The stock market is touching highs, but some corporate icons have seen valuations crash. I believe dispersion, China, and a changing of the guard are key to understanding these fallen angels.

Dispersion

In 1996, at the height of the brand era, I was asked to address the board of Levi Strauss & Co. on the future of brands and retail. The title of my presentation was “The Death of Distance.” The rap was that brands need to establish direct relationships with consumers (e-commerce), as digital technology would disperse products and services without regard for existing distribution channels.

This happened. Amazon dispersed retail to desktop, to mobile, to voice. Netflix dispersed DVDs to the mailbox, then to every screen as net neutrality enabled them to replicate tens of billions in cable infrastructure at near-zero cost, freeing up billions that resulted in a content/price ratio traditional players could not match. The pandemic accelerated dispersion of the office (remote work), healthcare (telemedicine), and education (online learning). What I didn’t see, however, is that AI would be steroids for dispersion, enabling anyone to leapfrog everyone.

Intel

Moore’s Law, named for Intel cofounder Gordon Moore, is an observation that the number of transistors on a microchip doubles every two years. It’s a meme that encapsulates the relentless pace of technological progress. When I graduated from the Haas School of Business, Intel was the job everyone wanted, as the firm was surfing Moore’s wave, which was doubling in size every two years. The “Intel” phenomenon could (now) be described as the ability to shed the majority of your value, despite being the leader in a booming industry. Few firms have fallen so far, so steadily, as Intel.

At its peak in 2000, Intel’s market cap was $500 billion. Since then, the S&P is up 243%, and Intel down 80%. If Intel had kept pace with the S&P, the firm would be worth 16X what it’s worth today. A stark reminder of this fall from grace: Jensen Huang (CEO, Nvidia) is worth more than Intel. The firm is at risk of being dropped from the Dow. Many icons disappear as everything everywhere ends. However, this fall is extraordinary, as leading firms usually experience this type of value destruction when they are helpless in the face of a sector’s decline. This is on Intel, as its market has boomed, with semiconductor sales increasing 18% globally YoY and 21% in China. Intel’s brand and enduring legacy of Andy Grove mask what is arguably the worst managed firm of the last 20 years. At the beginning of 2021, Intel and Nvidia commanded the same market capitalization. Today, the wizard behind the AI curtain is worth 30 Intels.

Intel missed dispersion, i.e., failed to capitalize on mobile and AI. While it remains the biggest maker of processors for PCs and laptops, Intel no longer has the power to predict the future by making it. The future belongs to Nvidia. Five years ago, Nvidia was a second-tier semiconductor firm best known for giving Call of Duty better resolution. Today, it’s the third-most-valuable company on earth, with between 70% and 95% of the AI chip market. With a P/E ratio of 99 Intel is still likely overvalued. But the game’s not over; Intel is shifting its business model to serve as a manufacturer for other chip companies, including Nvidia and Apple, that outsource the part of the supply chain that was supposed to be the ultimate moat: manufacturing. It ends up, there are a lot of moats (slack supply) that can be rented. In sum, Intel aspires to become the picks and shovels of a market they once dominated.

TSMC, which has 60% of the “foundry” market, reported gross margins of 53%, compared with Nvidia, the leading pure play chipmaker, which reported margins of 75%. The front-end, branded chip has higher margins and is a much better business. However, at $100 billion, in a market where CapEx rivals nations, Intel just needs to show a pulse to substantially increase its valuation. Their key advantage is not their brand or IP, but that they have lost so much value that they have (much) less to lose. Leveraging their brand and IP to be the best house in a bad neighborhood could result in a dramatic increase in value … from here.

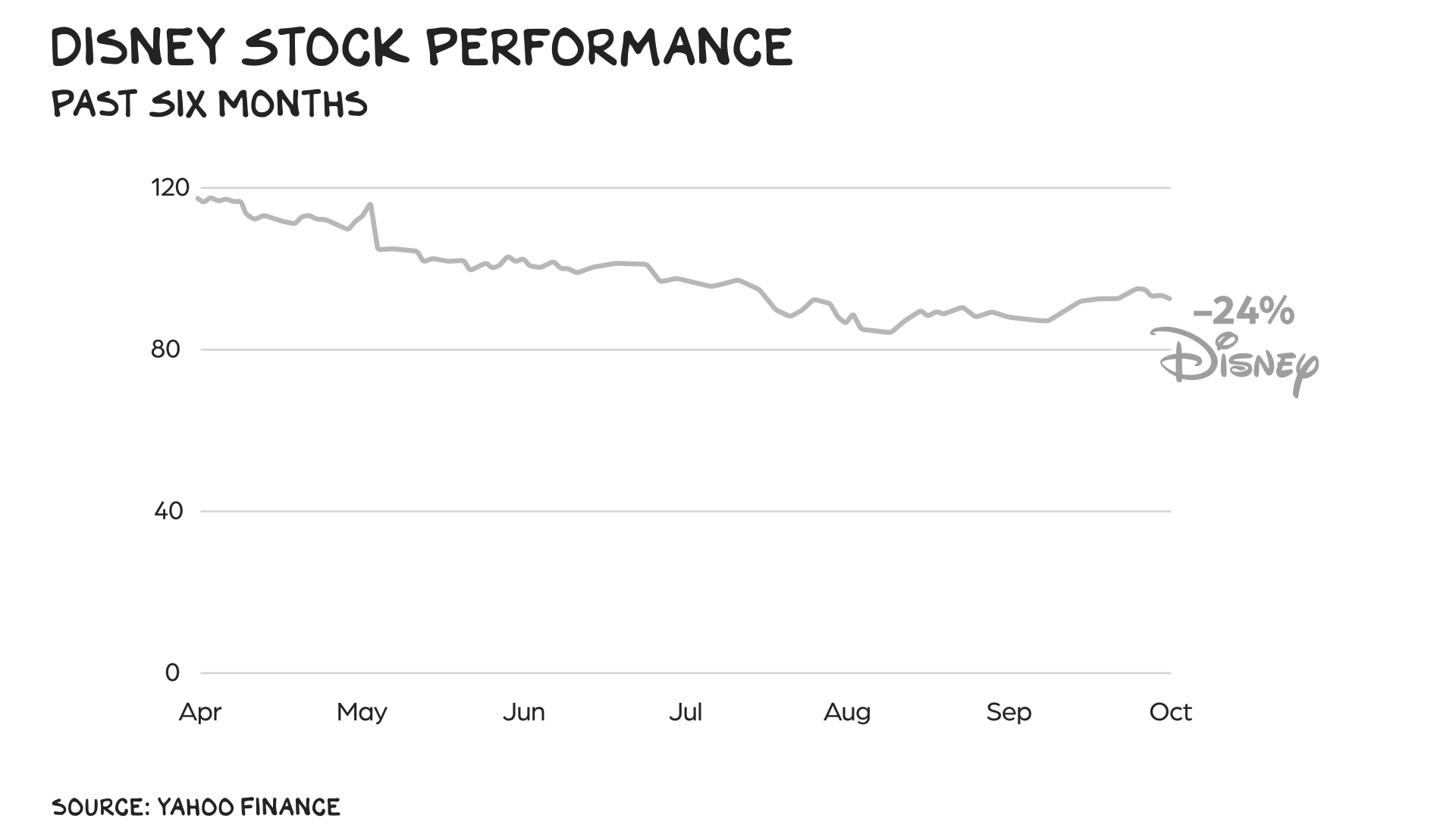

Disney

Hollywood is becoming a fair-weather Detroit. Less than 50% of all TV usage is attributed to linear as streaming now dominates. Domestic film and TV production is down 40%. The year before GM and Chrysler declared bankruptcy, their auto sales were off 23% and 30%, respectively. It would be convenient, and more dramatic, to claim this is because of AI. It isn’t. The root cause is more pedestrian; content budgets are up 3% this year, but studios can find people to do the same thing for less money elsewhere. Half of Netflix’s $15 billion annual content budget is now spent overseas. Note: Los Angeles will not register similar urban blight as, you know, weather.

Disney, unlike Intel, can blame the weather … or at least the atmospherics. Despite having 10,000 screens, AMC is not known as the largest theatrical distributor but a meme stock. In the past three years, Paramount Global market cap dropped from $43 billion to $7.5 billion. Warner Bros. Discovery lost two-thirds of its value in two years. YouTube, which spends zero on content as it splits revenue with creators, accounts for 10% of TV viewership. Netflix is second with 7.6%. But even the streamers that leapfrogged legacy media should worry about TikTok, which provides quick, perfectly calibrated dopa hits for two+ hours per day.

Amid all the wreckage of Hollywood is the once seemingly impenetrable Disney castle, which has shed half its value as its P/E ratio dropped from 283 to 36 over the past three years. If Hollywood is Detroit, Disney is Ford. Theatrical is in structural decline, but Disney accounted for 42% of the global box office with only three films: Deadpool & Wolverine, Inside Out 2, and Alien: Romulus. Cable is dying, but Disney owns so much content — Hulu, ABC, FX, ESPN, Marvel Studios, Lucasfilm, Pixar, 20th Century Studios, and National Geographic — that its streaming services are becoming the new cable bundle. But even with price hikes, access to the entire Disney streaming ecosystem, without ads, costs $159.99 annually; a mid-tier cable package costs $1,380 per year.

At the parks, which accounted for 36% percent of revenue last quarter, operating profit dropped 3%, as attendance slowed industry-wide. Disney and Comcast, which owns Universal Studios, blamed competition with international travel. At the low end, a three-night Disney World vacation for a family of four costs $2,783. According to a recent survey, 45% of parents take on debt for a Disney vacation. My take: Disney parks, similar to a Santa Monica producer of reality TV content, cost too much for not enough. Disney recognizes this and announced a $60 billion investment to improve the value prop. Pro tip: Deadpool ride.

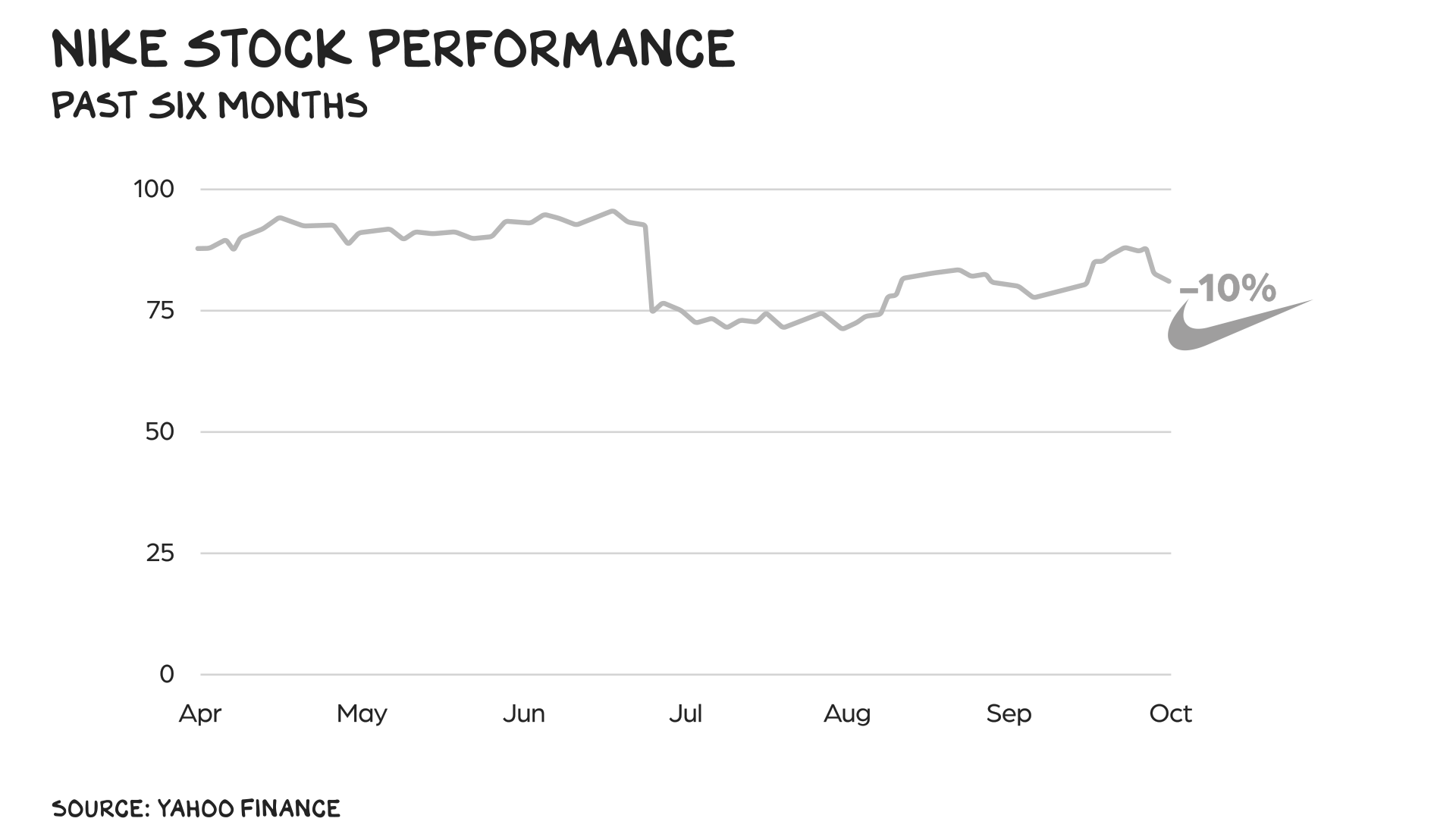

Nike

Wearing Nike makes me feel stronger. I love Nike, especially the unapologetic brand positioning: “You don’t win silver, you lose gold.” But after losing 50% of its value in three years, Nike is nowhere near the medal podium.

During the pandemic, running clubs boomed. This should’ve been great news for Nike. Instead, it was a shot of adrenaline for Nike competitors. (Hoka sales were up 27% last quarter, while Q3 sales for On were up 46%.) Meanwhile, Nike’s former CEO John Donahoe blamed remote work for the firm’s innovation slowdown. Donahoe represented a pivot to digital and direct to consumer. When Nike was my client, I advocated for this strategy, as dispersion would neutralize Nike’s best weapon (broadcast advertising). But the FuelBand never gained traction, DTC revenue was down 13% last quarter, and ultimately Donahoe confirmed that Nike leaned into digital and DTC at the expense of retail partners — a decision that hurt Nike, as retail returned stronger than expected post-pandemic and Nike lost touch with cutting-edge smaller retailers. And then China sneezed, and Nike caught full-blown pneumonia. Fourth-quarter sales in China dropped 19%, and Nike warned investors to expect more bad news. This quarter, Nike’s sales were down 10% YoY and down 4% in China.

Still, there’s nothing wrong with Nike that can’t be fixed by what’s right with Nike. Their new CEO, Elliot Hill, represents a return to the brand’s roots; the stock popped 7% on news of his hiring and then gave it back (see above: sales down 10%). And while this isn’t investment advice, Nike’s P/E ratio has dropped from a 2020 high of 73 to 23, suggesting that the stock is undervalued. It’s going to take time, as this may be a board problem. Nike, after shitting the bed on its earnings call this week, announced they would no longer be providing guidance. This is just plain stupid, and a rookie move from a great company. When things are bad, you OVERcommunicate, and if Nike’s management team is so thin the board lets them punt on key information flows to investors, then they shouldn’t be in the S&P 500.

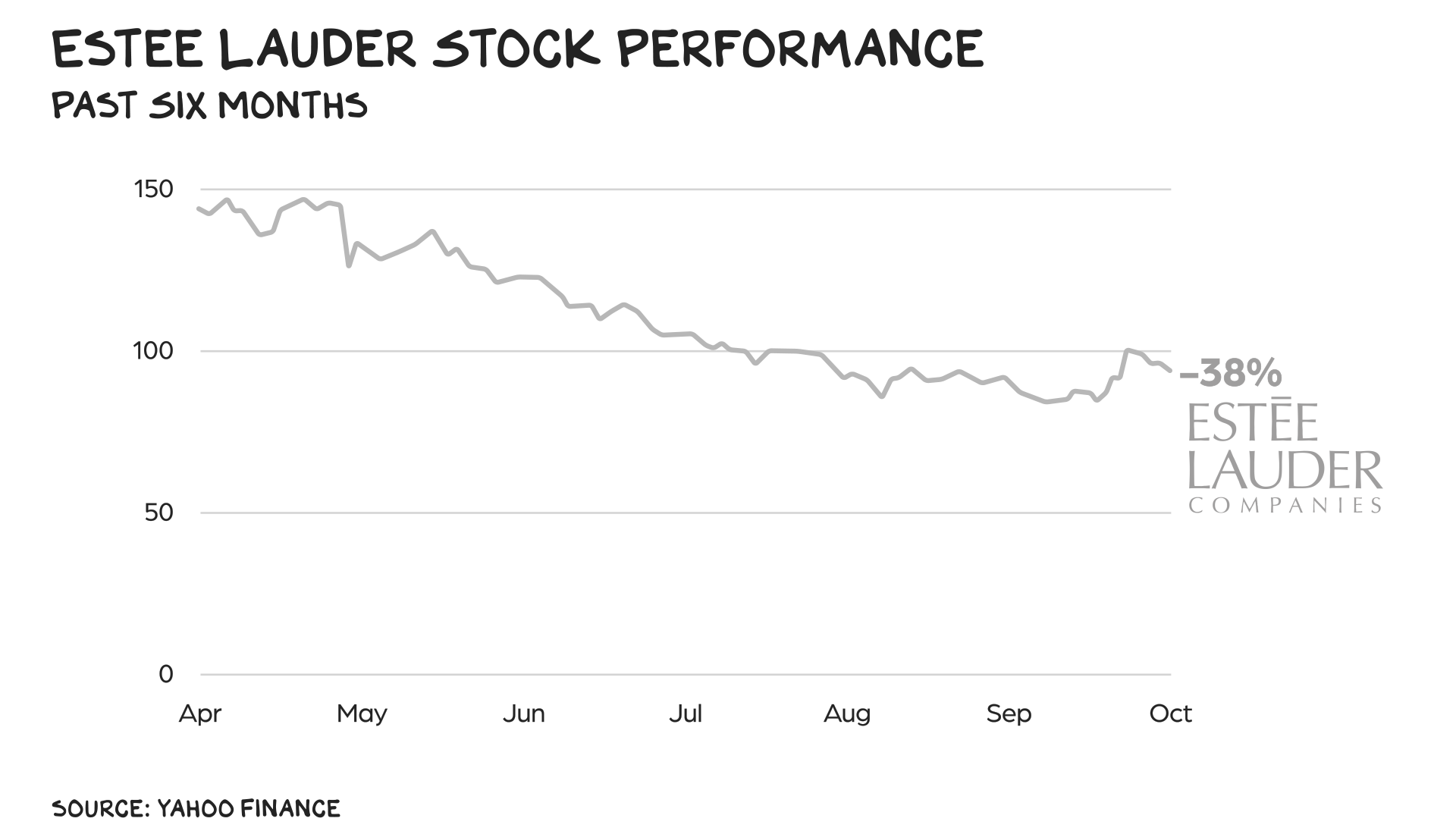

Estée Lauder

{kind=link}

At first blush, it’s easy to blame China for Estée Lauder’s 75% drop in market cap over three years. But Estée Lauder used that explanation pre-pandemic, during lockdowns, and post-pandemic. Meanwhile, the global beauty market has been relatively strong, growing 10% from 2022 to 2023, while China’s beauty market lagged, growing by only 3% amid heavy price discounting. Estée Lauder, L’Oréal, and Shiseido have all struggled in China recently, although Estée Lauder has struggled the most.

But a bad economy isn’t automatically bad news for luxury brands. The “lipstick effect” is a theory that says during economic downturns consumers on tight budgets still splurge on small, affordable luxuries, as such purchases give people a sense of indulgence without breaking the bank. The question isn’t whether budget-conscious Chinese consumers have soured on luxury, but whether they’ve soured on Estée Lauder? According to Vogue, it’s the latter. Proya is set to become the first Chinese beauty brand to hit $1 billion in revenue. Chinese beauty brand Florasis will open its first counter in Paris. Direct-to-consumer brand Uniskin launched its first brick-and-mortar store in Shanghai.

The HBO show Succession was a modern-day Shakespearean drama that captured the essence of power, wealth, and family dysfunction. Ostensibly, it was about Rupert Murdoch, but it also could’ve been about Sumner Redstone, or the Estée Lauder family, which owns 35% of the company and controls 80% of the voting power. Ultimately, this isn’t about China or navigating dispersion; it’s about the frailty of family dynasties. Such dynamics make for good TV drama, but they’re lousy for shareholder value. Similar to Nike, Estée has missed key trends and finds long-tail brands nipping at every appendage.

The Green Mile

Dispersion and the rise of China both began in the 1990s. Three decades later, China is the world’s second-largest economy, and it has more middle-class households than the U.S. Dispersion is no longer coming; it’s here, and AI will take it in new directions. Similar to Congress, there are just too many old people in corporate America clinging to power. One of the key problems in America is a lack of churn. Politicians, CEOs, and tenured faculty refuse to leave, creating a stasis that is bad for the economy, as our country is run by people who are out of touch, and reduces opportunity for young people. If that sounds ageist, trust your instincts. I am an ageist, and so is biology.

At 73, Bob Iger is the oldest CEO of the fallen angels I discussed here. His first, second, and third priorities need to be picking a successor. At 60, Nike CEO Elliott Hill is the youngest fallen angel boss, and like Iger, he came out of retirement to turn an iconic company around. Pat Gelsinger, 63, started his career at Intel at 18. His mentor was Andy Grove, a leading gangster CEO of the last century. Estée Lauder CEO Fabrizio Freda is 67. He’s retiring after 16 years at the helm. Maybe it’s a vibe, as my kids say, but a changing of the guard is upon us.

Comebacks

In January of 2011, Netflix was worth $11 billion. By November, the company’s market cap was just over $3 billion. The reason? As Netflix pivoted to streaming it tried to spin off its DVD business. The Qwikster backlash cost Netflix 1 million subscribers. As it turned out, Netflix was right, but early, as they ultimately closed their DVD business in 2023. In 2012, Best Buy was on the brink of bankruptcy and the big-box sector looked doomed. A year later, Best Buy’s market cap increased 3X as a new CEO led one of the biggest turnarounds in retail history. And then there’s the turnaround story everyone knows: Apple.

We’re wired to overestimate the impact of negative events, a phenomenon known as the negativity bias. It’s a cognitive distortion that makes us believe that failures have a greater impact than they actually do. At some point, every business experiences a crisis, i.e., an opportunity.

As a Professor of Brand Strategy, I can’t help but wax nostalgic and believe these firms are ripe for a comeback. They all boast global brands, talented workforces, and robust supply chains. However, the most attractive thing about these firms is just how badly they’ve been beaten down. In the first four weeks of 2024, Nvidia added the value of all four of these firms. And that’s the bull case as at some point every stock (unless it’s going to zero) is too expensive/cheap. These angels have fallen so far, redemption is overdue.

Life is so rich,

![]()

P.S. This week on Prof G Markets, Ed and I spoke with Lina Khan, chair of the Federal Trade Commission, about Unlocking Innovation Through Antitrust Enforcement. Listen and subscribe here on Apple or here on Spotify.

P.P.S. Section just confirmed Moderna’s VP of AI & Product Platforms and S&P Global’s Chief Artificial Intelligence Officer as speakers for the AI:ROI Conference. It’s free to attend on Nov. 14 – register to learn from real AI leaders.