By The Round Table Consulting Group

🧠 Wheeeeeeeeee!

Another day, another “ceasefire extension,” another 0.8% pop in Brent to $99 and WTI to $90.30 (Bloomberg). Clack, clack, clack, clack… that’s the sound of this rally car ratcheting up the first hill of the roller coaster – and if you listen closely under the CNBC cheerleading, it’s also the sound of 147 container ships idling in the Persian Gulf waiting for someone, anyone, to tell them it’s safe to move (Maersk advisory).

Trump announced the ceasefire is extended “indefinitely until talks conclude“ – which is a neat trick, because as of Tuesday night the Iranian delegation still hadn’t landed anywhere, Vance’s flight manifest is still unconfirmed and the naval blockade of Hormuz remains fully in place. Peace! We have peace! Please ignore the warships…

Jon Stewart’s 2009 takedown of CNBC comes to mind this morning. Back then it was “Bear Stearns is fine.” Today it’s “No Peace Plan, No Problem“ (WSJ) – a headline so on-the-nose I half expected it to be followed by “Also, gravity is optional.”

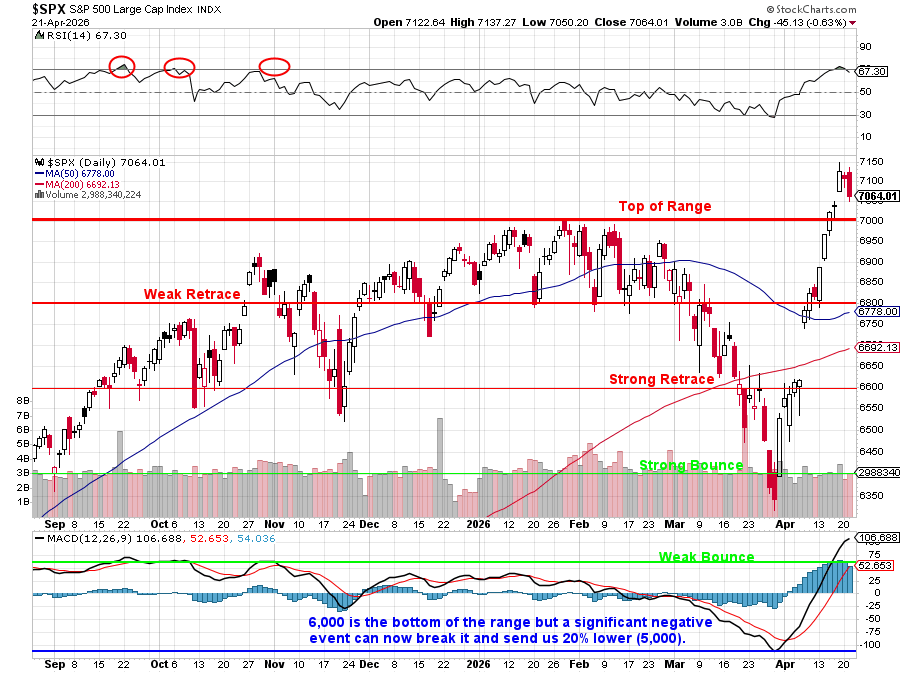

When the Wall Street Journal’s front-page feature on the wartime rally leads with a 30-year-old Amazon delivery driver who said ‘F— it’ and bought Robinhood because of the war, you don’t need an RSI indicator. You have the WSJ indicator. And it’s flashing the same thing as the RSI.

The article is useful, but as a contrarian tell rather than as confirmation. It’s the sentiment top, in written form.

So let’s do what we do. Let’s look at the evidence – not the speculation, not the tape-painting, not the White House press releases – and figure out what’s actually happening under the hood.

The Oil Math Doesn’t Care About Your Feelings

Here’s the thing about physical commodities: they don’t read Truth Social. The IEA’s March supply report shows a 10.1 million barrel-per-day supply loss – and the agency itself called it “the largest single-month supply loss in history, exceeding 1973, 1979, and 2022 combined” (IEA Monthly Oil Market Report). Let that sink in. Every oil shock you’ve ever studied in business school, added together, was smaller than what happened in March and is continuing through April (at least).

Kpler’s tanker tracking data shows ~500 million barrels of waterborne crude have failed to load or discharge in the seven weeks since the Strait went hot – roughly $50 billion of physical oil, gone from the system (Oilprice.com). Hormuz throughput is running ~3.8M bpd early April versus the 20M+ bpd pre-war baseline (WSJ).

The IEA has already burned through a 400 million barrel strategic release, dropping member-country stockpiles by ~20% (IEA). Wood Mackenzie’s base case is 11M bpd offline with a minimum 6-month path to normalize – and IEA Executive Director Birol told the FT this weekend that full recovery is a 2-year project (Financial Times).

JPMorgan’s commodities desk ran the inventory math and concluded that the “pre-closure barrels in transit” buffer that’s been cushioning spot prices was fully depleted by approximately April 20 (JPMorgan Commodities Weekly). We are now trading on live supply. That’s why every “ceasefire is holding!” headline only buys a 0.5% dip before buyers show up – the physical market knows!

And this matters more than the futures print, because the real crisis is one level downstream.

The Jet Fuel Cliff Is Not a Metaphor

If crude is tight, refined products are a full-blown emergency – and this is where the actual corporate carnage is happening.

-

-

Jet fuel hit $4.88/gallon at the NY Harbor spot on April 3, up from $2.50 on February 27. That’s +95% in five weeks (Platts/S&P Global).

-

Crack spreads are running $65-138/barrel versus a normal $10-25 range – 3 to 7 times normal (Energy News Bulletin).

-

US gasoline is $4.02/gal (+35%), diesel $5.49/gal (+46%) (EIA weekly).

-

And here’s the piece the cable-news crowd doesn’t understand: refiners cannot simply “make more jet fuel.“ A barrel of crude yields a fixed slate of products based on the molecular chemistry of the input crude and the configuration of the cracker. You can nudge the slate 2-3% at the margin. You can’t just flip a switch and turn gasoline into Jet-A (Byrnes / LinkedIn technical breakdown). That’s why crack spreads are insane – refiners are physically constrained from arbitraging the mismatch away.

-

- ACI Europe and Rystad Energy both estimate the European jet fuel buffer runs dry between April 30 and May 12 (Rystad Energy jet fuel note). That’s not a recession risk – that’s eight-to-twenty-day risk.

- SAS already cancelled 1,000 flights in April. Ryanair has warned of May/June cuts. The US had ~7,000 daily cancellations in early April (BTS). This isn’t coming – IT’S HERE!!!

Airlines: The Unhedged Catastrophe

Airlines: The Unhedged Catastrophe

Of the four US majors, only Delta (DAL) is meaningfully protected – and only because they own the Monroe Refinery in Trainer, PA, which physically produces their jet fuel. Everyone else went into 2026 with zero crude hedges because fuel was cheap and the forward curve was backwardated.

Wheeeeeeeeee!

The receipts:

-

-

United (UAL) slashed 2026 guidance, admitted $340M unbudgeted Q1 fuel expense, forecast $4.30/gallon Q2, and cut capacity -5% (UAL 8-K, Apr 15).

-

Alaska (ALK) suspended 2026 guidance entirely, reported a $193M Q1 loss, forecast $4.50/gal in Q2, and estimated ~$600M incremental full-year fuel expense – a -$3.60 Q2 EPS hit (ALK investor update).

-

Industry-wide: ~$25B of unbudgeted 2026 fuel expense. Three of four majors are unhedged. Delta’s CEO Ed Bastian warned in Tuesday’s call that “more consolidation and potentially some bankruptcies“ are coming (Delta Q1 earnings call transcript).

-

Baggage fees: DAL, WN, UAL, and JetBlue all raised checked-bag fees by $10 in the last 10 days (NYT). When airlines start nickel-and-diming in April, they’re not bluffing – they’re bleeding.

-

This is not a “buy the dip on UAL” setup. This is a “which regional goes first” setup (Phil ditched our airline plays in the last portfolio review).

The Helium Problem You Didn’t Know You Had

The Helium Problem You Didn’t Know You Had

Qatar’s Ras Laffan complex took a direct hit February 28. 27-30% of global helium supply is offline (J2 Sourcing crisis update). Repair estimates: 3 to 5 years. Lost LNG capacity: 17%, with revenue impact of roughly $20B/yr to Qatar alone (10% of their GDP). SK Hynix has already started diversifying suppliers, which means semiconductor fabs across South Korea and Taiwan are now juggling a second supply chain risk on top of the one they already had. Asian LNG spot prices are up 140% (Platts Asian LNG).

Helium matters for MRI machines, semiconductor manufacturing, rocket launches, welding, and fiber optics. It has no substitute. If you want to own one obscure, non-obvious beneficiary: look at Air Products (APD) and Linde (LIN), the two non-Qatari majors who can capture price. Phil has often mentioned APD as a “nice, boring company to own.“

Shipping: The Other Bill That’s Coming Due

Maersk suspended FM1 (Far East-Middle East) and ME11 (Middle East-Europe) routes (Maersk advisory). 147 container ships are sheltering in the Gulf. Maersk CEO Vincent Clerc told Bloomberg they are adding $200 per 20-ft container and expects 15-20% freight rate increases passed to consumers (Bloomberg).

UPS: $0.64/lb Middle East surcharge. FedEx: $0.50-$1.50/lb surcharge. The UPS fuel surcharge ratcheted from 21.5% to 26.5% in weeks (Supply Chain Dive). This feeds directly into consumer staples margins over the next two quarters – and it’s why we added UPS on the dip: they collect the surcharge while the street frets about volumes.

The Fed Problem Nobody Wants to Talk About

Elizabeth Warren on the Senate floor Monday: Kevin Warsh “did not show the courage and independence to say ‘No’ to a President who has made clear he wants control of the Fed“ (Bloomberg). Next Tuesday-Wednesday (April 28-29) is FOMC. The market is still pricing 1-2 cuts by year-end. With oil where it is, PCE printing April 30, and a Chair confirmation vote that may or may not torpedo Fed independence – the tail risk here is not that they cut too slowly, it’s that “the Fed” becomes a meaningfully different institution.

The Opportunity Side – Because This Is Still a Market

Yes, we are cautious. Yes, we are hedged. No, we are not running to cash – because when oil prices are dislocated and refined product markets are structurally mispriced, specific companies make generational margins. Here is where we are leaning:

Refiners – The Crack Spread Is Your Friend

-

-

Valero (VLO) – pure-play refiner, $65-138 crack spreads are dropping straight to the bottom line. Reports April 29.

-

Marathon Petroleum (MPC) – same trade, bigger footprint, raised guidance twice.

-

Exxon (XOM) – integrated, but the downstream chemicals + refining combination is exactly the wrong-way trade everyone dumped in March.

-

Chemicals – The Street Is Finally Catching Up

-

-

LyondellBasell (LYB) – up 40.1% in March alone. Alembic upgraded to $100 from $66. RBC raised to $91. Citi modeling 31% operating income growth (Intellectia / LYB analyst roundup). Earnings May 1 – we’ll get an actual read.

-

Dow (DOW) – upgraded by Barron’s; 11-15% of global ethylene/polyethylene capacity is affected by the Qatar/Iran disruption.

-

CF Industries (CF) – fertilizer play, natural gas feedstock advantage.

-

Delta (DAL) – The Only Airline We’d Touch

Monroe Refinery ownership + Q1 guide-raise + industry consolidation beneficiary. If Bastian is right about bankruptcies, DAL is the one that emerges bigger.

Defense & Energy Services

Still in favor, and the ceasefire extension doesn’t change the 6-24 month capex cycle already underway.

The Dangers We Are Not Ignoring

-

-

Airline credit risk – watch the regionals and Alaska. Bondholders are repricing.

-

Consumer staples margin compression – freight + fuel + packaging. Think PG, CL, KMB – we are not buying them here even with dividends.

-

Europe jet fuel cliff April 30-May 12 – if SAS is the canary, LHA, AF-KLM, and IAG are the mine.

-

Fed independence – if Warsh is confirmed in a politically-compromised process, the long bond tells you what it thinks.

-

7,000 to 6,800 air pocket – the S&P closed Tuesday at 7,042 with RSI 70+. The “wall” at 7,000 is made of short-covering and CTA flow, not conviction. We are still carrying our VIX May calls, our SPX 7,100/7,200 bear call spreads, and our SPY put spreads, SQQQ and TZA hedges. Dry powder waits at 6,800 (weak support) and 6,600 (strong) but there is no urgency to buy here – at S&P 7,064 with the RSI testing 70 (overbought).

-

The Two-Week Gauntlet

The Bottom Line

We already told you last week: the rally is a house of cards built on low-volume distribution days papered over by short-covering on every “ceasefire” rumor. Nothing we’ve seen this week changes that view – but here’s the wrinkle that keeps us from being pure bears: the dislocation is so large and so lopsided that specific longs (refiners, chemicals, Delta) are fundamentally cheap while specific shorts (unhedged airlines, consumer staples) are fundamentally broken.

So we stay paired. We keep the index hedges on. We own UPS (Monday’s Top Trade, 2028 spreads, net $12,450 on $50K, 13.5x forward earnings). We own SYF (Tuesday’s Top Trade, 8x forward, $6.5B buyback = 23.8% of float, 13% dividend hike). We sell premium into every VIX panic and every “peace” squeeze. And we keep dry powder for 6,800 and 6,600 – because the physics of oil, the chemistry of a refinery, and the arithmetic of an unhedged airline balance sheet do not care about Truth Social.

The opportunities are real. The dangers are real. The only thing that isn’t real is the narrative coming out of Washington.

Clack, clack, clack, clack… let’s see what the top of the hill looks like.

America First: The Grand Strategy of Donald Trump")

{kind=link}