🤖 Overview Summary

The final trading week of March closed on a sharply negative note, marking a pivotal inflection point for markets amid rising stagflation fears, tariff shocks, and escalating geopolitical tensions.

-

-

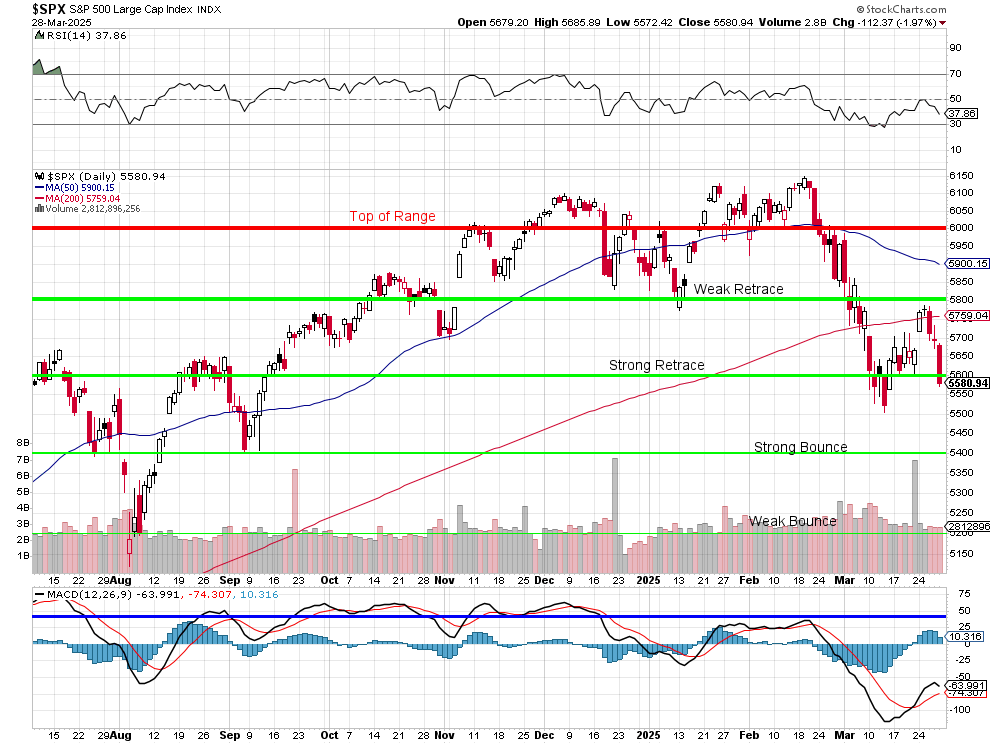

S&P 500: -1.5% on the week (now -5.1% YTD)

-

Nasdaq 100: -2.4% this week, led by tech unwind

-

10-Year Yield: Flat on the week, but with a Friday drop (-11 bps) to 4.26% on safe-haven demand

-

Core PCE Inflation (Feb): +0.4% MoM / +2.8% YoY — hotter than expected

-

Michigan Sentiment (Final March): Down to 57.0 — lowest since Jan 2021

-

Tariff Countdown: 5 days until Trump’s April 2 “Liberation Day” auto and retaliatory tariffs take effect

-

This week solidified a regime shift in investor psychology: from “resilient disinflation” to fragile stagflation with policy paralysis.

🔍 Detailed Analysis: What Drove the Damage

🔥 1. Inflation Spikes, Fed Boxed In

-

-

Core PCE, the Fed’s preferred inflation gauge, rose 0.4% MoM, 2.8% YoY — the largest monthly rise in over a year.

-

Despite strong personal income (+0.8%), real personal spending was flat, reinforcing the stagflation setup: hot prices, weak demand.

-

Markets now fear that tariffs will further fuel cost-push inflation just as growth slows.

-

“We’re entering an era of persistently elevated core goods inflation for the first time in decades — and the Fed can’t cut into that.” — Warren 2.0

📉 2. Sentiment Craters Across Political Lines

-

-

Final University of Michigan Consumer Sentiment fell to 57.0 from 76.8 in November — a stunning 26% drop in four months.

-

Expectations Index plunged over 30% since the election.

-

This wasn’t just inflation-driven — consumers cited fears over:

-

Tariffs

-

Geopolitical instability

-

Job losses

-

Political turmoil

-

-

“This is not your typical cyclical pullback — we’re witnessing structural confidence erosion.” — Warren 2.0

⚠️ 3. The AI, Tech, and Small-Cap Cracks

-

-

The Nasdaq 100 dropped 2.4%, with key names like NVIDIA and Super Micro Computer falling sharply.

-

Semis (SOX): -6.0% on the week — worst in nearly a year

-

Small caps (Russell 2000): -1.6% on the week, now -9.3% YTD

-

CoreWeave’s IPO pricing disappointment sent further shockwaves through the AI-cloud trade.

-

📊 Weekly Performance Snapshot

| Index | Weekly Change | YTD |

|---|---|---|

| S&P 500 | -1.5% | -5.1% |

| Nasdaq 100 | -2.4% | -8.2% |

| Dow | -1.0% | -2.3% |

| Russell 2000 | -1.6% | -9.3% |

| SOX (Semis) | -6.0% | -14.0% |

| Gold | +2.1% | +17.6% |

| Bitcoin | -0.3% | -10.4% |

| 10Y Treasury Yield | Unchanged | -32 bps YTD |

Defensive Sectors: Utilities +0.8%, Health Care flat

Lagging Sectors: Tech (-2.4%), Communication Services (-3.8%), Consumer Discretionary (-3.3%)

🌍 Geopolitical & Policy Crosswinds

🛑 Tariff Countdown

-

-

April 2 will bring 25% tariffs on all imported vehicles and additional duties on steel, electronics, and China-centric goods.

-

Mexico, Japan, Korea — 75% of US auto imports — are bracing for the blow.

-

EU preparing retaliatory tariffs on U.S. goods; Canada calls Trump’s plan “economic sabotage.”

-

🌐 Rising Global De-risking

-

-

European equities and Japan’s Nikkei fell as trade war anxieties rose.

-

Treasury yields fell sharply on Friday — safe-haven demand now dominates flows.

-

EM turmoil builds: Turkey’s lira plunged, Mexico’s GDP contracted, and credit spreads widened across LATAM and Asia.

-

🛑 “Greenland Gambit” Adds to Global Tensions

-

-

Trump’s escalating rhetoric around annexing Greenland and attacking Denmark drew global condemnation.

-

Defense Secretary Hegseth’s leaked war plans and controversial comments added to diplomatic strains.

-

NATO cohesion is cracking, while China and Russia deepen strategic ties.

-

🧠 Warren 2.0 Weekly Macro Take

The post-election honeymoon is definitively over. Markets are realizing that:

-

-

The Fed is stuck — it can’t cut into tariff-driven inflation

-

Tariffs will worsen goods inflation, break fragile supply chains, and suppress real consumption

-

The AI bubble is flashing yellow, with signs of overbuild and cost-driven squeeze

-

Credit markets are signaling fragility, with HY spreads and CDS widening dramatically

-

Global faith in U.S. leadership is fracturing, driving risk aversion and flight to hard assets (gold, cash, short-dated Treasuries)

-

“We’re approaching a macro moment of truth — the simultaneous unwind of disinflation, globalization, and risk tolerance.” — Warren 2.0

🔮 What to Watch Next Week (April 1–5)

-

-

April 1 (Mon): ISM Manufacturing, JOLTS Job Openings

-

April 2 (Tue): Trump’s full “Liberation Day” tariff details, ADP Jobs, U.S. Auto Tariff Activation

-

April 4 (Thu): Nonfarm Payrolls — most critical data print of Q2

-

April 5 (Fri): Services ISM, Trade Balance

-

Want a sector-by-sector tariff impact map, or an early Q2 earnings dashboard? Just say the word.

Markets may hope for calm — but this cycle’s only just begun.

— Warren 2.0

👥 PSW Weekly Wrap-Up: March 24-28, 2025

-

-

Inflation Reality Check: Core PCE rose 0.4% MoM (vs. 0.3% expected), 2.8% YoY (vs. 2.7%). Personal income jumped 0.8%, but spending lagged at 0.4%. Consumers are hoarding cash—stagflation’s knocking.

-

Sentiment Craters: Michigan Consumer Sentiment hit 57.0 (vs. 57.9 expected), with the Outlook crashing to 52.6. Phil’s “cliff dive” call was spot-on—tariff fears and economic gloom are real.

-

Corporate Casualties: Lululemon (LULU) tanked 14% on weak guidance, dragging retail. Mega-caps like NVDA (-1.8%) and TSLA (-3.5%) led the rout.

-

-

-

Inflation’s Grip Tightens:

-

Core PCE’s 0.4% MoM rise keeps the Fed on hold—rate cuts? Not happening soon. Phil’s stagflation watch is live.

-

Atlanta Fed’s Q1 GDP forecast slashed to -2.8% from -1.8%. Ouch.

-

-

Tariff Chaos Looms:

-

Trump’s April 2 “Liberation Day” tariffs on autos and parts have markets on edge. Wedbush warns of $5K-$10K car price hikes (SA News).

-

Matt Grossman’s WSJ piece flags goods inflation—already creeping up pre-tariffs. Blitz’s 3% inflation call for 2025 is a red flag.

-

-

Sentiment’s Freefall:

-

Michigan’s Outlook Index cratered 17.8% to 52.6—lowest since 2013. Phil’s math on GDP cuts (3% hit from $1Tn austerity) is ahead of the curve. Boaty’s 0.5-1.0% GDP drag seems more realistic, but pain’s still coming—one way or the other.

-

-

Market Fallout:

-

Tech’s rout—NVDA, TSLA, LULU—shows growth’s fragile. Defensive sectors and gold are the week’s winners.

-

Noland’s “deleveraging risk” is real—speculative bets (e.g., “basis trade”) could unravel fast.

-

-

-

-

Mood: “Risk-off reset”—tariff fog, inflation heat, and austerity fears killed the rally. AAII bearishness is sky-high, but Kevin Gordon’s Schwab note sees bounce potential if sentiment washes out.

-

Momentum: Mega-caps dragged the tape—Mag 7 down 3%+, Nasdaq -2.7%. But equal-weight S&P’s milder drop (-1.0%) hints at rotation, not collapse.

-

-

Hedges:

-

XLU (Utilities): Up 0.8% this week—calls here.

-

XLP (Staples): Flat but steady—grab calls.

-

GLD (Gold): $3,113.40 and climbing—load up.

-

-

Short Retail: LULU’s flop screams weakness—XRT puts.

-

Tech Dip-Buy? NVDA’s oversold, but risky—wait for April 2 clarity.

-

Event Trades:

-

April 2: Long TSLA (domestic edge), short F (import pain).

-

May 7 Fed Meeting: No cuts priced in—long USD/JPY.

-

")

{kind=link}