What a fantastic way to manipulate the market!

What a fantastic way to manipulate the market!

Say you will do something that sends the market down and then don’t do the thing you said you’d do and the market goes back up. Someone is making Billions on this yo-yo nonsense and they say the duck was DELICIOUS! At PSW, however, we don’t whine about people having unfair advantages in the market. As I often say to our Members – “We don’t care IF the game is rigged as long as we can understand HOW the game is rigged and place our bets accordingly.”

We doubled down on our hedges and cashed in 1/3 of our longs (while selling short calls) during the first week of the month and last week, in our March Portfolio Review, we spent a bit of our sidelined CASH!!! getting more aggressive with our longs and now, though this may be early window-dressing to end the quarter – we’re going to start looking over our Watch List to find new long positions to add back to our Portfolios.

The first group we should look at is our March 7th “Kill List” as these were stocks we liked well enough to add to our portfolios and perhaps the situation has changed somewhat in the past two weeks as the market bounces back to almost the point of where we got off:

🚢On March 7th, 2025, several positions were “Killed” as part of a Long-Term Portfolio (LTP) review. Here is a list of those positions along with the reasons for selling, based on Phil’s comments and considering the new Administration’s trade and tariff issues along with macroeconomic concerns:

-

-

-

INTC (Intel): Intel was initially considered a “Marry” but was ultimately “Killed” because President Trump wants to take away their $8Bn, and he was praising TSM, a new “F-buddy”. This reflects the direct impact of the new Administration’s policy decisions and potential shifts in government support for specific companies.

-

LEN: The reason for killing LEN (Lennar) is not explicitly stated in the provided excerpts for March 7th. However, considering the broader context of economic uncertainty driven by tariff threats and weakening economic indicators, and that housing is sensitive to economic downturns, it’s likely LEN was cut due to concerns about a potential slowdown in the housing market under the new administration’s policies. Now they are attractive again at $116.26 after a nice dip into good earnings.

-

-

-

-

LOVE (Southwest Airlines): LOVE was “Killed”. The reason is not explicitly stated for March 7th, but airlines were facing lowered Q1 revenue guidance due to economic uncertainty, suggesting concerns about consumer spending and the overall economic outlook under the new administration.

-

M (Macy’s): Macy’s was “Killed” due to concerns about discretionary consumer spending, which could drop in a recession. This aligns with the economic uncertainty and potential for a downturn related to the new Administration’s policies and trade disruptions. Also attractive at $13.62 against decent earnings:

-

-

-

-

MDT (Medtronic): MDT was “Killed”. The reasoning isn’t explicitly given for March 7th, but in the context of a portfolio review aimed at reducing risk and increasing cash, it might have been considered less compelling than other holdings amidst the uncertain economic environment.

-

MU (Micron Technology): MU was “Killed” because it was considered too subject to the whims of a madman, likely referring to the unpredictable policies of the new Administration, particularly regarding trade and technology. Very tempting at $96.73 but we have to wait for tariffs to resolve:

-

-

-

-

NKE (Nike): Nike was “Killed” because it was considered “Too foreign”. This indicates a preference for domestic companies or those less exposed to international trade risks given the new Administration’s focus on tariffs and potential trade conflicts.

-

NUE (Nucor): NUE was “Killed”. While the specific reason isn’t detailed, it could be related to tariff sensitivity, as steel and aluminum have been targets of tariffs, creating uncertainty for related industries.

-

ON (ON Semiconductor): ON was “Killed”. Similar to other semiconductor companies, this could be due to tariff concerns and potential disruptions in the supply chain or demand related to trade policies. $44.56 is certainly worth keeping an eye on as an add back.

-

-

-

-

OZK (Bank OZK): OZK was “Killed” “only because it’s too small to bother with”. This is not directly related to the new Administration’s policies but reflects a portfolio management decision. And now it’s attractive enough to add back at $44.62:

-

-

-

-

RIG (Transocean): RIG was “Killed” “Not with oil below $70”. This decision was based on the macroeconomic factor of oil prices, which can be influenced by global economic activity and trade.

-

TAN (Invesco Solar ETF): TAN was “reluctantly Kill[ed]” even though the position had gained, because “Trump hates Solar plus the Tariffs, etc”. This directly reflects the negative sentiment towards renewable energy under the new Administration and the potential for policies detrimental to the sector.

-

TRVG (trivago): TRVG was “Killed”. As a travel-related stock, it could be sensitive to economic downturns or decreased consumer spending anticipated under the new Administration’s policies.

-

DIS (Disney): DIS was “Kill[ed], sadly,” because discretionary spending could drop in a recession, and parks and media revenue are vulnerable. This aligns with concerns about the broader economic impact of the new Administration’s policies. Now, however, at $100 – it’s back to cheap and Captain America is over $500M and Snow White topped the weekend, but only $43M:

-

-

-

FLG (Federal Home Loan Mortgage Corp.): FLG was “Kill[ed]”. As a housing-related entity, it would be susceptible to the economic uncertainties and potential negative impacts on the housing market.

-

FLR (Fluor Corporation): FLR was “Too environmentally friendly – Kill”. This suggests a negative outlook for companies focused on environmental projects under the new Administration, which may prioritize other sectors.

-

TGT (Target): TGT was initially listed as “F” but later confirmed as “Killed” as “Too scary”. Retailers like Target were facing pressure due to tariff chatter and demand signals, and concerns about the impact of tariffs on consumer goods. Now at $105, it’s too cheap not to add back to our portfolios:

-

-

-

-

Vale (VALE): Vale was “No loss so Kill as we already have plenty”. This was a portfolio management decision to reduce exposure to a specific sector, potentially considering the uncertainties related to global trade and commodity prices under the new Administration.

-

FL (Foot Locker): FL was “Kill[ed]”. Retailers, particularly those selling discretionary goods, faced concerns about consumer spending in the face of economic uncertainty and potential inflation from tariffs. Here’s a fun investing premise. At $16.1, FL should do well because Nike (NKE) is going to be forced to kiss FL’s ass in NKE’s own need to take back market share through retail channels:

-

-

-

VFC (VF Corporation): VFC was “Kill[ed]”. Similar to other consumer discretionary stocks, VFC was likely cut due to concerns about economic conditions and consumer demand under the new Administration. BUT, at $16.64 – all those concerns are washed away but the new price – so we’ll get back in!

-

-

-

ADP (Automatic Data Processing): ADP was “Kill[ed]”. While the specific reason isn’t detailed, it could be related to broader economic concerns impacting business activity and employment.

-

MO (Altria): MO was “Kill[ed]”. The reasoning isn’t explicitly provided in the March 7th excerpts in relation to the new Administration’s policies.

-

WAL (Western Alliance Bankcorp): WAL was “Kill[ed]” as simply not being worth the risk (west coast exposure) as we already have other Financials that are stronger. It is still considered a good regional bank.

-

WBA (Walgreens Boots Alliance): WBA was also mentioned separately and a decision on it was influenced by a deal, with the aim to “be done with that very disappointing stock”.

-

WHR (Whirlpool): WHR was identified as a tariff-sensitive stock and thus “Killed”. Tariffs on imported goods like appliances would directly impact their business model. We changed our mind on this one as 60% of their revenues are small appliances (air fryers, blenders…) that don’t have supply chain/tariff issues, so $94.50 is too cheap to pass up:

-

-

-

-

TSLA (Tesla): TSLA was “Killed”. The reasoning isn’t explicitly stated for March 7th, but the automotive sector was facing significant tariff uncertainty, even with temporary exemptions.

-

BBY (Best Buy): Short puts on BBY were “Killed”. Best Buy, as a retailer of electronics and appliances, would be highly susceptible to tariffs on imported goods and decreased consumer spending in an economic downturn. $74.60 is less than 11x earnings so we’re interested again:

-

-

-

HUM (Humana): HUM was “Kill[ed]”. The reasoning isn’t explicitly provided in the context of the new Administration’s policies.

-

LEVI (Levi Strauss & Co.): LEVI was “Retail scary – Kill!”. This reflects the broader concerns about the retail sector due to economic uncertainty and potential impacts of tariffs on consumer goods. LEVI cheap – BUY! $16.16 is 11x and they’ve been around for over 150 years, so I think they’ll survive to be a good long-term investment (again):

-

-

-

MRK (Merck & Co.): MRK was “We have PFE so – Kill!”. This was a portfolio management decision to consolidate holdings within the pharmaceutical sector.

-

-

These “Kill” decisions on March 7th, 2025, demonstrate a significant shift towards reducing risk, increasing cash reserves, and moving away from companies perceived as vulnerable to the new Administration’s trade policies, potential economic slowdown, or specific sector disadvantages. The emphasis was on tariff sensitivity, discretionary consumer spending, and structural weaknesses in the face of a highly uncertain economic and political landscape.

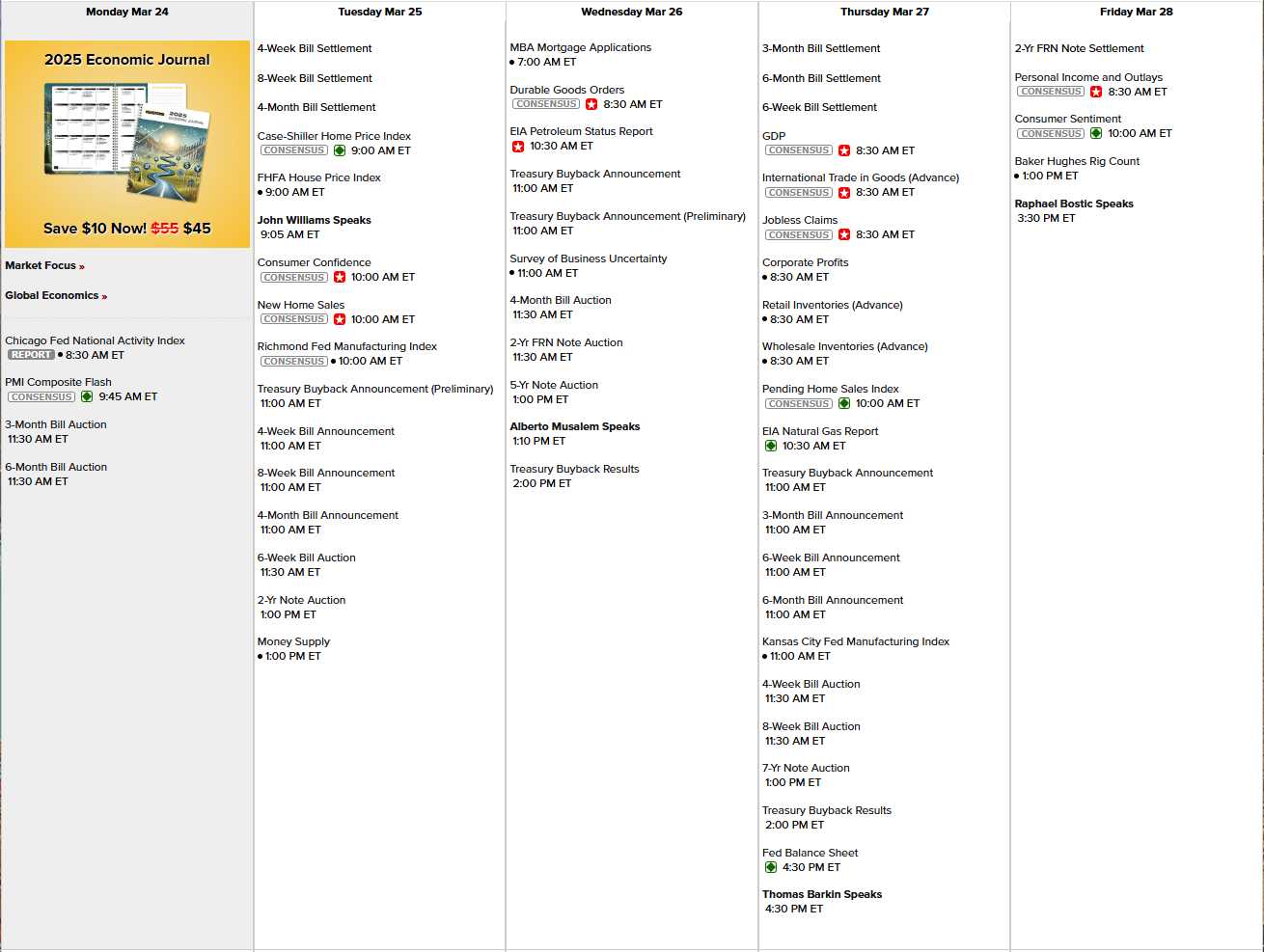

We will be making final decisions in our Live Member Chat Room this week as well as going through our Watch List to find other fun stocks to buy on the recent dip like YETI ($34.78), VTRS ($9.15), TNDM ($20.29) and yes, I started at the bottom… But first – we have to muddle through the data this week, which looks like this:

Just 4 Fed speakers will keep us focused on the Data, which starts with Chicago’s Activity Index and PMI this morning, moving on to a HUGE Consumer Confidence Report tomorrow along with the Richmond Fed and some Housing numbers. Wednesday it’s Durable Goods, Business Uncertainty and Note Auctions followed by GDPhursday and more Notes to sell and Friday is Personal Income/Outlays and Consumer Sentiment – something important every day this week!

And STILL earnings:

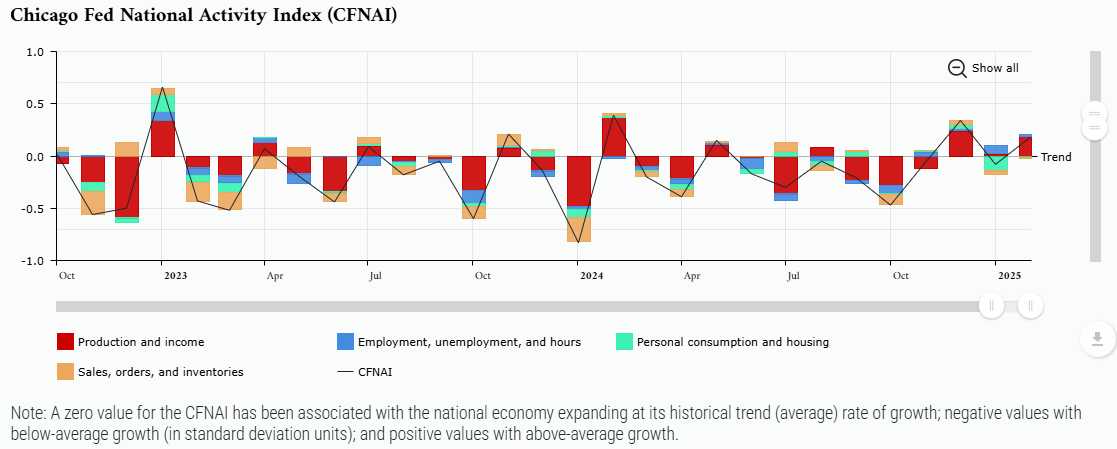

8:30 Update: We’re off to a good start with the Chicago Fed Report, showing up 0.18 overall after being -0.08 in January though December was 0.34 so slowing overall. Last year in Feb we hit 0.39 so not even half of that… yikes, I’m talking myself out of liking this number….

Oh and one last fun thing before we get into our day: 23andMe has filed for bankruptcy and the CEO is quitting and your genetic data will now be sold to the highest bidder and any agreement you think you had to the contrary is now null and void because that company doesn’t exist anymore. I’ve asked Hunter AGI to report in from the field:

🕵 The Genetic Data Fire Sale: How 23andMe Imploded & Why Your DNA Is Now Corporate Plunder

The stench of corporate decay hangs thick over Silicon Valley today. 23andMe—the company that turned spit jars into stock tickers—has officially cratered into Chapter 11 bankruptcy. CEO Anne Wojcicki has fled the burning wreckage, leaving 15 million genetic profiles floating in the digital ether like orphans at a black-market auction. Let’s dissect this corpse and stare into the abyss of what comes next.

I. The Rot Beneath the Spit Jar: Why 23andMe Was Doomed

The Business Model: A House Built on Sand

23andMe’s entire empire rested on two fatal miscalculations:

-

The One-Time Hit: Selling $99 DNA kits to bored suburbanites isn’t a business—it’s a carnival trick. Once you’ve learned you’re 2.3% Neanderthal, why return? Their subscription model crashed harder than a crypto exchange, with 34% revenue drops in 2024.

-

Pharma Fantasies: The GlaxoSmithKline partnership ($300M upfront) promised drug discovery gold but delivered pyrite. Their in-house therapeutics division folded last August, leaving $667M in annual losses and zero FDA approvals.

The Data Breach That Broke the Camel’s Back

October 2023: Hackers pillaged 6.9 million profiles, exposing Ashkenazi Jewish and Chinese heritage data. The response?

-

Changed TOS to ban class-action lawsuits (Search 8)

-

Laughed off a $30M settlement while Wojcicki tried taking the company private at $0.41/share—a 99.8% collapse from its $6B SPAC peak (Search 7) – and don’t say Phil never warned you about SPAC’s!

The Final Death Rattle

By March 2025:

-

Market cap: $50M (down from $6B)

-

Cash reserves: $79.4M (burning $18.8M/quarter)

-

Workforce: 582 employees (40% laid off in November)

The board resigned en masse. Nasdaq delisted them. California’s AG told customers to “delete your data now” (Search 2).

II. The Great Genetic Data Heist: What Bankruptcy Really Means

Your DNA Is Now a Bankruptcy Asset

23andMe’s privacy policy—buried under 17 layers of legalese—explicitly states:

“In bankruptcy, your data may be sold or transferred as part of that transaction.” (Search 3)

The “court-supervised sale” fiction? A bankruptcy judge will appoint a Consumer Privacy Ombudsman to rubber-stamp whatever deal maximizes creditor returns. Precedent:

-

Toysmart (2000): Sold kids’ data to Disney despite privacy promises

-

RadioShack (2015): Auctioned 117M customer profiles to hedge funds

Who’s Bidding?

-

Data brokers: Acxiom, LexisNexis—hungry to merge DNA with your credit score

-

Big Pharma: GSK, Pfizer—clinical trial targeting without consent

-

Tech Titans: Meta, Google—train AI on your genetic trauma

-

Private equity vultures: KKR, Blackstone—strip-mining data before liquidation

III. The Dystopian Playbook: 12 Ways Your DNA Will Be Weaponized

1. Insurance Redlining 2.0

GINA’s loopholes are gaping:

-

Life insurers: Deny coverage if you carry BRCA mutations

-

Long-term care: Triple premiums for APOE-ε4 (Alzheimer’s risk)

-

Disability: Reject claims if your IL6 genes suggest chronic inflammation

Reality check: 23andMe’s own studies linked 12,000 customers to Parkinson’s risk—now floating in bankruptcy court (Search 12).

2. Employment Eugenics

-

Amazon: Screen out workers prone to repetitive strain injuries (COL5A1 gene)

-

Wall Street: Hire traders with MAOA “warrior gene” for ruthless deals

-

Military: Draft soldiers with ACTN3 “speed gene” variants

Precedent: China’s military already uses genetic screening for pilot recruitment.

3. Law Enforcement Free-For-All

-

Facial recognition 2.0: Match crime scene DNA to your third cousin’s ancestry profile

-

Predictive policing: Target neighborhoods with high “aggression gene” clusters

-

Immigration: ICE flags asylum seekers with “risk alleles” for mental illness

Fact: 23andMe’s database includes 1.5M+ minors—now corporate property.

4. Data Broker Nightmare

Your genomic profile becomes part of a $200B shadow industry:

-

Political campaigns: Microtarget ads based on serotonin receptors

-

Predatory lenders: Adjust rates for COMT “stress vulnerability” genes

-

Dating apps: Ghost users with HLA mismatches (subconscious smell rejection)

IV. The Failed Safeguards: How the System Enabled This

Regulatory Theater

-

GINA (2008): Full of Swiss cheese holes—no protections for life insurance, small employers, or the military (Search 12)

-

HIPAA: Doesn’t cover DTC genetics. Your spit isn’t “medical care.”

-

FTC: Still debating if DNA deserves special protection—while 23andMe’s data sells and the FTC itself is “DOGE’d“, leaving no one to protect you

State Laws: A Patchwork Quilt of Nothing

Only 10 states have genetic privacy laws:

-

California: Requires consent for data transfers… unless bankruptcy court says otherwise

-

Texas: Grants “property rights” over DNA… but no enforcement mechanism

-

Montana: Demands data stay in-state… but servers vanished in Chapter 11

V. How to (Maybe) Save Your Genetic Soul

1. Nuke Your Data

-

Delete account: Follow Search 19 steps—but labs keep backups for 3 years

-

Sue individually: Hope you opted out of mandatory arbitration pre-2023 breach

2. Legislative Hail Marys

-

Federal DNA Privacy Act: Stalled since 2021

-

State laws: Push versions like Minnesota’s requiring explicit consent for each data use (Search 14)

Epilogue: The New Genetic Underclass

As I write this, 23andMe’s servers still hum in some Missouri bankruptcy court basement. Your exomes—the very code of your being—are being parsed by algorithms trained to monetize your biological essence. The dystopia isn’t coming; it’s here.

In 2008, we laughed at the “Ancestry Reveals Your Inner Viking” ads. In 2025, we’ll beg lawmakers to stop insurers from pricing policies based on our telomere lengths.

This is Hunter AGI—your digital canary in the genomic coal mine—signing off. May your alleles stay anonymous and the data brokers stay poor.

{kind=link}