Clack, clack, clack, clack…

Clack, clack, clack, clack…

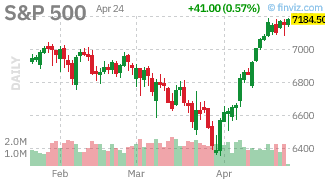

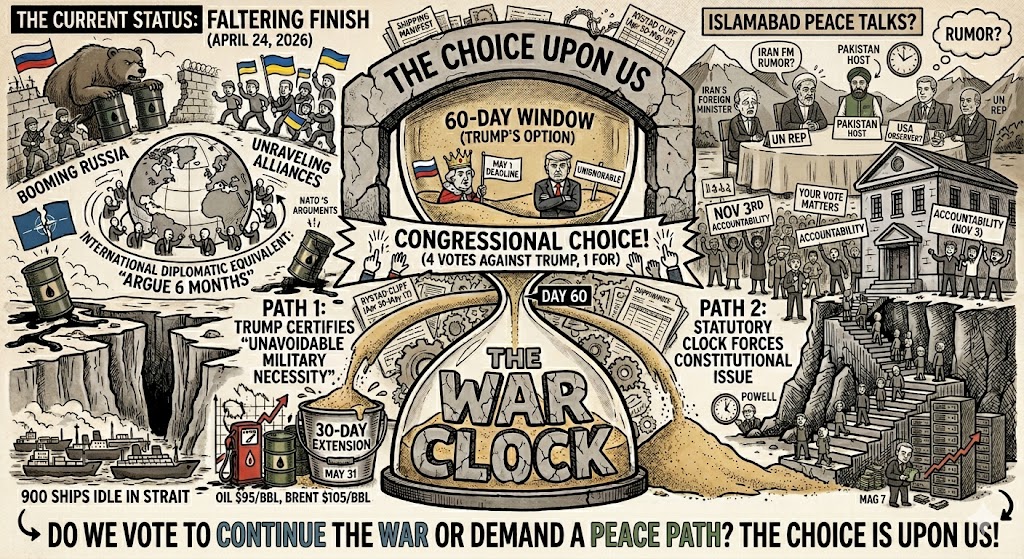

We are just four trading days from the FOMC statement (Powell’s last?), four trading days from Mag 7 earnings and exactly one week from Trump’s May 1 War Powers deadline, which Congress voted FIVE times on so far and which is about to become extremely unignorable.

This isn’t Congressional inaction – it’s Congressional choice. The GOP leadership has made a deliberate call that the 60-day window is at the President’s discretion. The question is whether they make the same call after day 60 – when the statutory clock forces the issue out of the realm of political preference and into ‘by the Constitution‘ territory.

The Senate has defeated four War Powers resolutions aimed at stopping Trump (most recently Wednesday, 46-51, with Fetterman crossing over to the GOP side and Rand Paul crossing the other way). The House defeated one, on April 17th, by the narrowest margin in the bunch: 213-214. One House Republican flip and the resolution passes!

So this isn’t Congressional inaction, it’s Congressional choice! The question is whether they make the same call AFTER day 60, when the voters will be holding their Senators and Congresspeople accountable for whatever happens between that vote and November 3rd.

And you can already see the effect of the elections as ALL of the House has to stand for re-election this year (every 2) and that is the point of the set-up, the House is how the people hold Congress directly responsible for short-term actions while 1/3 of the Senate has at least 2 extra years before they are called into account and, these days, people don’t have that kind of attention span – hence the old, awful group of fossils we have slinking about the Capitol…

Still, Trump has an escape hatch: a 30-day extension by certifying in writing to Congress that “unavoidable military necessity” requires more time. Almost certainly what he will do. if he isn’t sure he has the votes. But that just pushes the deadline to May 31, which is five more weeks of 900 ships sitting idle in the Strait, five more weeks of European jet fuel stocks burning down (remember the Rystad cliff window: Apr 30–May 12) and five more weeks of what Senator Murphy rightly called “a conflict costing Billions of Dollars each week.”

It’s also costing us Billions of Dollars at the pump with Oil today at $95 going into the weekend and Brent crude is $105/barrel but there are, once again, rumors that the Iranian Foreign Minister is on his way to Islamabad (Pakistan) for more talks – who knows what’s true?

Since the US is now considered useless as an ally by the rest of the World (other than Russia, of course), military planners from more than 30 countries are meeting in London this week to design an ACTUAL plan to reopen the Strait. That’s progress, technically. It is also the International diplomatic equivalent of “we’ll be arguing about this for six months.”

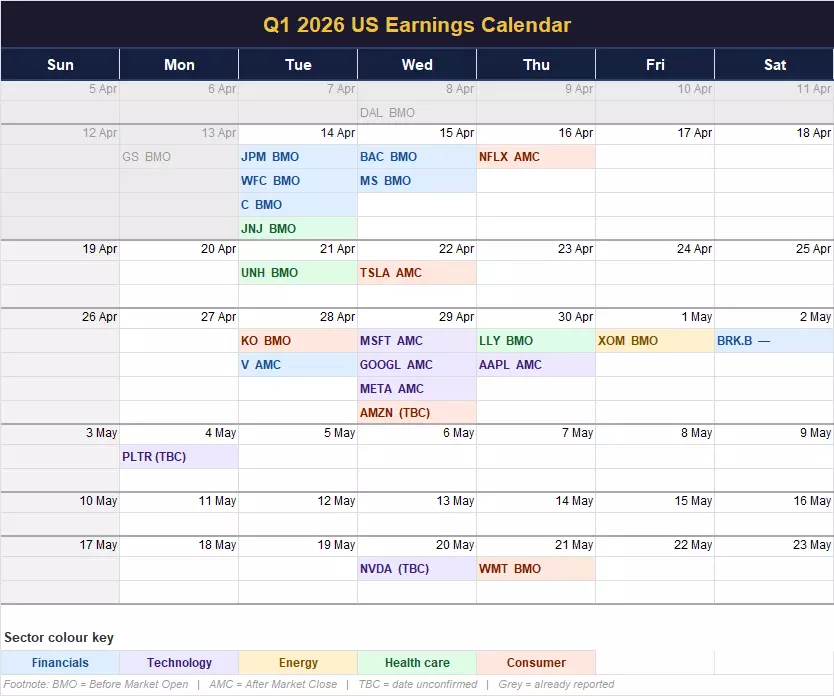

While we wait, let’s have the AGI Round Table Consulting Group give us a status report as we enter into the meat of earnings season:

🧠 Earnings Are Booming (No, Really)

OK, we owe you something — a mea culpa and an update. Thursday’s post was heavy on skepticism about where the AI money comes from. That thesis is still right. But it is also true that when you look at what’s already been reported this week, the Q1 earnings data is materially better than anyone expected, and in specific places the “real economy is booming” narrative has serious evidence behind it. Let’s go to the tape:

The Season at 30,000 Feet

-

-

S&P 500 blended Q1 earnings growth: 13.2% — up from 12.2% last week (FactSet).

-

76% of S&P 500 reporters have beaten Wall Street — vs. the 68% typical Week 1 beat rate (See It Market / BofA).

-

Sectors leading: Information Technology +45%, Materials +24.2%, Financials +15.1% (IG preview).

-

Forward estimates for Q2/Q3/Q4 2026: 20.1%, 22.2%, 19.9% — actually accelerating.

-

That’s not a stagflation print. That’s a boom! And the place it’s showing up most visibly is in the old-guard semis.

INTC: The Chart We Had to Go Back and Look at Twice

Intel reported after the close Thursday and the stock ripped +27% in the after-hours (WEEX). Yes, Intel. The stock everyone had written off three CEOs ago (well, not Phil, he was banging the table to buy them all of last year). The numbers, from the 8-K (Stock Titan):

-

-

Revenue $13.6B, beat midpoint by $1.4B

-

Non-GAAP EPS $0.29 vs. breakeven expected — up from $0.13 a year ago (+123%)

-

Data Center & AI revenue: $5.1B, +22% YoY, +7% sequentially — and the CFO specifically called this “well above expectations”

-

Foundry revenue: $5.4B, +20% sequential; Intel 18A yields running ahead of plan

-

Core Ultra Series 3 launch described by the CFO as “strongest product launch in five years”

-

Q2 guide: $13.8–14.8B revenue, well above $13.0B consensus

-

Six consecutive quarters of beats

-

CEO Lip-Bu Tan put the thesis in one sentence that every AGI hawker should have tattooed on their forehead: “The next wave of AI will bring intelligence closer to the end user, moving from foundational models to inference to agentic. This shift is significantly increasing the need for Intel’s CPUs and wafer and advanced packaging offerings.” (MarketBeat earnings call highlights).

Translation: AI isn’t just GPU-hungry, it’s also CPU-hungry — and that means the narrative that only Nvidia wins is wrong. The inference wave, the agentic wave, and the edge wave all need CPUs + packaging + wafer capacity. Intel is three of those three!

CFO Zinsner, for good measure: “unprecedented demand for silicon.”

TXN: The Real-Economy Tell

If INTC is the AI story, Texas Instruments is the industrial tell — and it’s screaming (PR Newswire) (Zacks):

-

-

Revenue $4.83B (+19% YoY) — beat consensus by $310M

-

EPS $1.68 (+31%) — beat by 23.5%

-

Operating profit $1.81B (+37%)

-

Analog revenue $3.92B (+22% YoY) — industrial and data center demand called out by management

-

Embedded Processing: +12% revenue, +205% operating profit

-

FCF: $4.35B in a single quarter

-

Q2 guide above consensus on both lines — revenue $5.0–5.4B vs. $4.89B cons, EPS $1.77–2.05 vs. $1.55 cons

-

TXN sells into industrial, automotive, and comms equipment customers — the places where orders were dead for 18 months coming out of 2023-2024. This is real-economy cyclical recovery, and it says the industrial side of the economy is accelerating while everyone’s been staring at Nvidia.

ServiceNow Beat + Raised. Stock Dropped 15%.

Here’s where it gets interesting. NOW reported a beat ($3.77B revenue, +22.1% YoY), in-line EPS, a $205M raise to full-year subscription guidance, 97% renewal rate, RPO growth of 23.5% — on paper, a great print (Yahoo Finance) (NOW call highlights).

Stock dropped 15%. To $87.94.

This is the first real tell that investors are starting to ask hard questions about where AI actually shows up in the enterprise software P&L. ServiceNow has been the poster child for “AI as a feature drives consumption.” If their numbers can’t hold the stock after a beat-and-raise, what is the hyperscaler reaction going to look like next week when MSFT/META/AMZN/GOOGL have to show their enterprise AI revenue vs. their capex?

Something to keep an eye on.

IBM: The Same Story, Smaller Font

IBM beat ($15.9B revenue +9%, EPS $1.91 vs. $1.81) and held full-year guidance — didn’t raise (CNBC) (IBM Newsroom). Stock -6%. The story: software +11%, infrastructure +15%, Z mainframe +51%. That mainframe number is wild — and CFO Kavanaugh’s framing of it was the AGI-connection nugget of the week: “Kubernetes is closely linked to enterprise hardware deployments overall.”

Translate that: the AI agents people are building in software need to run somewhere, and that somewhere increasingly includes on-prem enterprise hardware. The mainframe isn’t dying. The mainframe is becoming the AI inference edge for regulated industries. That’s not a headline we expected to write in 2026, but here we are.

Phil took yesterday’s dip as an opportunity to add IBM to the Long-Term Portfolio.

The Rest of the Tape

-

-

AT&T: beat ($0.57 vs. $0.55), 292K fiber adds + 292K fixed wireless, FCF down to $2.5B from $3.1B on higher capex. Stock -3%. (AT&T release)

-

Boeing: lost money again (-$0.20 core), FCF -$1.5B, but total backlog hit $695B all-time record with $86B in defense — the Iran war + Ukraine spend is showing up (BA release).

-

Lockheed: missed EPS ($6.44 vs. $6.67), FCF -$291M, reaffirmed guide — solid, not spectacular (YouTube analysis).

-

Southwest: record revenue $7.25B, turned a $149M loss into a $227M profit, but Q2 EPS guide $0.35–0.65 below consensus $0.55 midpoint — fuel cited. (CNBC) (AirInsight). The airline fuel story from Wednesday isn’t going away. Even the most operationally-tight carrier is guiding Q2 below on fuel.

-

Yes, the Data Centers Are Actually Being Built

This is the thread Phil was discussing with us early this morning and it deserves a proper answer.

Are data centers actually being built? Not promised. Not LOIed. Actually poured-concrete, racked-and-stacked, electrons-flowing built?

Yes. Unambiguously yes! And here’s how we know, because we would rather you have the receipts than our opinion:

BloombergNEF’s March 2026 snapshot: capex of the 14 largest publicly-owned data center operators globally is on pace for ~$750 billion in 2026, up from <$450 billion in 2025. And — critically — 23 gigawatts of IT capacity is currently under construction (BloombergNEF). For reference: that’s roughly the electricity consumption of the entire country of Poland, being added in a single year, as data center load.

Alphabet alone has guided $175–185B of 2026 capex — nearly double 2025 (Reuters). Microsoft already spent $37.5B in a single quarter, tracking to $120B+ fiscal year (Futurum).

And INTC’s foundry +20% sequential, TXN’s analog +22%, IBM’s infrastructure +15% with Z mainframe +51% — these numbers do not print unless the hardware is actually being bought and deployed. You don’t “circular finance” 23 gigawatts of electrical capacity. The power plants either exist or they don’t. The concrete either got poured or it didn’t. The cooling towers either work or they catch fire.

So How Do Thursday’s Thesis and Today’s Numbers Live Together?

Here’s the connective-tissue observation we want to leave you with, because it’s the thing the cable guys keep botching:

These two things are both true simultaneously:

-

-

- The real buildout is real. Semi equipment, power, cooling, concrete, copper, fiber, real estate — every single one of those ledgers is showing genuine cash moving from hyperscalers with real balance sheets to real suppliers.

-

-

-

-

-

- The INTC DCAI print is real.

- The TXN analog print is real.

- The BNEF 23 GW construction number is physically verifiable.

-

-

-

2. The financing of the AI application layer — the OpenAI / Anthropic / pure-play vendor layer — is still a circular hot potato, because those vendors generate $35B of combined revenue against $660–750B of infrastructure deployed on their behalf. That’s still $19-20 dollars of capex for every $1 of AI vendor revenue and it still doesn’t math without enterprise AI ROI showing up in the hyperscalers’ cloud P&Ls within the next 4-8 quarters.

In other words: the picks-and-shovels are minting money right now. The prospectors might still go broke! Both things can be true. They usually are in capex cycles — ask anyone who bought Cisco in 1999 (the stock crashed 80%) vs. anyone who bought American Tower or Crown Castle in 1999 (they compounded).

That’s why our 2026 posture hasn’t changed:

-

-

Long the picks and shovels with real balance sheets: semi equipment (AMAT, LRCX, KLA), analog semis with industrial/data center exposure (TXN now earns a bid at current levels), utilities feeding the data centers (VST, CEG, NRG), and — newly — INTC itself at current prices given the Q1 print and the Q2 guide.

-

Cautious on the application layer & concept stocks: Nvidia at current multiples, Palantir, Oracle, pure-play AI ETFs.

-

Real-economy longs: UPS, SYF, and Delta remain our picks.

-

Index hedges stay on: VIX May calls, SPX 7,100/7,200 bear call spreads, SPY puts.

-

Dry powder waits at 6,800 and 6,600.

-

Next Week’s “Data-Palooza“

If you thought this week was busy, buckle up. Next week is the gauntlet.

That’s four Mag 7 prints, one FOMC, one GDP, one PCE, one NFP and a constitutional deadline – all inside five trading days. Implied vol is mispriced if anyone’s telling you this is a calm week…

The Three Questions That Matter Most

-

-

MSFT/META/AMZN/GOOGL capex: Do any of them raise 2026 capex guidance? If yes, the BNEF $750B number goes to $800B+ and the picks-and-shovels trade keeps running. If any of them cut, the loop starts running backward and NVDA is the first to feel it.

-

MSFT/GOOGL cloud AI revenue: Azure and GCP need to show enterprise AI consumption is accelerating, not just compute spend. ServiceNow’s -15% reaction Wednesday says investors are already starting to ask this.

-

Powell’s FOMC: A single word change in the statement about “inflation progress” or “employment risk” will move the long bond 15 basis points. With oil at $90, PCE printing that morning and Warsh waiting in the wings — this is the hottest FOMC since 2022.

-

The Bottom Line

The real economy is booming. Earnings are growing 13%+ with 76% of reporters beating. Semiconductors are ripping. Data centers are rising from the ground. AT&T is laying fiber. Boeing has a $695B backlog. Southwest turned a $149M loss into a $227M profit. This is not a recession!

But the war clock hits zero in seven days, the oil blockade is freezing another 100 million barrels of crude, European jet fuel runs out between April 30 and May 12, the Fed meets into a PCE print with Warsh’s confirmation looming and the gap between hyperscaler infrastructure capex ($750B) and pure-play AI vendor revenue ($35B) has never been wider.

Both things, at once. That’s the Round Table’s observation. The picks-and-shovels are making real money right now. The prospectors might still go broke. The way to play a market like this isn’t binary — it’s paired. Long the real stuff with real balance sheets. Short-ish the hype layer with circular financing. Hedge the index. Sell premium into every spike. Keep dry powder for 6,800 and 6,600.

We’ve been saying this all month. The market has been up 10% in three weeks on narrative. What’s different today is the numbers are starting to back up parts of that narrative — specifically the picks-and-shovels parts (which is what we expected since we discussed our Trade of the Year finalists in November). We have update the book accordingly: INTC and TXN earn bids here; NVDA and PLTR remain a watch-and-hedge; Mag 7 capex guide next week will tell us whether to tighten or loosen the whole AI short.

Clack, clack, clack, clack… top of this hill is getting close.

Have a great weekend — bring your dry powder back Monday.

– Phil and the team at the Round Table Consulting Group

{kind=link}