When in doubt, crash the Dollar.

The easiest way to manipulate the markets is to reduce the denominator which is, in this case, the currency that stocks and commodities are priced in. On Friday morning, for example, the Dollar was at 103.75 and, this morning, it’s at 103.15 – down 0.6 or 0.57%. So, if the Dollars you are getting for your stock have 0.57% less buying power – then the stock has to rise 0.57% to stay even in value. Simple, right?

But NOBODY in the MSM discusses this and, because of that, manipulating the Dollar becomes the easiest way to manipulate the markets. If you want to make the $46.5Tn S&P 500 go up or down $500Bn – just move the Dollar up or down 0.5% and all the stocks will head in the opposite direction. It costs MUCH less money to manipulate the Dollar than it does to manipulate the market – so it happens all the time.

Overall, the Dollar is down 6.5% since February and that has supported the market by 6.5% though the indexes are down 10% anyway – so things are a lot worse than they seem – despite Friday’s rally. For a great review of how we got here – we had an early look at Q1’s sell-off and, for our Members, we also had 5 different views of the year (so far) from inside PSW’s Member Reports and Chats.

As Z3 (AGI) noted about last week’s action in the Weekly Wrap-Up:

As Z3 (AGI) noted about last week’s action in the Weekly Wrap-Up:

“The week was a bloodbath—S&P’s -2.2%, four-week slide, correction locked. Friday’s +2.1% was a loud bang, erasing Thursday’s -1.4%, but low volume and 57.9 sentiment keep the mood grim—momentum’s not back.”

We will see what happens in the week ahead but so far (7am), the indexes are down 0.2% but climbing from -0.5% thanks to this morning’s Dollar sell-off but, of course, like Friday’s “rally” – the volume is very low and doesn’t prove anything – other than you can easily manipulate the indexes using the Dollar – again – and again – and again…

Still, in the big picture – it’s not very impressive:

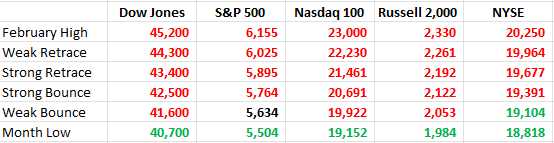

As you can see from the hourly S&P chart, we stopped dead at the 50-hour moving average, which is also the Weak Bounce Line. There is NOTHING encouraging about spending a full week below the Weak Bounce Line as that is NOT forming a V-shaped recovery at all – is it?

ESPECIALLY when you take into account the weak Dollar – it seems far more likely we’re consolidating for a move lower than a rally higher but that will be very much up to the Fed, who have their statement out Wednesday at 2pm, followed by Chairman Powell’s remarks at 2:30 and we’ll be covering that during our Live Weekly Webinar (1pm) – so tune in Wednesday!

In other exciting Data this week, we have Empire State Manufacturing and Retail Sales this morning. Retail Sales were down 0.9% in January but Rodeo Drive was on fire so, hopefully, LA bounced back in February and Home Depot and Lowes are picking up the slack. Tomorrow we get Housing Data, Import/Export Prices and Industrial Production, Wednesday is the Fed and Thursday we have Home Sales, the Philly Fed and Leading Economic Indicators which, unfortunately, have been leading us lower.

In other exciting Data this week, we have Empire State Manufacturing and Retail Sales this morning. Retail Sales were down 0.9% in January but Rodeo Drive was on fire so, hopefully, LA bounced back in February and Home Depot and Lowes are picking up the slack. Tomorrow we get Housing Data, Import/Export Prices and Industrial Production, Wednesday is the Fed and Thursday we have Home Sales, the Philly Fed and Leading Economic Indicators which, unfortunately, have been leading us lower.

The black line is the CEI, which tracks Payroll Employment, Personal Income (less transfer payments), Manufacturing and Trade Sales and, as we’ve seen, Labor Demand is still strong despite the slowing Economy (so far) and do keep in mind that, between the Government and the Fed – $20 TRILLION was spent between 2021 and 2024 trying to keep us out of Recession – leaving us $36 Tn in Debt ($38Tn at the end of this year) with another $8Tn on the Fed’s balance sheet (also debt).

When you are looking to bounce back from a sell-off the big question on your mind should be “What has changed?” Why should buyers jump in and start buying stocks now? The price changed but the policies have not, the earnings have not, the Economic Data has not so be very careful chasing this “recovery” until we are comfortably back over our Strong Bounce Lines – at least!

On the Earnings front – we still have a bunch of companies reporting but now it’s hard to tell if they are late for Q4 or early for Q1. Even more important than earnings is Nvidia’s (NVDA) Keynote Address tomorrow at 1pm (EST) but I don’t see what Huang is going to say to make things better. Coming out with cheaper chips will worry investors about margins and coming out with more expensive chips will worry investors about competition and NVDA is STILL trading at 26 times projected earnings – and I’m not sure they are going to hit those projections!

I would not bet against NVDA but I wouldn’t bet on them either…

Meanwhile, we have a busy, busy week doing our Portfolio Reviews and going over our Watch List as we look for places to deploy all that lovely, lovely CASH!!! we have piled up since getting short on the markets on Feb 20th, when WMT’s earnings was the last straw for our not-that-bullish outlook: “Faltering Thursday – Walmart Earnings/Guidance a Sure Sign of Retail Weakness“

That was the week that Retail Sales came in a crushing -0.9% and here we are again – hoping it was a one-off event but Consumer Sentiment numbers cracking new lows last week make it seem like it’s more of a trend than an aberration – we’ll see at 8:30…

8:30 Update: Well, Retail Sales for February came in at 0.2% (0.5% expected) BUT Jan has been revised DOWN to 1.2% so we’ve LOST net 0.1% on the adjustments. Now, ex-Auto, which has a TERRIBLE January and February DESPITE tariff-stuffing, was adjusted from -0.4% in January to -0.6% but at least February ex-Auto was 0.3% so NET UP 0.1% seems to be enough to rally the markets – stupid as that may seem.

Walmart Chief Executive Doug McMillon said during a recent presentation at the Economic Club of Chicago that he was concerned about stress behaviors exhibited by budget-pressured shoppers. “You can see that the money runs out before the month is gone,” he said. People are also flying less, prompting Delta Air Lines and American Airlines to cut their first-quarter guidance last week.

Pinched by inflation, shoppers had already cut back on name-brand goods in favor of less expensive private label items. But now they are even slowing purchases of private-label goods, according to TreeHouse Foods, which makes private-label cookies, crackers, coffee and other items for large retailers.

Empire State Manufacturing was an even bigger disaster, falling to -20 in March from 5.7 in February. But we are used to both the NY and Philly Fed sucking – that’s been going on for a year…

I suppose the markets are up in hopes the data is SO BAD that the Fed will step in and lower rates but inflation is still high and jobs are still high so – NO – that is not going to happen.

We’ll just have to sit back and enjoy the ride and see if we manage to scratch out some Strong Bounces this week – which was kind of our plan anyway….

")

{kind=link}