{kind=link}

Rather than stressing over whether AAPL or MSFT can justify 30x earnings, how about investing in a pedigreed tech company that "only" has a $34Bn market cap but makes $4Bn in profits on $63Bn in sales? HPQ does not have AAPL's growth but they are steady performers and even made $2.8Bn last year, during the lockdown.

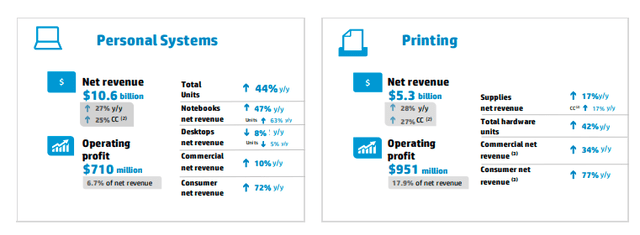

I love their new, trendy logo but it's the same old HP, making so many things that businesses depend on every day along with a thriving service division. Windows 11 requires better hardware so I think PC sales will pick up this year – especailly considering companies did little or no upgrading last year. HPQ still has 42.4% of the global printing market and I still think that, if you want to pick an ultimate winner in 3D printing – it will be HPQ.

HPQ pays a respectable 2.72% dividend but, initially, for the LTP, we'll just promise to buy it if it gets cheaper:

- Sell 15 HPQ 2023 $25 puts for $3 ($4,500)

- Buy 25 HPQ 2023 $22 calls for $7.50 ($18,750)

- Sell 25 HPQ 2023 $30 calls for $3 ($7,500)

That's net $6,750 on the $20,000 spread so we have $13,250 (196%) profit potential if HPQ can finish over $30 in Jan 2023. Not a big ask and our worst case is being assgined 1,500 shares at $25 and losing our $6,750, which would be another $4.50/share so we'd be at net $29.50, which is more than HPQ is now so it's an aggressive play but we're very happy to double down on this one if it sells off.