Stand by for interest rate cuts: the US is about to start, so expect Australia to follow

Just three weeks ago, Reserve Bank Governor Michele Bullock declared interest rate cuts unlikely in the next six months. But if there was any doubt about what’s going to happen to global interest rates, the US Federal Reserve chair Jerome Powell removed it on Saturday.

Before an audience of central bankers from around the world (including the deputy governor of Australia’s Reserve Bank Andrew Hauser), Powell declared the long-awaited US rate cuts were about to begin.

“The time has come for policy to adjust,” Powell said, with a refreshing clarity that left no room for ambiguity.

“The direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

Rate cuts by the US Fed and other central banks will create a near-irresistible pressure for Australia’s Reserve Bank to follow.

My tip? Australians are likely to get a rate cut as soon as Melbourne Cup Day, Tuesday November 5. Here’s why.

{kind=link}

What happens in the US will happen in Australia

When the US Fed’s rate-setting committee next meets on September 17 and 18, it looks certain to cut the US Federal Funds rate for the first time since it began lifting it in 2022.

The US would join the United Kingdom, China, Canada, New Zealand, Switzerland, Denmark, the European Union, and a host of other jurisdictions in cutting rates – some of them repeatedly – to shore up their economies.

Financial markets are pricing in the equivalent of four ordinary-size rate cuts in the US by the end of the year. Given the US Fed has only three meetings left this year, this implies they are expecting at least one cut to be a double.

Australia and the US aren’t that different

The US story, as Powell told it over the weekend, is also the Australian story.

Describing what he called the rise and fall of inflation in his speech, Powell explained inflation took off when consumer spending surged after the end of COVID restrictions.

The supply of goods was unable to keep pace at first, and consumers switched their spending to services.

Then Russia invaded Ukraine, ramping up energy and food prices and making high inflation a truly “global phenomenon”.

What brought inflation down from late 2022 was a return to normal in the supply of goods and food and energy, and restraint in consumer spending brought about by a series of aggressive interest rate hikes.

‘Anchored’ expectations of inflation

What has kept inflation falling without (so far) much damage to employment in the US has been surprisingly restrained inflation expectations.

If workers’ expectations about future inflation remain “anchored” to a figure that’s low, rather than soaring with actual inflation, they are likely to be modest in their wage demands and be more likely to keep their jobs.

Powell said it had been “far from assured that the inflation anchor would hold”.

In Australia – as in the US, the UK, Canada and most of the rest of the world – inflation has trended down since late 2022. And, just as in the US, our expectations remain anchored.

Australians expect further falls

Each month, the Melbourne Institute surveys Australians about the inflation they expect in the year ahead. On two of the measures, the expectations are ultra-low.

One is the so-called weighted mean, which ignores answers of greater than 5% and less than zero (on the grounds they are unrealistic) and averages the rest.

It suggests we expect an inflation rate of 2.6%: right in the middle of the Reserve Bank’s target band and not outsized in any way whatsoever.

Another measure is called the non-rounded inflation expectation. This excludes round numbers greater than 10 on the theory that if someone gives an answer of 15% they are not serious, but if someone gives an answer of 14.9% they are.

This measure suggests an inflation rate of 3.1%: almost exactly at the top of the bank’s 2-3% target band, and again nothing to get alarmed about.

Room to cut rates

With US inflation well-anchored, Powell said the US Fed can safely cut interest rates to support the labour market, which is beginning to weaken, as ours is here in Australia, although more slowly.

Those are the parallels, and they are strong. So the arguments for cutting interest rates in the US apply here as well, even if the timing is different. Australia moved later than the US on the way up and will move later on the way down.

And there’s another reason to believe that the cuts about to be unleashed in the US will flow through to cuts here, probably quickly.

The Australian dollar jumped after Powell’s speech. When Powell actually cuts rates, the Australian dollar is likely to climb further.

This is because cuts in the US make the US a relatively less attractive place to hold money and Australia a relatively more attractive place.

Cuts in one country flow through to cuts in another

The more the Australian dollar climbs relative to the US dollar, the cheaper the imports that are priced in US dollars become – which is another way of saying the lower Australian inflation becomes.

It’s the same for other countries. Merely by cutting their own rates, the US and other countries will be easing inflation in Australia. The more they do it, the more Australian inflation will ease, building up a stronger and stronger case for our Reserve Bank to cut rates.

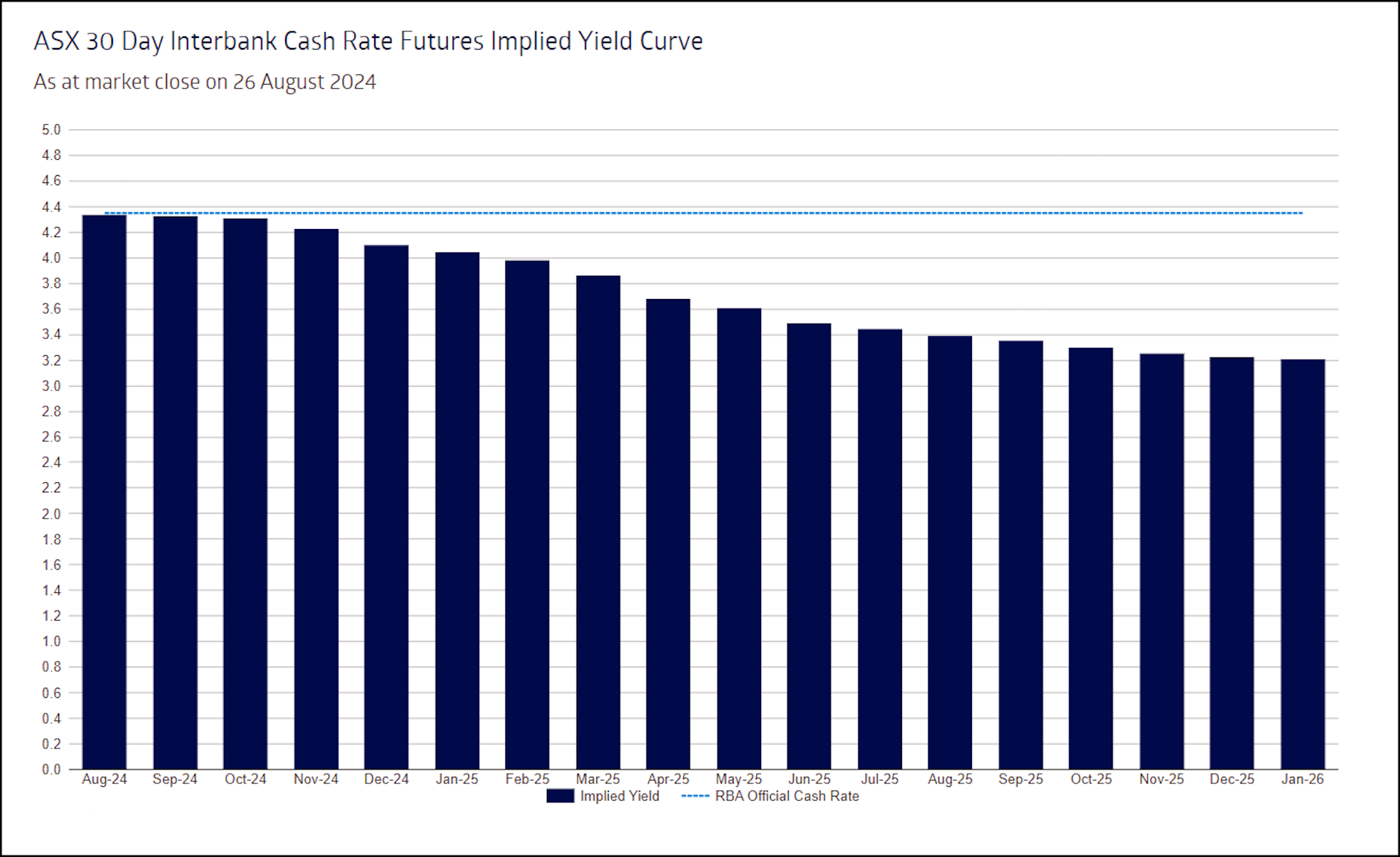

It’s why central banks tend to move rates together (albeit with delays). It’s why on Monday, Australian financial markets were pricing one interest rate cut by Christmas and a total of three by May.

{kind=link}

Traders don’t believe Australia’s Reserve Bank Governor Michele Bullock when she said interest rate cuts were unlikely in the coming months. They think what happens overseas will happen here too.![]()

Peter Martin, Visiting Fellow, Crawford School of Public Policy, Australian National University

This article is republished from The Conversation under a Creative Commons license. Read the original article.