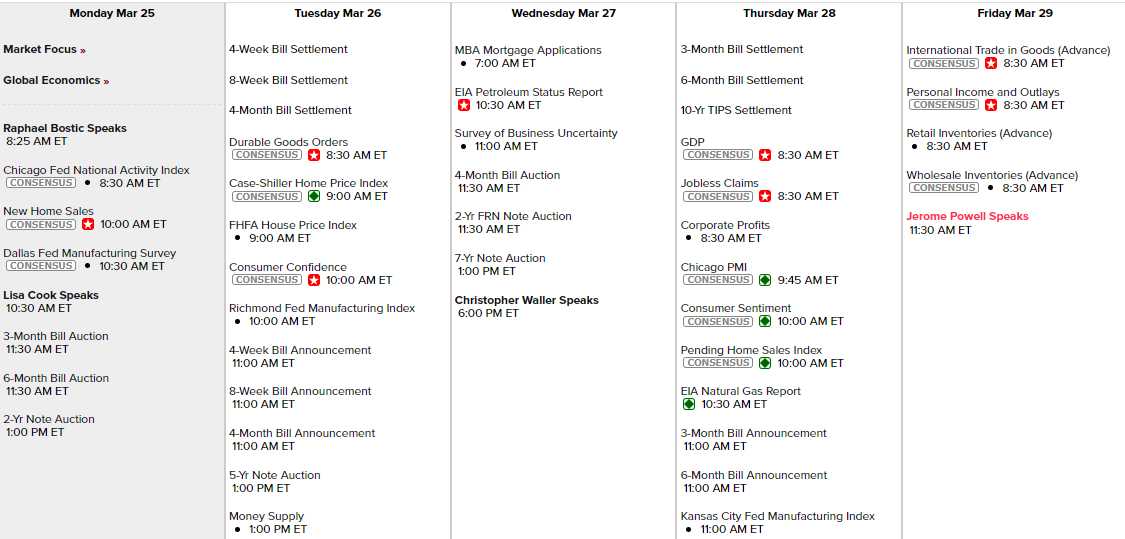

Let’s see, we have only Bostic, Cook (both today) and Waller (Wednesday) speaking other than Powell and it’s PMI, New Home Sales and Dallas Fed this morning (note auctions all week) followed by Durable Goods, Case-Shiller, Home Prices, Consumer Confidence and the Richmond Fed tomorrow. Wednesday just Business Uncertainty and the 7-year Auction, Thursday is GDP (3rd estimate of Q4 – yawn), PMI, Consumer Sentiment, Home Sales and Farm Prices (inflation indicator) and then it’s questionable whether Personal Income and Retail & Wholesale Inventories will actually come out on Friday – we’ll see.

And it’s amazing how many companies are still reporting earnings when the next cycle begins in a couple of weeks, officially April 12th when JP Morgan reports but LOVE reports Thursday morning and that kicks it off as far as we’re concerned. The earnings reports know Friday is a holiday. I see GME, RH, CCL – but not too much excitement there – so I guess we’ll be focused on data this week.

It always sucks to be a CEO and watch the stock pop when you resign but that’s what’s happening to Boeing (BA)’s Dave Calhoun along with Commercial Division’s Stan Deal (seems made up), who finally gave into the inevitable this morning. Fortunately, we just added a bullish spread on BA to our Long-Term Portfolio in our LTP Review – right at the bottom! Congrats to all who played along at home and – you’re welcome!

And isn’t that the whole point of what we teach you here at PhilStockWorld? Where the TA people see a terrible chart that’s breaking down – we see a value stock on sale. How are you going to “Buy Low and Sell High” if you don’t know what low (or high) is? Stock prices are not random numbers (though they seem like it at the moment) – they are an indication of the value of the companies they represent and they can be right or wrong(do you know the difference?). If you learn that – all the rest is easy!

It still won’t be smooth sailing for BA as this debacle has and will drain the company’s once-ample cash stockpiles and the board is going ahead with meetings with the major airlines without a CEO – and that can be a powder keg.

Google (GOOG) and Meta (META) are already joining Apple (AAPL) in an EU probe of “digital dominance” as my “live by the 7 – die by the 7” scenario for the markets is already starting to play out. Google’s App Store is getting the same treatment that was announced for AAPL last week and META’s new subscription fees for Instagram and Facebook could trigger fines from the EU of up to 10% of their GLOBAL Revenue and up to 20% if the violations repeat.

For META, 10% is $16Bn out of $52Bn in profits anticipated this year – ouch! GOOG makes $342Bn so $34Bn in fines out of $85Bn of expected profits – ouch and double ouch if they also count GOOGL, the way the indexes do (Ha! I knew that would come back to bit them!). They both count for $2Tn, which is 8% of the Nasdaq and 5% of the S&P!

Get ready for a fun ride this week – we’ll see how brave the bulls are going to be into the long weekend, which also ends the month and the quarter…

{kind=link}